What is a Government Bond Yield?

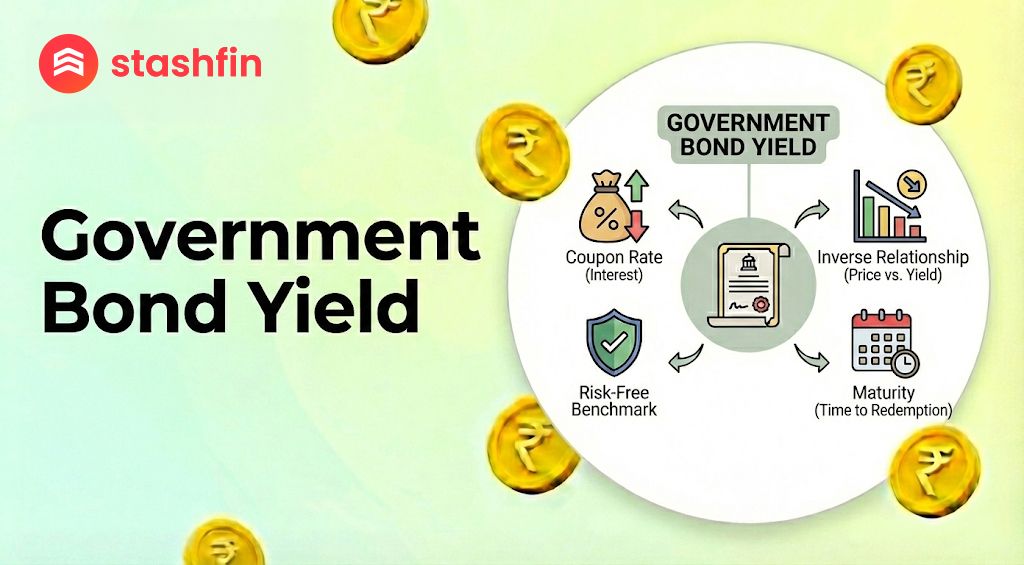

The yield is the amount of money a bond earns for an investor. People often get confused between the interest rate and the yield, but in the market, they are two different things.

The Bond Basics

Imagine you lend $100 to the government. This $100 is called the Principal. The government gives you a piece of paper (or a digital record), which is the Bond. They promise to give your $100 back in ten years.

How Yield is Different from Interest

The government sets a fixed interest rate when they first sell the bond. This is called the Coupon. If the coupon is 5%, you get $5 every year.

The Yield is different because bonds can be traded like stocks. If you sell your bond to someone else for $90 instead of $100, the yield changes. The person who bought it still gets the $5 interest, but because they paid less for the bond, their "yield" (actual return) is now higher than 5%.

The Seesaw Rule: Prices vs. Yields

Bonds work like a seesaw. This is the most important rule in the bond market:

- When the Price of a bond goes up, the Yield goes down.

- When the Price of a bond goes down, the Yield goes up.

Why Do Bond Yields Change?

In early 2026, we are seeing yields move for three main reasons:

- Central Bank Interest Rates: Banks like the Reserve Bank of India or the Federal Reserve set "base rates." In February 2026, the RBI held rates steady at 5.25%. When central banks raise rates, old bonds with lower interest become less attractive, causing their prices to drop and yields to rise.

- The Role of Inflation: Inflation is when things like milk and bread get more expensive. If inflation is high, the $5 you get from a bond buys fewer things. Investors demand a higher yield to make up for this loss of "buying power."

- Government Borrowing: If a government needs to borrow a lot of money for big projects, they must offer a better deal to attract buyers. This extra supply of bonds can push yields higher.

Why Should You Care About Yields?

Even if you don't own a bond, yields touch your life in two big ways:

- Loans and Mortgages: Banks look at government bond yields to decide how much to charge you for a loan. When the 10-year bond yield goes up, fixed-rate mortgage rates usually follow.

- Savings and Retirement: Most pension funds hold government bonds. When yields are high, these funds can grow faster, potentially leading to better retirement payouts.

The "Yield Curve" Explained Simply

A Yield Curve is a graph that shows the yields of bonds that last for different amounts of time (like 2 years, 10 years, or 30 years).

- Normal Curve: Usually, you get a higher yield for lending money for 30 years than for 2 years because there is more "time risk."

- Inverted Curve: This happens when short-term yields are higher than long-term yields. It is often seen as a warning sign of an economic slowdown.

Market Update (Feb 2026): Currently, India's 10-year G-Sec yield is hovering around 6.67% – 6.70%. Analysts describe the curve as "steepening" slightly as long-term yields hold steady while short-term rates begin to settle following earlier policy shifts.

The yield is the amount of money a bond earns for an investor. People often get confused between the interest rate and the yield, but in the market, they are two different things.

The Bond Basics

Imagine you lend $100 to the government. This $100 is called the Principal. The government gives you a piece of paper (or a digital record), which is the Bond. They promise to give your $100 back in ten years.

How Yield is Different from Interest

The government sets a fixed interest rate when they first sell the bond. This is called the Coupon. If the coupon is 5%, you get $5 every year.

The Yield is different because bonds can be traded like stocks. If you sell your bond to someone else for $90 instead of $100, the yield changes. The person who bought it still gets the $5 interest, but because they paid less for the bond, their "yield" (actual return) is now higher than 5%.

The Seesaw Rule: Prices vs. Yields

Bonds work like a seesaw. This is the most important rule in the bond market:

- When the Price of a bond goes up, the Yield goes down.

- When the Price of a bond goes down, the Yield goes up.

Why Do Bond Yields Change?

In early 2026, we are seeing yields move for three main reasons:

- Central Bank Interest Rates: Banks like the Reserve Bank of India or the Federal Reserve set "base rates." In February 2026, the RBI held rates steady at 5.25%. When central banks raise rates, old bonds with lower interest become less attractive, causing their prices to drop and yields to rise.

- The Role of Inflation: Inflation is when things like milk and bread get more expensive. If inflation is high, the $5 you get from a bond buys fewer things. Investors demand a higher yield to make up for this loss of "buying power."

- Government Borrowing: If a government needs to borrow a lot of money for big projects, they must offer a better deal to attract buyers. This extra supply of bonds can push yields higher.

Why Should You Care About Yields?

Even if you don't own a bond, yields touch your life in two big ways:

- Loans and Mortgages: Banks look at government bond yields to decide how much to charge you for a loan. When the 10-year bond yield goes up, fixed-rate mortgage rates usually follow.

- Savings and Retirement: Most pension funds hold government bonds. When yields are high, these funds can grow faster, potentially leading to better retirement payouts.

The "Yield Curve" Explained Simply

A Yield Curve is a graph that shows the yields of bonds that last for different amounts of time (like 2 years, 10 years, or 30 years).

- Normal Curve: Usually, you get a higher yield for lending money for 30 years than for 2 years because there is more "time risk."

- Inverted Curve: This happens when short-term yields are higher than long-term yields. It is often seen as a warning sign of an economic slowdown.

Market Update (Feb 2026): Currently, India's 10-year G-Sec yield is hovering around 6.67% – 6.70%. Analysts describe the curve as "steepening" slightly as long-term yields hold steady while short-term rates begin to settle following earlier policy shifts.