What is the Cooling Off Period for a Personal Loan?

Flexibility, speed, and non-denomination of collaterals have made personal loans one of the most used types of credit in India. Personal loans have also shown a considerable rise in India in FY 2023, at an increase of more than 23%, and this indicates the increasing dependency of individuals on these types of credit lines to cater to an immediate, urgent financial requirement. However, most borrowers in a hurry to get funds fast do not consider an essential aspect of taking a loan, which is the cooling off period.

The cooling off period is both a legally and morally significant step in the process where the borrowers have a limited time to change their minds and get out of the deal without any big penalty. It is a form of protection to ensure people make no rushed or uninformed credit decisions.

In this blog, we are going to give you a clear answer: “What is the cooling off period for a personal loan,” why it has been established, what its advantages are, and how you, as a borrower, can utilize it to benefit your financial well-being. When thinking of getting a loan, particularly one on the internet or by using a fintech app, learning the meaning of the term might save you money and a headache in the future.

What is Cooling Off Period in Loans?

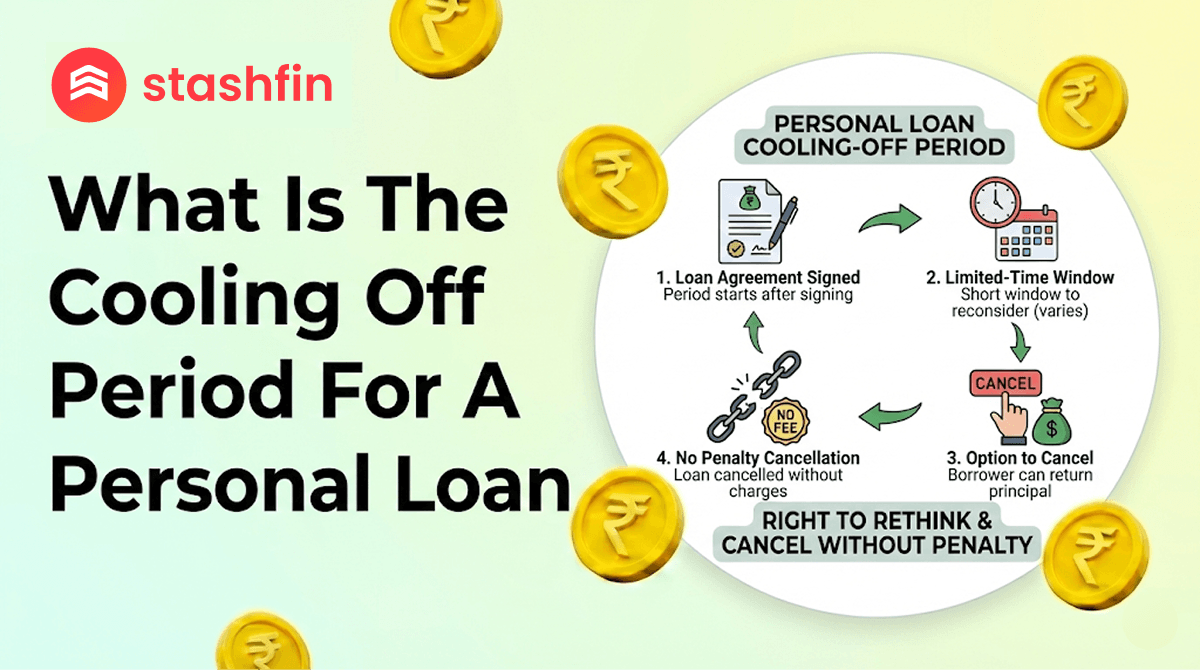

The cooling off period of a personal loan is a small window of opportunity that is allowed to a borrower when a loan is sanctioned, within which he can call off the loan without having to incur heavy penalties or face legal action. This is meant to safeguard the consumers, especially those who might have made a decision to borrow a loan on impulse or when compelled under duress.

Here are some important aspects to know:

- Typically ranges from 24 hours to 7 days, depending on the lender.

- Allows loan cancellation without major penalty if requested within the timeframe.

- Must be clearly mentioned in the loan agreement or terms and conditions.

Why is a Cooling Off Period Important?

Now that you know what is the cooling off period for a loan, let us look at the “WHY.” The cooling off period in loans ensures that borrowers have time to reflect on the loan agreement and assess whether they can manage the repayments. It also helps prevent fraud and manipulation by giving users a buffer period to review the full loan documentation.

Reasons why it matters:

- Reduces buyer’s remorse in rushed or pressured loan signings.

- Offers protection from predatory lending practices.

- Enables better financial planning without the pressure of long-term EMIs.

What is the Process for Loan Cancellation?

If a borrower chooses to cancel their loan during the personal loan cooling off period, there is a defined process to follow. This can vary slightly depending on the bank, NBFC, or fintech lender.

Here are the general steps:

- Contact the lender’s customer support within the defined window.

- Submit a formal cancellation request via email or the app portal.

- Ensure you return the disbursed loan amount, if already credited, usually without interest if within the cooling off period personal loan.

- Receive written confirmation of loan cancellation from the lender.

Key Things to Remember Before Cancelling a Loan

Before you decide to cancel a loan using the cooling off period for a personal loan, there are several factors to consider. These can affect your credit report, repayment options, and future loan eligibility.

Important considerations:

- Review all loan documents and terms, including cancellation clauses.

- Assess how far the loan process has gone — if disbursed, immediate repayment might be required.

- Know that cancelling a loan may leave a soft footprint on your credit report, especially if credit checks were conducted.

Is Cooling Off Period Available for All Loans?

Not all loans offer a cooling off period, and the availability often depends on the lender’s internal policies or the type of loan offered. It is more commonly seen in digital lending, NBFCs, or platforms aligned with RBI fair practices.

Here’s what to know:

- Banks and regulated NBFCs may or may not offer a cooling period explicitly.

- Online lenders and apps often provide a window as part of their consumer-friendly approach.

- Always read the loan agreement thoroughly to verify this clause before signing.

What is the Impact of Loan Cancellation on Credit Score

While cancelling a personal loan during the loan cooling period may seem like a clean break, it can still leave a mark on your credit history, depending on how far the process has gone.

Impacts include:

- No impact if a loan wasn’t disbursed or recorded by the credit bureaus.

- Minor impact if the loan was disbursed and then repaid, as repayment will be noted.

- Inquiries made during the application still count towards your credit inquiry history.

To avoid any misunderstanding, always ensure the loan is cancelled with written confirmation and that the lender updates their records with the credit bureau accordingly.

Cooling Off Periods Offer Protection When Used Smartly

At StashFin, we believe in empowering our users with financial knowledge that supports better decisions. The cooling off period for personal loans is one such consumer right that gives borrowers a chance to pause, think, and walk away if they’re not confident about repaying the loan. While not all institutions offer it, we ensure transparency at every stage of the lending journey so that you’re never left in the dark.

Whether it’s a small personal loan to get through the month or a larger one for major expenses, always read the terms, use your cooling off rights wisely, and borrow only what you can repay. With the right approach, personal loans can be a smart financial tool—and StashFin is here to help you use them responsibly.