Difference Between Zero Coupon and Deep Discount Bonds: 2026 Investor Guide

Lock in long-term wealth by mastering the mechanics of discounted debt instruments.

- Understand why these bonds are sold far below their face value

- Compare deep discount bonds vs zero coupon bonds for retirement planning

- Learn how "phantom income" affects your 2026 tax filings

- Discover high-yield opportunities in the infrastructure and government sectors

Need to Understand Deep Discount Bonds vs Zero Coupon Bonds?

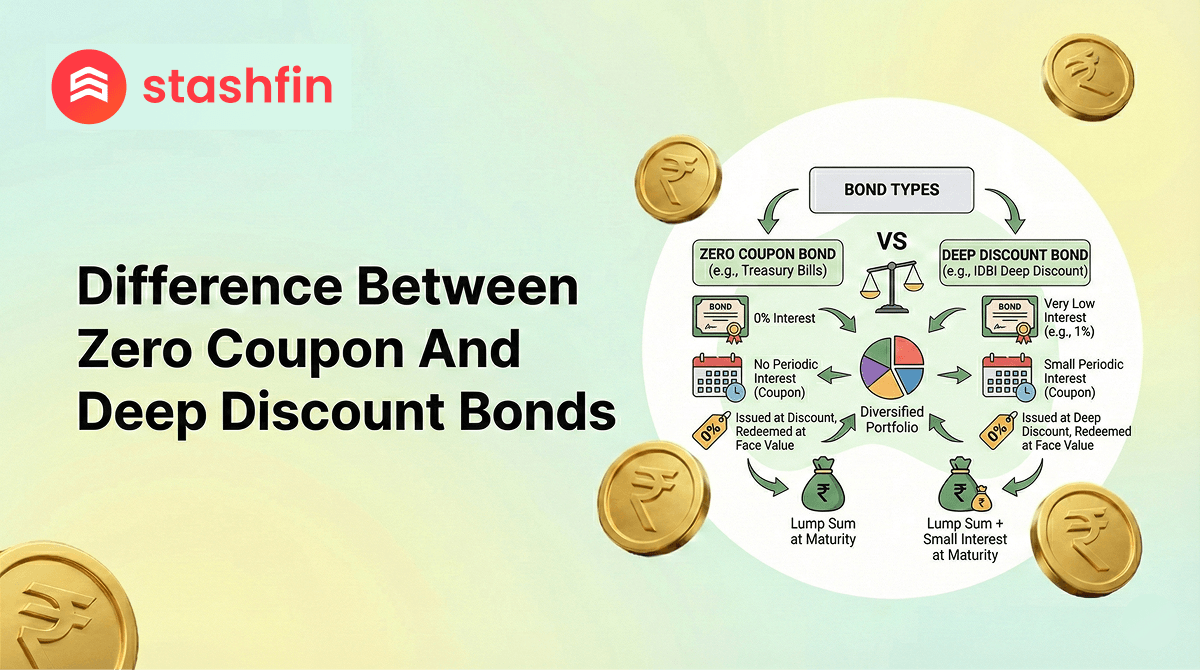

In a fluctuating interest rate environment like 2026, many investors are turning to "discounted" securities to avoid reinvestment risk. While they appear identical at first glance—both are sold at a discount and pay a lump sum at maturity, the nuances in their structure are vital.

- Zero Coupon Bonds (ZCBs) are the pure form of this instrument. They pay zero periodic interest. Your entire profit is the difference between the low purchase price and the full face value at the end.

- Deep Discount Bonds (DDBs) are technically a sub-type of zero-coupon bonds but are defined by the scale of the discount (typically 20% or more) and their much longer tenures, often spanning 15 to 25 years.

While every DDB is a type of zero-coupon instrument, a ZCB can be a short-term tool (like a 91-day T-Bill), whereas a DDB is almost always a long-term play.

Features and Benefits of Zero Coupon and Deep Discount Bonds

In 2026, these bonds are favored by investors who want to "set and forget" their money. Here is why the deep discount bonds vs zero coupon bonds category is growing:

- Elimination of Reinvestment Risk: Since there are no periodic coupons to reinvest, you don't have to worry about falling interest rates affecting your future returns.

- Predictable Lump Sums: You know exactly how much you will receive on the maturity date, making them ideal for funding a child's education or a retirement fund.

- Low Initial Capital: Because of the "deep discount," you can buy a bond with a high future face value for a fraction of the cost today.

- Portfolio Stability: These bonds are less affected by short-term market noise, though they are highly sensitive to long-term interest rate shifts.

- High Yield to Maturity (YTM): For those holding until the end, these instruments often offer superior internal rates of return (IRR) compared to traditional coupon-paying bonds.

Why Understanding Deep Discount Bonds vs Zero Coupon Bonds Matters

The fundamental difference between zero coupon and deep discount bonds lies in the maturity duration and the "steepness" of the discount.

| Feature | Zero Coupon Bonds (ZCB) | Deep Discount Bonds (DDB) |

|---|---|---|

| Periodic Interest | Strictly Zero. | Usually Zero (can sometimes be "minimal"). |

| Discount Scale | Can be small (e.g., 2% for T-Bills). | Significant (Usually 20% to 80% below par). |

| Investment Tenure | Short-term (T-Bills) to Long-term. | Primarily Very Long-term (10–30 years). |

| Typical Issuers | Central Banks (RBI), Governments. | Infrastructure Firms, NABARD, PSUs. |

| Taxation Concept | Often treated as Capital Gains at maturity. | May involve "Accrued Interest" tax annually. |

| Sensitivity | Moderate to High. | Extreme (Highest duration risk in bonds). |

Eligibility and Documentation for 2026 Investors

Investor Profile

To invest in these discounted instruments, you generally need to meet the following:

- Investor Type: Resident Individuals, NRIs (for government bonds), and Corporates.

- KYC Status: Fully updated PAN and Aadhaar linked to your brokerage.

- Financial Goal: Best suited for those who do not require monthly or quarterly income.

Documentation

The investment process is streamlined for the 2026 digital era:

- Demat Account: Essential, as most corporate DDBs are issued in electronic format.

- Trading Account: To purchase existing units on the secondary market.

- Bank Mandate: For the final "bullet payment" of the face value at maturity.

How to Invest: A Step-by-Step Guide

- Identify the Goal: Determine if you need the money in 1 year (ZCB/T-Bill) or 20 years (DDB).

- Evaluate Credit Rating: Since the payout is many years away, stick to AAA or AA+ rated issuers.

- Calculate YTM: Use the current market price and maturity date to find your true annual return.

- Execute via Exchange: Buy listed bonds through your trading terminal or participate in a fresh "New Fund Offer" (NFO).

Taxation & Charges for 2026

One of the most complex parts of the deep discount bonds vs zero coupon bonds debate is how the taxman views your profit.

| Type of Charge/Tax | Applicable Rule (2026) |

|---|---|

| Capital Gains Tax | For listed ZCBs, 12.5% on Long-Term Capital Gains (LTCG) if held over 12 months. |

| Imputed Interest | Some DDBs may require you to pay tax on "accrued interest" every year, even if you don't receive cash. |

| Brokerage Fees | Competitive rates (0.1% to 0.5% of transaction value). |

| Transaction Charges | Standard exchange fees (NSE/BSE). |