What Is NCD? (Non-Convertible Debentures)

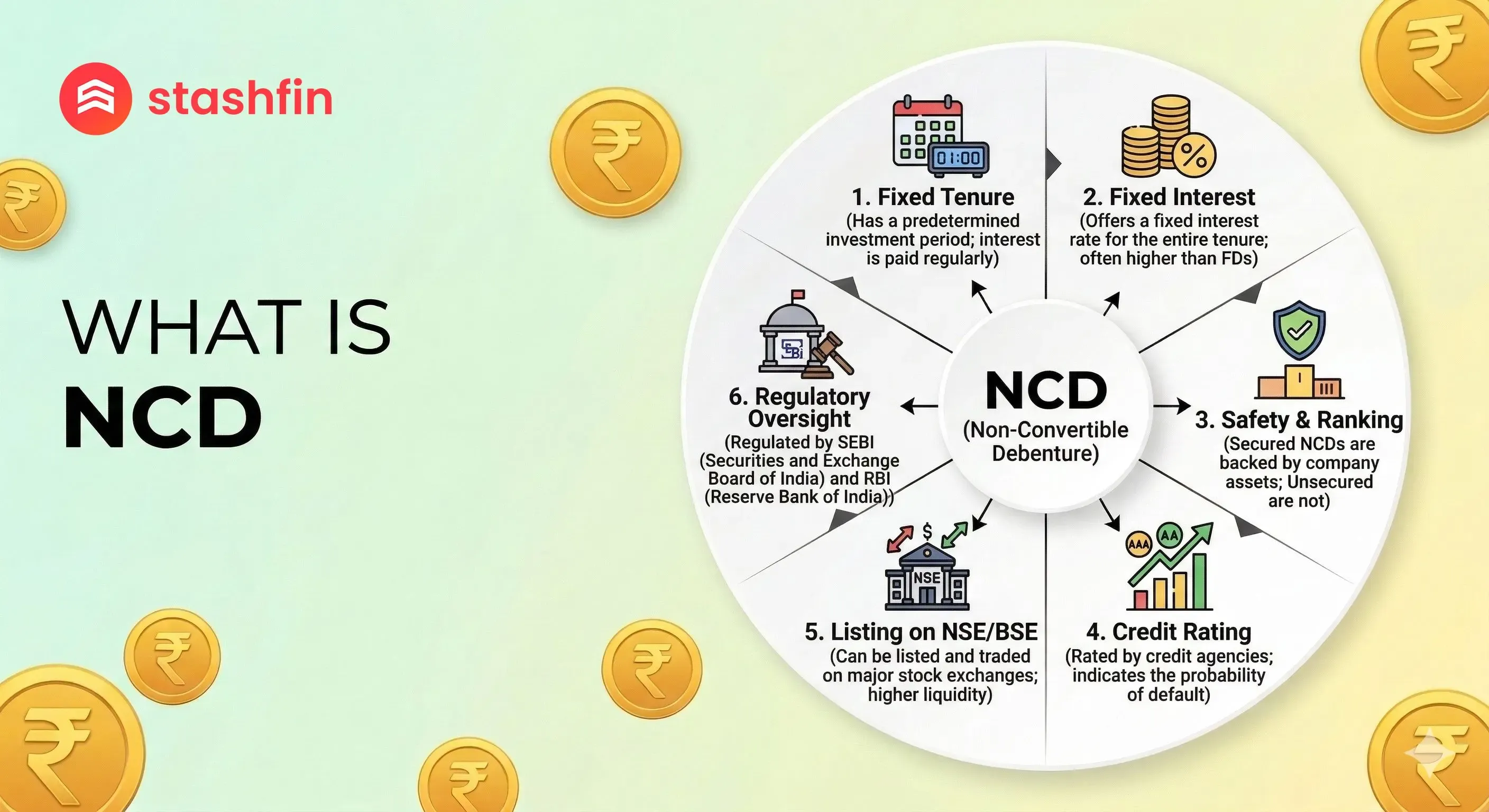

A Non-Convertible Debenture (NCD) is a fixed-income debt instrument issued by corporations to raise long-term capital from the public. Unlike "Convertible Debentures," which can be turned into equity shares after a certain period, NCDs remain as debt throughout their life. They cannot be converted into shares, and in return for this "non-convertibility," they typically offer higher interest rates than their convertible counterparts.

In simple terms, when you buy an NCD, you are lending money to a company. In exchange, the company promises to pay you a fixed rate of interest (called a "coupon rate") for a predetermined tenure and return your principal amount upon maturity.

Key Features of NCDs in 2026

In the current market, NCDs are favored for several structural advantages:

- Fixed Interest Income: You receive periodic interest payouts—monthly, quarterly, annually, or as a cumulative lump sum at maturity.

- Credit Ratings: Every NCD issue is rated by agencies like CRISIL, ICRA, or CARE. A rating of AAA or AA+ indicates high safety, helping you gauge the risk before you invest.

- Liquidity: Most NCDs are listed on stock exchanges like the NSE or BSE. This means you can sell your NCDs in the secondary market if you need funds before the maturity date.

- No Ownership Dilution: Since these don't convert to shares, the company's ownership remains unchanged, which is why reputed firms prefer this route for raising funds.

Types of NCDs: Secured vs. Unsecured

When exploring NCDs on the Stashfin app or through your broker, you will encounter two primary categories:

A. Secured NCDs (The Safer Route)

Secured NCDs are backed by the company's assets (like property or machinery). If the company fails to repay, these assets can be liquidated to pay back the investors. Because they offer a safety net, their interest rates are slightly lower than unsecured ones.

B. Unsecured NCDs (The High-Yield Route)

These are not backed by any specific collateral. Your investment relies entirely on the creditworthiness and reputation of the issuing company. To compensate for this higher risk, unsecured NCDs offer significantly higher interest rates.

NCDs vs. Bank Fixed Deposits (FDs)

Why are investors moving away from FDs toward NCDs in 2026? Let’s look at the numbers:

| Feature | Bank Fixed Deposit (FD) | Non-Convertible Debenture (NCD) |

|---|---|---|

| Returns | Generally 6.5% – 7.5% p.a. | High: 8.5% – 11.5% p.a. |

| Safety | High (DICGC Insured up to ₹5L) | Moderate (Depends on Credit Rating) |

| Liquidity | Penalty on early withdrawal | Tradable on stock exchanges |

| Taxation | TDS applicable on interest | No TDS for listed NCDs in Demat |

Taxation on NCDs (Post-2026 Budget Updates)

Understanding the tax impact is crucial for calculating your "real" returns. Following the New Income Tax Act of 2025 (effective April 2026), here is the simplified tax structure:

- Interest Income: Interest earned is added to your total income and taxed at your applicable income tax slab rate.

- Capital Gains:

- STCG: If you sell your NCD on an exchange before 12 months, it's considered Short-Term Capital Gain and taxed at your slab rate.

- LTCG: If sold after 12 months, it's Long-Term Capital Gain, taxed at 12.5% without indexation.

- TDS Advantage: One major benefit is that No TDS is deducted on interest payments for listed NCDs held in a Demat account, ensuring you receive the full cash flow to manage your liquidity.

Conclusion

Non-Convertible Debentures (NCDs) are a powerful middle ground for investors who find bank FDs too low-yielding but find the stock market too volatile. They offer the predictability of fixed income with the added bonus of inflation-beating returns.

In 2026, the key to successful NCD investing is Credit Quality. Always prioritize AAA or AA rated issues from reputed companies. By adding NCDs to your portfolio, you ensure a steady stream of passive income while keeping your capital relatively secure.