What is Maturity Date?

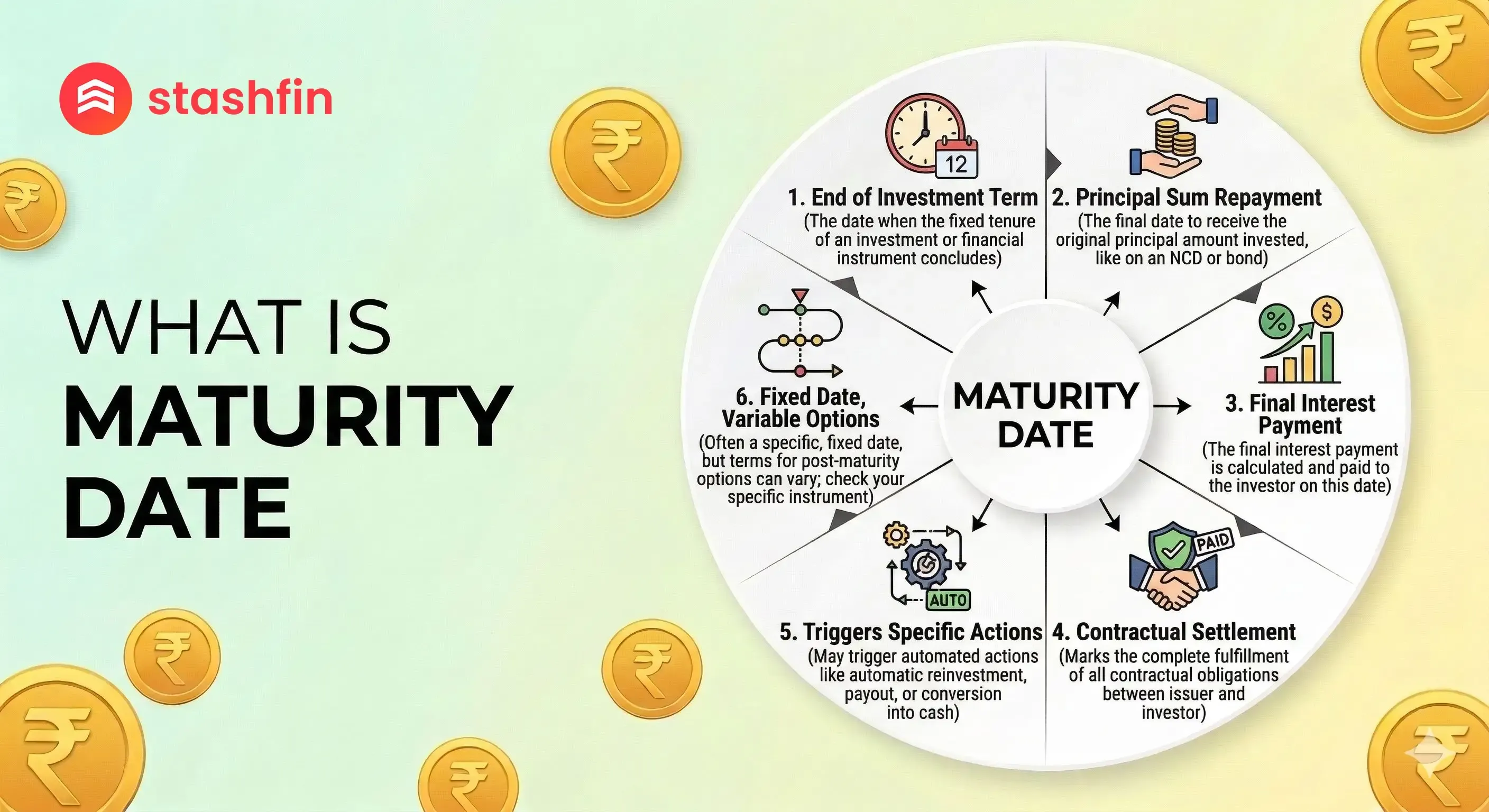

In simple terms, the Maturity Date is the specific day on which a financial agreement ends. It is the date when the "life" of a financial instrument, such as a loan, bond, or term deposit, expires, and the final settlement is due.

- For Borrowers: It is the deadline by which the loan must be fully repaid, including all principal and interest.

- For Investors: It is the day you receive your original investment (principal) back, along with any final interest earnings.

How Maturity Dates Work Across Financial Products

In 2026, the maturity date functions as a trigger for different actions depending on the product you hold. Let’s break down its role in the most common financial instruments:

A. Personal Loans and Mortgages

In the context of a Stashfin Personal Loan, the maturity date is the day your final EMI is due. Once this payment is successfully processed, your debt is officially "mature" or paid in full. At this point, the lender usually issues a No Objection Certificate (NOC), confirming that you have no further liabilities.

B. Fixed Deposits (FDs)

When you open an FD, the maturity date is fixed at the start. On this day, the bank releases the funds into your savings account.

Note: Many banks in 2026 offer "Auto-renewal." If you don't take action on the maturity date, your money might be locked in for another term at the current prevailing interest rate, which may not always be in your favor.

C. Bonds and NCDs (Non-Convertible Debentures)

For debt instruments like bonds or NCDs, the maturity date is when the issuing company or government must pay you the "Face Value" of the bond. Until this date, you might receive periodic interest (coupons), but the bulk of your capital returns only at maturity.

Classifying Maturity: Short-Term vs. Long-Term

Maturity dates help classify financial products into three main categories. Choosing the right one depends on your liquidity needs and risk appetite.

| Category | Tenure | Examples | Ideal For... |

|---|---|---|---|

| Short-Term | Less than 1 Year | Treasury Bills, 6-Month FDs | Immediate needs & high liquidity. |

| Medium-Term | 1 to 5 Years | Personal Loans, Corporate NCDs | Intermediate goals like a wedding. |

| Long-Term | 5 to 30 Years | Home Loans, PPF, Govt Bonds | Retirement or wealth creation. |

Why the Maturity Date is Critical for Your Financial Health

The maturity date is more than just a "due date"; it is a strategic data point for your financial planning.

- Cash Flow Management: Knowing exactly when a loan ends or an investment pays out allows you to plan future expenses without taking on unnecessary new debt.

- Credit Score Impact: For borrowers, the maturity date is the "deadline for discipline." If a loan is not settled by its maturity date, it can be marked as "Defaulted" on your credit report, which can slash your CIBIL score.

- Interest Rate Risk: For investors, longer maturity dates often mean higher interest rates. However, they also carry "Interest Rate Risk"—if market rates rise while your money is locked in, you miss out on higher returns elsewhere.

[Image showing the relationship between bond maturity length and interest rate risk]

Can a Maturity Date Change?

While most maturity dates are "fixed," certain financial structures in 2026 allow for flexibility:

- Prepayment: Many borrowers choose to pay off their loans before the maturity date to save on interest. At Stashfin, we offer Zero Foreclosure Charges on many products to support this.

- Callable Bonds: Some bonds have a "Call Option," where the issuer can pay you back and end the contract before the official maturity date if interest rates drop.

- Loan Extensions: In some cases of financial hardship, lenders may agree to extend the maturity date (restructuring), though this usually increases the total interest paid.

Conclusion

The maturity date is the finish line of your financial journey with a specific product. Whether you are counting down the days until your last EMI with Stashfin or waiting for a high-yield NCD to pay out, understanding this date ensures you are never caught off guard.

In 2026, the smartest financial move you can make is to mark your maturity dates in red. Be proactive, plan for the cash inflow or outflow, and ensure your money is always working toward your next big goal.