What Is Repo Rate? Everything You Need to Know

In the world of finance, few terms carry as much weight as the Repo Rate. If you have ever applied for a personal loan, managed a home loan EMI, or even tracked the interest on your savings account, you have been directly impacted by this figure. Set by the Reserve Bank of India (RBI), the Repo Rate is the "master key" that controls the flow of money in our economy.

Understanding how the Repo Rate works helps you time your borrowings, manage your debts, and make informed decisions about your credit line. In this guide, we break down the complexities of the Repo Rate and its real-world impact on your wallet in 2026.

Defining the Repo Rate

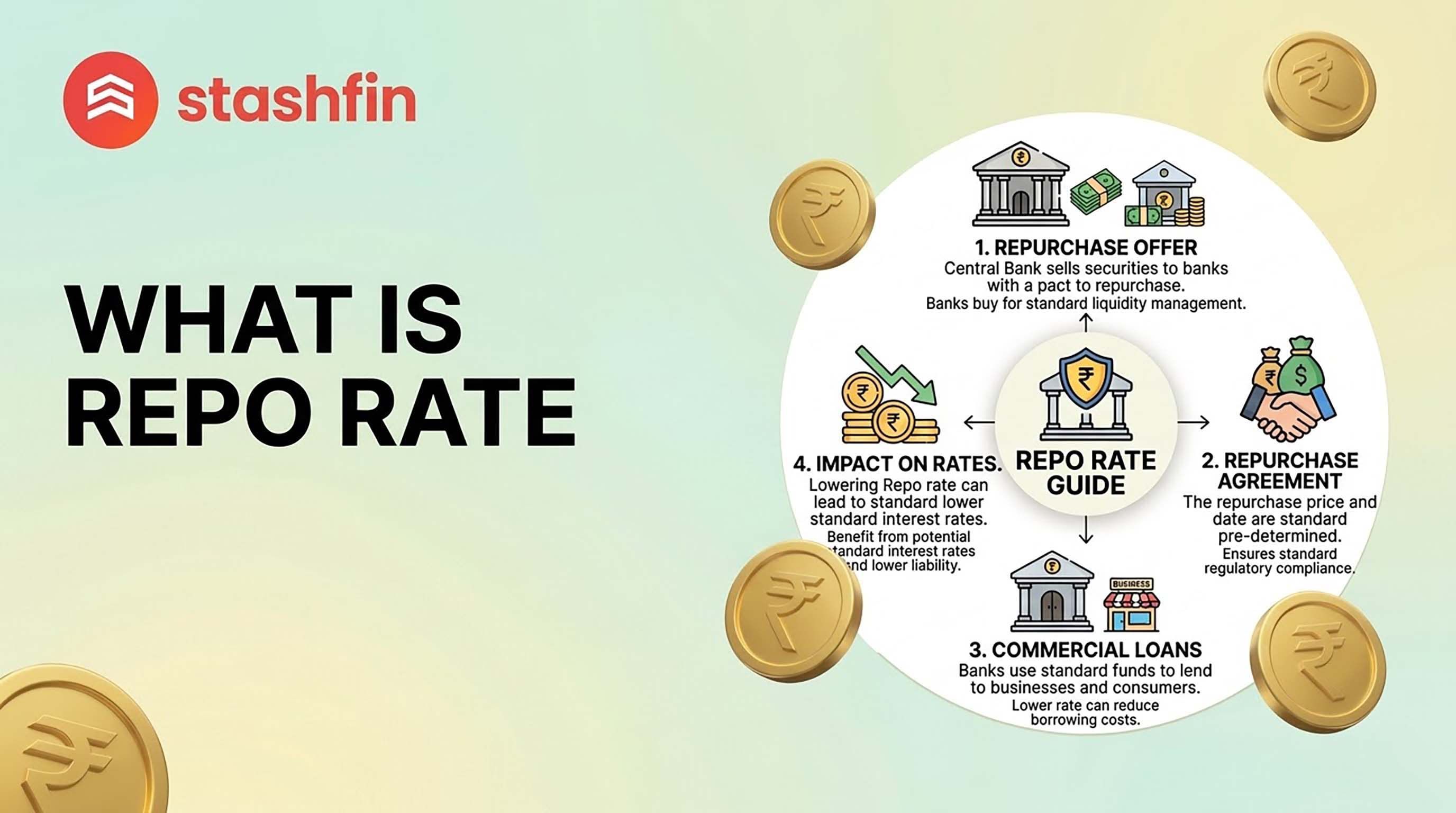

Repo Rate stands for Repurchase Option or Repurchase Agreement Rate. It is the interest rate at which the Reserve Bank of India (the central bank) lends money to commercial banks (like SBI, HDFC, or ICICI) when they face a shortage of funds.

Think of it as the "wholesale" price of money. Just as a shopkeeper buys goods at a wholesale price and sells them to you with a margin, commercial banks borrow from the RBI at the Repo Rate and then lend that money to you at a slightly higher interest rate.

How it Works: The Mechanism

When banks borrow from the RBI, they provide government securities as collateral. They agree to "repurchase" these securities at a later date at a predefined price. The difference between the loan amount and the repurchase price is effectively the Repo Rate.

Why Does the RBI Change the Repo Rate?

The RBI’s Monetary Policy Committee (MPC) meets every two months to review the Repo Rate. Their goal is to maintain a delicate balance between economic growth and inflation control.

1. To Control Inflation (Rate Hike)

When inflation is high (prices of goods are rising too fast), the RBI increases the Repo Rate.

- The Logic: Borrowing becomes expensive for banks, which in turn makes loans (Home, Car, Personal) expensive for you.

- The Result: People spend less, demand for goods drops, and prices eventually stabilise.

2. To Stimulate Growth (Rate Cut)

When the economy is sluggish or in a recession, the RBI decreases the Repo Rate.

- The Logic: Banks can borrow cheaply from the RBI and pass on those savings to you through lower EMIs.

- The Result: With cheaper credit available, people buy more houses, cars, and consumer durables, giving the economy a much-needed boost.

How Repo Rate Affects Your Personal Loan and EMI

In 2026, most retail loans are linked to an external benchmark, usually the Repo Rate itself. This is known as EBLR (External Benchmark Linked Rate).

The Direct Impact:

- Floating Rate Loans: If you have a home loan or a floating-rate personal loan, a Repo Rate hike means your EMI or your loan tenure will increase almost immediately.

- New Loan Applications: When the Repo Rate is low, it is the best time to apply for a Stashfin Credit or a personal loan, as you are likely to secure a lower interest rate.

- Fixed Rate Loans: These are generally unaffected by short-term Repo Rate changes, as the interest rate is locked in at the time of signing.

Repo Rate vs. Reverse Repo Rate

While they sound similar, they serve opposite functions in the banking ecosystem.

| Feature | Repo Rate | Reverse Repo Rate |

|---|---|---|

| Definition | Rate at which RBI lends to banks. | Rate at which RBI borrows from banks. |

| Purpose | To inject liquidity into the system. | To absorb excess liquidity from the system. |

| Impact | Higher rate makes loans expensive. | Higher rate encourages banks to park money with RBI. |

| Flow of Money | RBI $\rightarrow$ Commercial Banks | Commercial Banks $\rightarrow$ RBI |

The Broader Impact on the Economy

Beyond your personal EMIs, the Repo Rate influences:

- Fixed Deposits (FDs): When the Repo Rate rises, banks usually increase the interest rates on FDs to attract more deposits.

- Stock Market: Generally, the stock market reacts negatively to a Repo Rate hike because higher borrowing costs reduce corporate profits.

- Currency Value: Higher interest rates can often attract foreign investment, potentially strengthening the Indian Rupee against the Dollar.

Conclusion

The Repo Rate is much more than just a percentage in a news headline; it is a signal of the nation's economic health. For a borrower, it dictates the cost of dreams. For a saver, it determines the growth of their hard-earned money.

In 2026, staying updated on RBI's policy moves is essential. At Stashfin, we keep our processes transparent and our rates competitive, ensuring you always have access to affordable credit.