Difference Between Interest Paid and Interest Accrued

Understanding the gap between your paper obligations and your actual cash flow.

- Master the accrued interest meaning for better accounting

- Differentiate between actual cash outflows and periodic obligations

- Learn how interest timing impacts your tax liability in 2026

- Optimize your debt management and investment tracking

What is Accrued Interest?

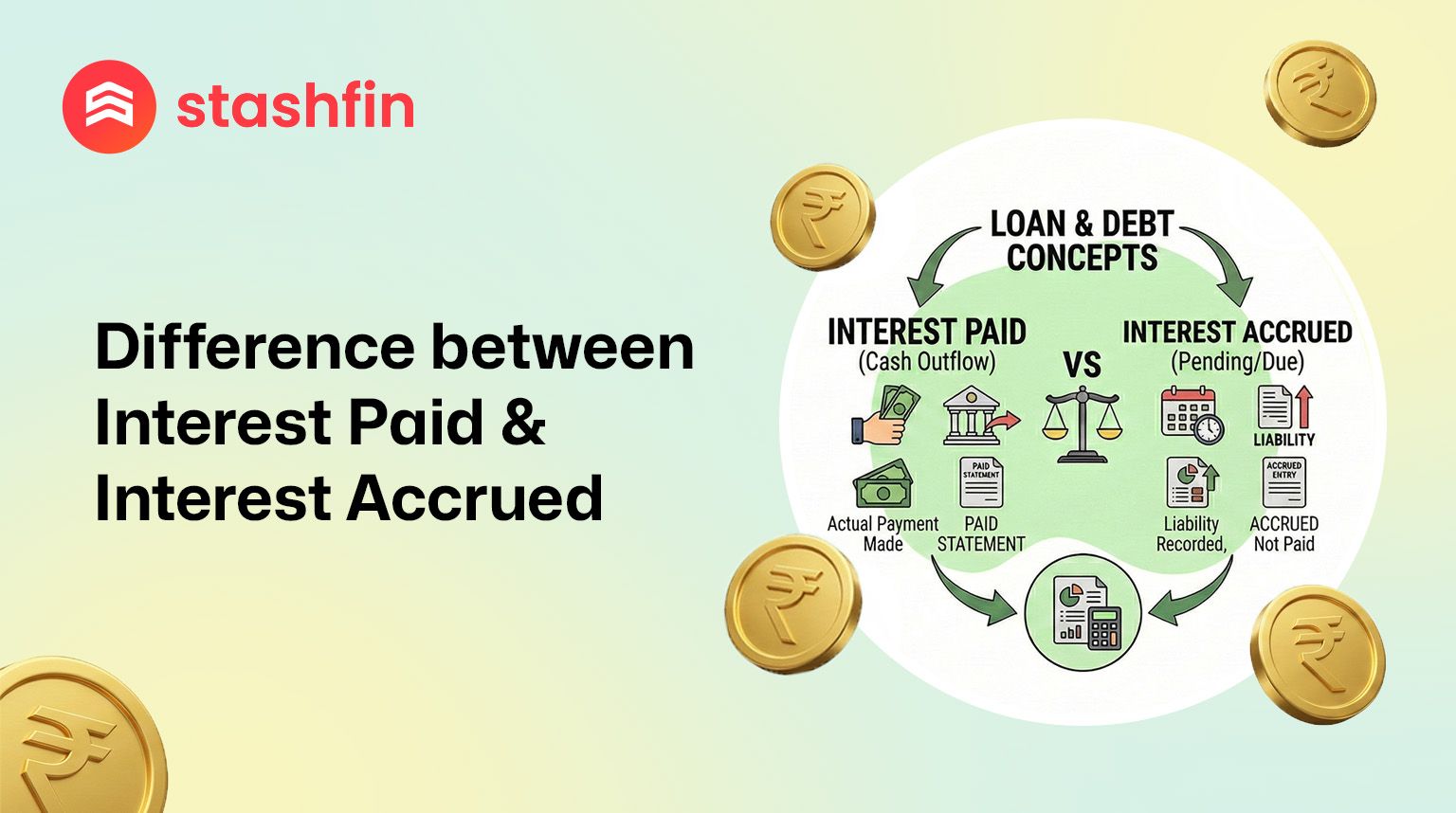

In the world of accounting and personal finance, the timing of a payment is just as important as the amount itself. The difference between interest paid and interest accrued often boils down to a matter of "now" versus "later."

- Interest Accrued represents the interest that has been earned or incurred but has not yet been paid or received. It is an obligation that is "building up" on the balance sheet.

- Interest Paid refers to the actual movement of cash. It is the moment the money leaves your bank account (as a borrower) or enters it (as a lender).

For businesses, this distinction is the foundation of Accrual Basis Accounting, ensuring that expenses match the period in which they occurred, regardless of when the check was cut.

Features and Benefits of Tracking Interest Paid vs Interest Accrued

When you correctly identify the difference between interest paid and interest accrued, you gain a more accurate picture of your financial health. Here is why distinguishing between them is so valuable:

- Accurate Financial Reporting: Ensure your profit and loss statements reflect true costs incurred during a specific month.

- Effective Tax Planning: Depending on your jurisdiction, you may be able to claim deductions on interest accrued even before it is paid.

- Better Cash Flow Management: Anticipate future "Interest Paid" events by tracking how much interest is currently accruing on your loans.

- Investment Clarity: For bondholders, understanding accrued interest ensures you know exactly how much "earned income" you are entitled to if you sell a bond between payment dates.

- Transparency with Lenders: Understand how your daily interest is calculated on credit cards or mortgages to avoid "sticker shock" at the end of the billing cycle.

Why Understanding Interest Paid vs Interest Accrued Matters

The core difference between interest paid and interest accrued lies in the timing of the transaction. While one is an accounting entry, the other is a physical cash transaction.

| Feature | Interest Paid | Interest Accrued |

|---|---|---|

| Definition | The actual cash amount transferred to settle interest. | Interest that has accumulated but remains unpaid. |

| Cash Flow Impact | Immediate. Cash leaves or enters the account. | None. It is a "paper" entry until the due date. |

| Accounting Entry | Recorded in the Cash Book/Bank Statement. | Recorded as a Liability (Payable) or Asset (Receivable). |

| Timing | Occurs on specific payment dates (Monthly, Quarterly). | Occurs continuously over the life of the loan/investment. |

| Relevance | Critical for liquidity and daily budgeting. | Critical for profitability and long-term liability tracking. |

Understanding the Calculation Logic

Accrued Interest Meaning in Practice

Imagine you have a loan with a 12% annual interest rate, and payments are made once a year on December 31st. By the end of June, you haven't paid any interest yet, but you have accrued six months' worth of interest.

Documentation & Tracking

In a professional setting, tracking interest paid vs interest accrued requires specific documentation:

- Amortization Schedules: To see how much interest is scheduled to accrue each month.

- Bank Statements: To verify the actual interest paid.

- General Ledger: To record accrued interest as a "Current Liability."

How to Manage Interest Accruals and Payments

Managing your interest obligations in 2026 is simple if you follow these steps:

- Review Loan Terms: Identify if your interest is calculated daily, monthly, or annually.

- Monitor Accruals: Use a digital dashboard to see your "outstanding interest" building up in real-time.

- Schedule Payments: Set alerts for the date the "Accrued Interest" converts into "Interest Paid."

- Audit Statements: Cross-check your accrued interest against the actual amount debited from your account to ensure no overcharges.

Impact of Accrued Interest on Different Financial Products

| Product | Impact of Accrued Interest |

|---|---|

| Bonds | If you sell a bond mid-period, the buyer pays you the accrued interest since the last coupon. |

| Credit Cards | Interest accrues daily from the date of purchase if the full balance isn't paid. |

| Mortgages | Interest accrues throughout the month and is usually "paid" in arrears on the 1st of the next month. |

| Fixed Deposits | You may see interest "accrued" in your passbook even if it only hits your account at maturity. |