Section 80EE Tax Deduction on Home Loan Interest: Who Qualifies & How to Claim (2026 Guide)

If you're in a hurry to file your taxes or plan your investments, here is the essential roadmap for Section 80EE in 2026.

Quick Summary: The Section 80EE "Cheat Sheet"

- What is it? An additional deduction of up to ₹50,000 on home loan interest.

- Is it extra? Yes! This is over and above the ₹2 Lakh limit of Section 24(b).

- The Big Catch: It only applies to loans sanctioned between April 1, 2016, and March 31, 2017.

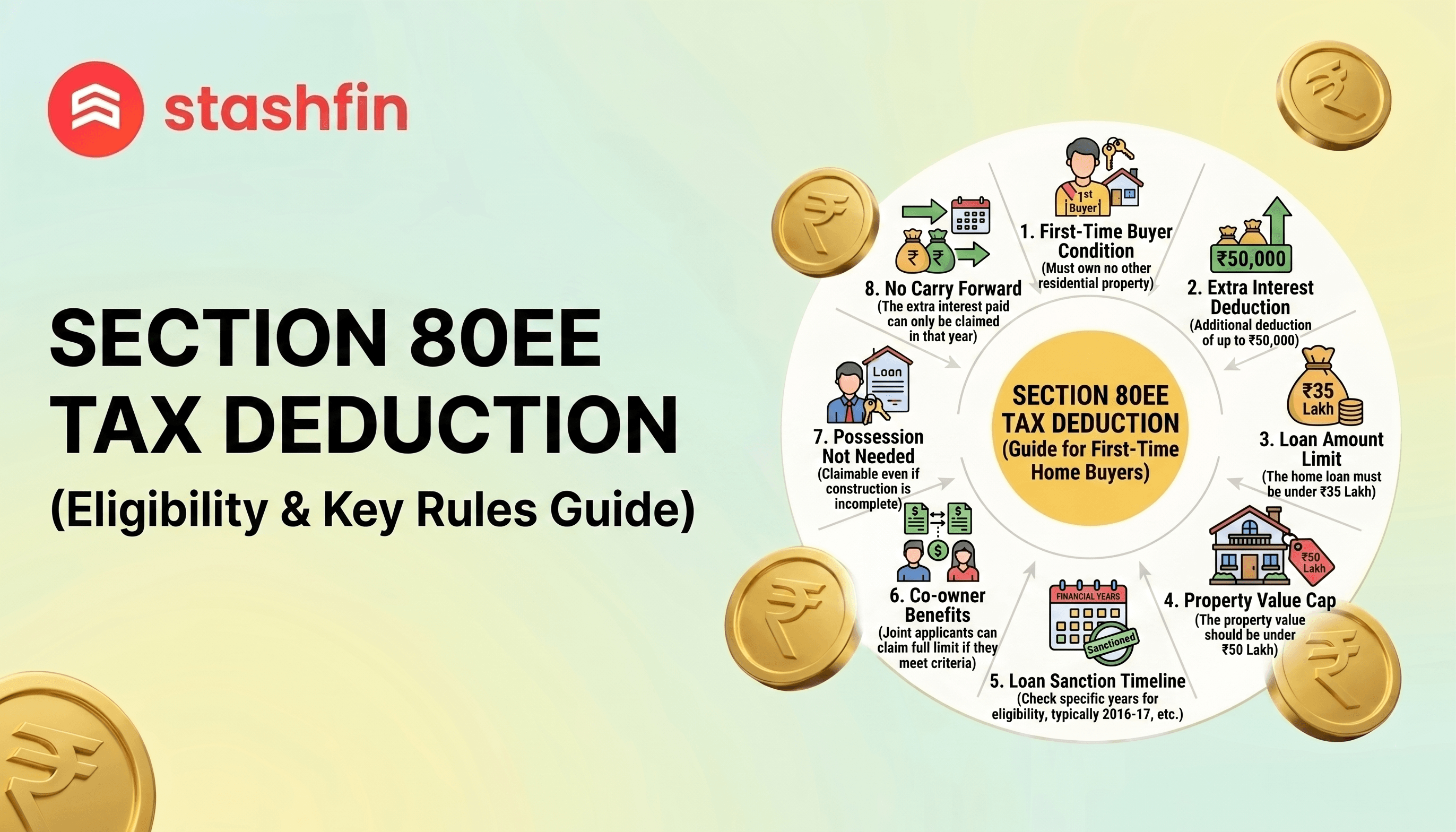

- The "First-Timer" Rule: You must not have owned any other residential property on the date the loan was sanctioned.

- Regime Alert: This benefit is available only under the Old Tax Regime.

- Property Limits: The house value must be ≤ ₹50 Lakh, and the loan amount must be ≤ ₹35 Lakh.

1. What is Section 80EE? The "Bonus" for First-Time Buyers

Section 80EE was introduced to incentivize the "housing for all" mission. While Section 24(b) is the standard deduction, 80EE acts as a "loyalty bonus" for those who purchased affordable homes during a specific historical window.

The Stackable Nature of 80EE

Section 80EE allows you to claim an interest deduction even after you have exhausted the ₹2 Lakh limit under Section 24(b).

Why it matters: In 2026, if your total annual interest is ₹2.5 Lakh, Section 24(b) covers only ₹2 Lakh. Section 80EE allows you to claim the remaining ₹50,000, potentially saving you over ₹15,000 in taxes if you are in the 30% tax bracket.

2. Who Qualifies for Section 80EE? The 4 Golden Rules

Since the window for new loans under this section has closed, it acts as a "grandfathered" benefit for eligible taxpayers.

- Rule 1: The Sanction Window – The loan must have been sanctioned between April 1, 2016, and March 31, 2017.

- Rule 2: First-Time Homebuyer – You should not have owned any other residential house property on the date of the loan sanction.

- Rule 3: Value Caps – The property value must not exceed ₹50 Lakh and the loan amount must not exceed ₹35 Lakh.

- Rule 4: Individuals Only – This is available only to Individual Taxpayers (not HUFs or firms).

3. Section 80EE vs. Section 80EEA vs. Section 24(b)

In 2026, it is vital to distinguish between these overlapping sections:

| Feature | Section 24(b) | Section 80EE | Section 80EEA |

|---|---|---|---|

| Deduction Limit | Up to ₹2,00,000 | Up to ₹50,000 | Up to ₹1,50,000 |

| Sanction Window | Any year | FY 2016-17 only | FY 2019-20 to 2021-22 |

| Property Value | Any value | ≤ ₹50 Lakh | ≤ ₹45 Lakh (Stamp Value) |

| First-time Buyer? | No | Yes | Yes |

| Stackability? | Base deduction | On top of 24(b) | On top of 24(b) |

Note: You cannot claim both 80EE and 80EEA. They apply to different sanction windows.

4. How to Claim Section 80EE: A Step-by-Step Guide

- Obtain the Interest Certificate: Get the year-end statement from your bank bifurcating Principal and Interest.

- Exhaust Section 24(b) First: Claim the first ₹2 Lakh under "Income from House Property."

- Enter Balance in Chapter VI-A: Enter the remaining interest (up to ₹50,000) under the Section 80EE tab in your ITR.

- Maintain Paperwork: Keep your Sanction Letter and Interest Certificate ready for potential tax scrutiny.

5. Why Your Tax Regime Choice Changes Everything

In 2026, the New Tax Regime is the default. However:

- Old Tax Regime: Essential to claim Section 80EE and 24(b).

- New Tax Regime: Most deductions, including 80EE, are not available.

Comparison Tip: If your total deductions (80C + 80EE + 24b) exceed ₹3.75 Lakh to ₹4 Lakh, the Old Regime usually offers higher savings.

6. Strategic Benefits: The Power of Joint Ownership

If you bought your home jointly with a spouse in 2016-17:

- Spouse A: Can claim ₹2 Lakh (Sec 24) + ₹50,000 (Sec 80EE).

- Spouse B: Can claim ₹2 Lakh (Sec 24) + ₹50,000 (Sec 80EE).

- Total Family Shield: Up to ₹5,00,000 in interest deductions.

7. Common Pitfalls to Avoid

- Possession Not Required: Unlike Section 24(b), you can claim 80EE as soon as you start paying interest, even if the property is under construction.

- Residential Only: Plots of land or commercial shops do not qualify.

- Resale Properties: Both new and resale homes qualify as long as the loan was sanctioned in the 2016-17 window.

Conclusion

Section 80EE remains a powerful tool for those who entered the market a decade ago. By opting for the Old Tax Regime and maintaining your documentation, you can maximize your tax refund and strengthen your financial future.