How Income Protection Insurance Works in India

What is Income Protection Insurance?

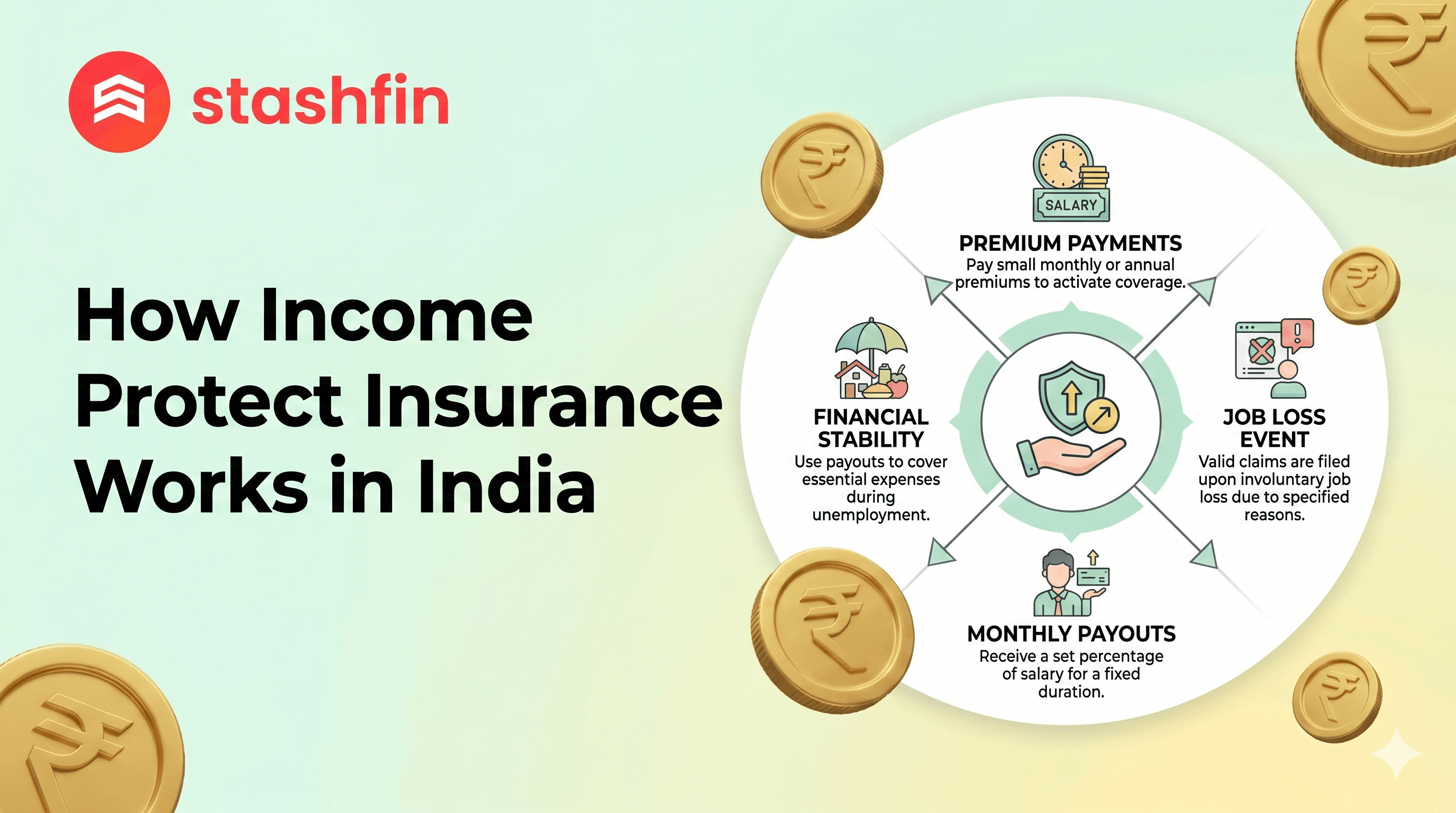

Income protection insurance is a plan that keeps money coming to you if you cannot work. In India, many people call this Salary Protection. It is like a safety net for your bank account.

If you get very sick or have an accident, you might stay home for a long time. During this time, your office might not pay you. Income protection insurance steps in to help. It gives you a part of your salary every month. This helps you pay for food, school fees, and rent.

The Difference Between Income Protection and Term Life Insurance

- Term Life Insurance: This pays money to your family only if you pass away.

- Income Protection: This pays money to you while you are still alive but unable to work.

How the Payout System Works

When you buy a plan, you decide how much money you need each month. Most plans in India cover about 75% to 100% of your take-home pay.

Monthly Income vs. Lump Sum

In 2026, most Indian workers choose Monthly Payouts. This feels like getting a regular salary. Some plans also offer a Lump Sum, which is one big bag of money all at once. This is better for paying off big bank loans (EMIs).

The Waiting Period (Deductibles)

You do not get money the very first day you fall sick. There is a Waiting Period. This is usually between 7 to 30 days. You must be unable to work for this long before the insurance company starts paying you.

What Does it Cover?

This insurance protects you against things that stop you from doing your job.

Illness and Accidental Disability

If a doctor says you cannot work due to a broken bone or a serious illness (like a heart attack), the policy starts. It covers both Temporary (short-time) and Permanent (forever) problems.

Involuntary Job Loss (Redundancy)

In 2026, many Indian plans now include Job Loss Cover. If your company closes down or lays you off, the insurance can pay your EMIs for 3 to 6 months while you look for a new job.

Note: It does not cover you if you quit your job on your own.

Eligibility and How to Apply

To get this insurance in India, you usually need to meet these rules:

| Criteria | Requirement |

|---|---|

| Age | 18 to 65 years old |

| Employment | Regular job or registered business (Self-employed) |

| Minimum Income | ₹25,000 per month |

| Documents | PAN Card, [Aadhaar Redacted], and 3 months' salary slips |

If you need immediate funds to manage expenses during the waiting period, you can apply for a Personal Loan to bridge the gap.

Why You Need It in 2026

Life is getting expensive. If your income stops for even two months, it can be hard to pay for:

- Home Loans: Banks still want their money every month.

- School Fees: Your children’s education should not stop.

- Medical Bills: Being sick costs a lot of money in 2026.

Having this plan means you can focus on getting better instead of worrying about money.