What Is CVV Number and How Does It Operate?

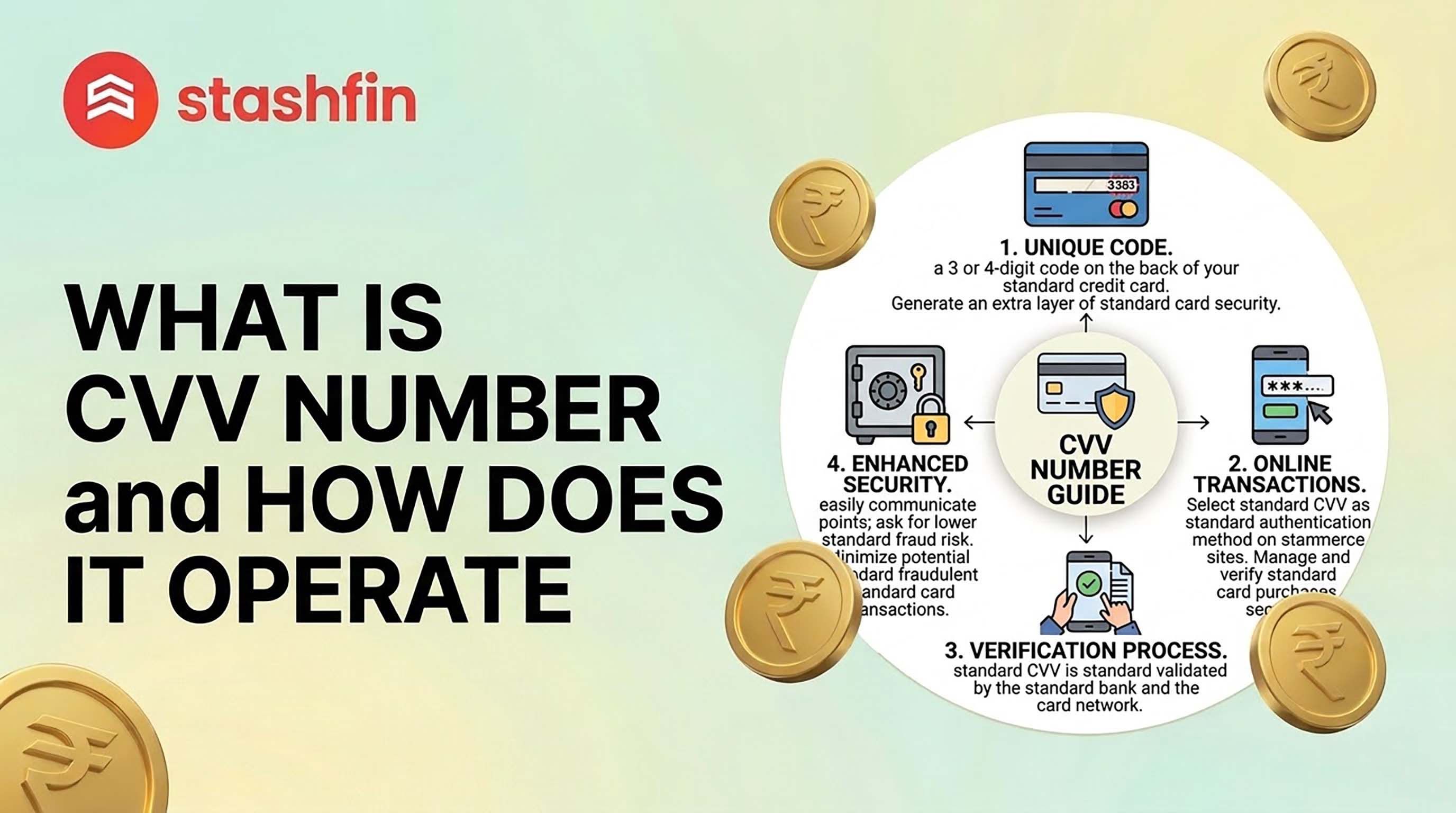

A CVV (Card Verification Value) is a specialized security code used primarily for "Card-Not-Present" (CNP) transactions, such as online shopping, phone orders, or mobile app payments. While your 16-digit card number and expiry date are often stored by browsers or merchant sites for convenience, the CVV is designed to be the final, physical proof that the person making the purchase actually has the card in their possession.

Decoding the Acronym: Is it CVV, CVC, or CID?

Depending on which card network you use, the name of this security code might change, even though the purpose remains the same:

- CVV / CVV2: Used by Visa.

- CVC / CVC2: Used by Mastercard.

- CID: Used by American Express (Amex) and Discover.

- CSC: A general term standing for Card Security Code.

Regardless of the name, these codes all serve as a "shared secret" between you and your bank to authenticate a transaction.

Where to Find Your CVV

In 2026, cards come in various designs—some physical, some metal, and some purely virtual.

- Visa, Mastercard, & RuPay: You’ll find a 3-digit CVV on the back of the card, usually printed in italics on or next to the white signature strip.

- American Express: The CVV (or CID) is a 4-digit number located on the front of the card, printed just above the main card number.

- Virtual Cards: If you use a virtual Stashfin card, your CVV is securely hidden within the app and can be viewed only after biometric authentication (fingerprint or face ID).

How the CVV Operates: The Security Workflow

The CVV isn't just a random number; it is generated using a complex cryptographic algorithm based on your unique card details. Here is how it operates during a typical online transaction:

- Input: You enter your card number, expiry, and the CVV on a payment gateway.

- Encryption: The gateway encrypts this data and sends a "verification request" to the card-issuing bank.

- Verification: The bank’s server runs the same algorithm. If the CVV you entered matches the one the bank has on record, the transaction is authorized.

- Instant Deletion: This is the most critical step. Under PCI DSS (global security standards), merchants are strictly prohibited from storing your CVV in their databases.

Why the CVV is Your "Last Line of Defense"

Even if a hacker manages to steal your card number and expiry date through a data breach at a major retailer, they usually cannot use that data for online fraud because they lack the CVV. Since the CVV is never stored by merchants, it is much harder to steal in bulk.

CVV vs. PIN: The Key Differences

Many people confuse the two, but they serve very different purposes:

| Feature | CVV Number | PIN (Personal Identification Number) |

|---|---|---|

| Length | 3 or 4 Digits | 4 or 6 Digits |

| Primary Use | Online / Phone (CNP) | ATM / Physical Stores (POS) |

| Storage | Printed on the card | Memorized by the user |

| Changeable? | No (Fixed for the card's life) | Yes (Can be reset at any time) |

Security in 2026: The Rise of Dynamic CVV (dCVV)

As we move deeper into 2026, static CVVs are slowly being replaced by Dynamic CVVs.

- How it works: Instead of a printed number, some high-security cards feature a small e-ink screen on the back that changes the CVV every 60 seconds or for every transaction.

- The Benefit: Even if someone sees your CVV today, it will be useless by the time they try to use it tomorrow.

Conclusion

The CVV number is a tiny detail with a massive responsibility. It bridges the gap between digital convenience and physical security. By understanding how it operates and why it should never be shared, you take a significant step toward securing your financial future.

At Stashfin, we believe in providing you with seamless credit and robust security. Whether you're making a high-value purchase or a small daily transaction, your CVV ensures that you remain the sole commander of your credit. Keep it private, stay alert, and continue to grow your financial dreams with confidence.