Comprehensive Guide to Infrastructure Bonds in 2026

What Are Infrastructure Bonds?

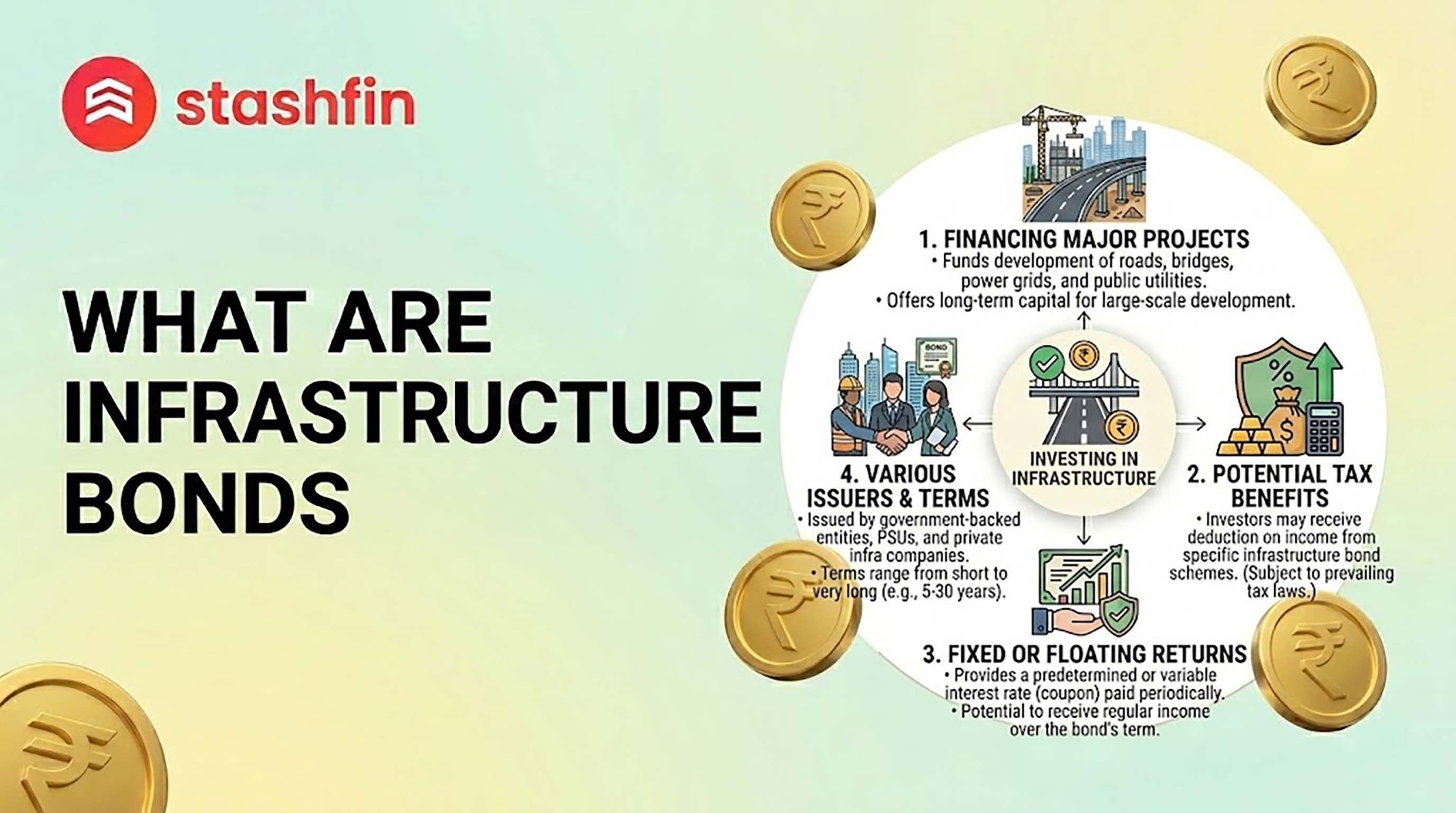

An Infrastructure Bond is a debt security issued by a government-authorized entity to raise capital specifically for the development of national infrastructure projects. When you buy these bonds, you are lending money to institutions like the National Highways Authority of India (NHAI), Indian Railway Finance Corporation (IRFC), or Power Finance Corporation (PFC).

In return, the issuer promises a fixed rate of interest (the coupon) at regular intervals and returns your principal at the end of the tenure. In 2026, these bonds are a "gold standard" for investors seeking higher safety than private corporate debt but better yields than traditional savings accounts.

How Infrastructure Bonds Work: The "Project-to-Payout" Cycle

Infrastructure projects like airports or power grids require massive upfront capital and take years to become profitable. These bonds bridge that gap:

- Issuance: A government-backed body (the "Issuer") announces a public issue of bonds.

- Deployment: Funds are funneled into projects defined under the "Infrastructure" category by the RBI.

- Revenue Generation: Once a project (like a toll road) is operational, the revenue generated is used to service the debt.

- Maturity: After the tenure (typically 10–15 years), you receive your final interest payment and your initial investment.

Key Features of Infrastructure Bonds in 2026

- Sovereign-Like Safety: Most are issued by PSUs with AAA or AA+ ratings. They are "Quasi-Sovereign" because the government is unlikely to let a national project fail.

- Higher Yields: In early 2026, while 10-year G-Secs yield around 6.5%–6.7%, certain infrastructure bonds offer 7.5% to 8.5%.

- Longer Tenures: These are long-term plays (10–15 years), ideal for retirement planning.

- Lock-in Periods: Tax-saving variants often have a mandatory 5-year lock-in, during which they cannot be traded.

The Tax Advantage: Section 80CCF & Beyond

Tax efficiency is a major draw for Indian professionals. Infrastructure bonds offer a unique edge, though the specific benefits depend on the bond type:

Section 80CCF (A Reality Check)

Note: Section 80CCF was a popular provision that allowed an additional deduction of up to ₹20,000 for notified infrastructure bonds. While many investors still look for this, it is important to note that the government has not issued new 80CCF-notified bonds in recent years. Always verify if a 2026 issuance is specifically "80CCF Notified" before investing for this extra deduction.

Tax-Free vs. Taxable Bonds

| Feature | Tax-Free Bonds | Taxable Bonds |

|---|---|---|

| Interest Tax | 100% Tax-Exempt | Taxed at your slab rate |

| Ideal For | High tax brackets (30%+) | Low tax brackets (5%–10%) |

| Coupon Rate | Lower (e.g., 5.5%–6.5%) | Higher (e.g., 7.5%–8.5%) |

| Effective Yield | Often beats FDs for HNIs | Predictable high-coupon income |

Why 2026 Is the Right Time to Invest

Following the Union Budget 2026-27, the government increased public capex to over ₹12 lakh crore. This surge has led to high-quality bond issuances.

- Falling Rate Protection: If the RBI cuts rates later in 2026, the fixed 8%+ coupons on existing bonds become more valuable (capital appreciation).

- Portfolio Anchor: In a volatile equity market, these bonds provide a "safe harbor" for your principal.

- Digital Ease: You can now buy these through the RBI Retail Direct portal or your stockbroking app in minutes.

Risks to Consider

- Liquidity Risk: Due to long tenures and lock-ins, these are illiquid. Don't invest emergency funds here.

- Inflation Risk: If inflation spikes, a fixed 7.5% return might lose real value. (Current 2026 inflation is stabilized around 2.75%–3%).

- Credit Risk: Rare for PSUs, but always check the latest CRISIL/ICRA rating rationale.

Conclusion

Infrastructure Bonds offer a rare combination of high safety, decent yields, and the satisfaction of building the nation’s backbone. In 2026, as the "Retail Era" of bond investing takes off, these are excellent tools for a secure financial future.

At Stashfin, we simplify your financial journey. While you invest for the long term in infrastructure, our Instant Credit Line ensures your daily liquidity needs are always met without touching your core savings.

Would you like me to help you compare the current yields of NHAI vs. IRFC bonds available on the secondary market?