How Banks Stay Safe: A Guide to Operational Risk Management

Managing operational risk is like wearing a seatbelt for a bank—it keeps everything running smoothly and prevents big crashes. In the world of finance, things can go wrong quickly. A computer glitch, a dishonest employee, or a clever hacker can cause huge trouble.

To stay safe, financial institutions use a special plan called Operational Risk Management (ORM). This guide explains how they do it in simple steps.

What is Operational Risk?

Operational risk is the chance of losing money because of internal failures. It is not about the stock market going down; instead, it is about things breaking inside the business.

The Four Main Categories

Experts usually split these risks into four distinct groups:

- People: Includes human error (typing the wrong number) or internal fraud (employee theft).

- Processes: Occurs when the "rules" of the bank fail, such as forgetting to verify a customer’s ID.

- Systems: Technology failures, such as a banking app crashing or a cyber-attack.

- External Events: Events outside the bank’s control, like floods, fires, or global pandemics.

Why Managing Risk Matters in 2026

In 2026, banks are faster than ever, utilizing instant payments and AI bots. Because things move so rapidly, a small mistake can escalate into a giant problem in seconds.

- Avoiding Huge Fines: Governments impose strict penalties. Failing to manage risk can cost millions in regulatory fines.

- Keeping Customer Trust: Trust is the most important asset a bank owns. If data is lost to hackers, customers will leave.

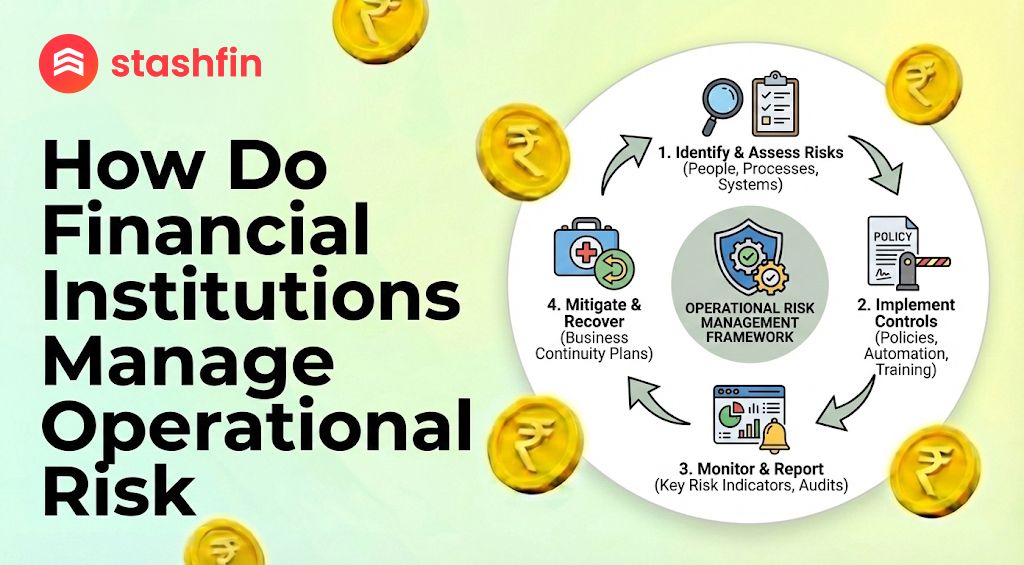

How Financial Institutions Manage Risk (Step-by-Step)

Banks follow a continuous cycle to keep risks under control.

Step 1: Finding the Risks (Identification)

Banks ask, "What could go wrong here?" They analyze historical data and monitor new trends, such as AI-driven scams.

Step 2: Measuring the Danger (Assessment)

Banks evaluate risk based on two factors:

- Frequency: How often will this happen?

- Severity: How much money will be lost if it happens?

Step 3: Fixing the Weak Spots (Mitigation)

Strategies to stop risks include:

- Security: Hiring more guards or cyber-experts.

- Risk Transfer: Buying insurance.

- Technology: Upgrading to more secure software.

- Training: Educating staff to avoid phishing links.

Step 4: Watching for Changes (Monitoring)

Banks use Key Risk Indicators (KRIs). These act like "smoke detectors." For example, a spike in failed login attempts triggers an alert for a potential hack.

Smart Tools Banks Use Today

In 2026, banks leverage high-tech tools to stay ahead:

- AI and Machine Learning: "Agentic AI" programs watch transactions 24/7 to spot fraudulent activity faster than any human.

- Real-Time Dashboards: Executives monitor the "health" of the bank globally. If a system fails in another country, the dashboard turns red for instant intervention.

Conclusion: Safety First

Operational risk management is the invisible shield protecting the banking world. By addressing human mistakes, fixing broken processes, and securing systems against external disasters, banks keep our money safe. In 2026, the combination of smart AI and real-time data makes this shield stronger than ever.