What is G-Sec & State Guaranteed Bond?

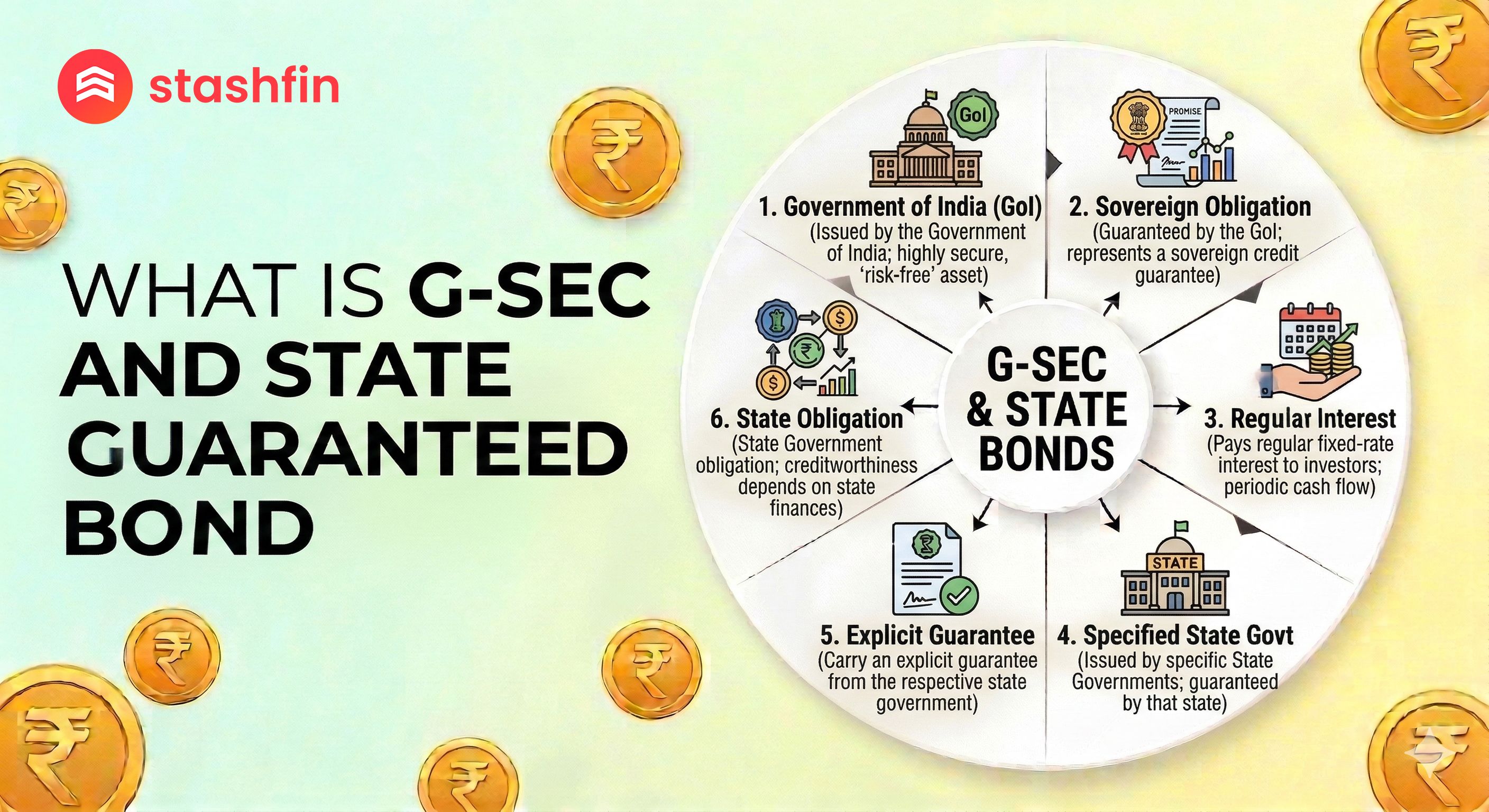

G-Secs (Government Securities) are debt instruments issued by the Central Government of India to fund its fiscal needs, like building highways, upgrading the military, or managing the national budget. Because they are issued by the sovereign power, they carry the highest level of safety (zero default risk).

State Guaranteed Bonds (often categorized under State Development Loans or SDLs) are debt instruments issued by State Governments. While they function similarly to G-Secs, they are used to fund state-specific development projects, such as irrigation, education, or state-run infrastructure. These bonds are "guaranteed" by the respective state, offering a robust layer of security and often a slightly higher interest rate than central bonds.

Deep Dive into G-Secs: The Sovereign Standard

In 2026, the Reserve Bank of India (RBI) has made G-Secs incredibly accessible to everyday investors through the RBI Retail Direct portal.

Key Features of G-Secs:

- Negligible Credit Risk: Since the Central Government has the power to tax and manage currency, the risk of default is practically non-existent.

- Regular Income: Most "Dated Securities" pay a fixed interest rate (coupon) every six months.

- High Liquidity: G-Secs are the most liquid part of the Indian debt market. You can sell them easily in the secondary market.

- Tenure Variety: You can choose a "short-term" T-Bill (91 days) or a "long-term" bond (up to 40 years).

Understanding State Guaranteed Bonds (SDLs)

State Development Loans (SDLs) are the primary way states like Maharashtra, Tamil Nadu, or Uttar Pradesh raise money.

Why Choose State Bonds Over Central Bonds?

- The "Yield Spread": In 2026, SDLs typically offer an interest rate that is 0.50% to 1.00% higher than G-Secs of the same tenure.

- State Guarantee: While technically "state-backed," the RBI manages the debt servicing. Interest and principal are deducted directly from the state’s account with the RBI, ensuring high repayment certainty.

- Portfolio Diversification: Investing in SDLs allows you to bet on the growth of specific high-performing states while keeping your capital secure.

Comparison: G-Secs vs. State Guaranteed Bonds

| Feature | Central G-Secs | State Guaranteed Bonds (SDLs) |

|---|---|---|

| Issuer | Government of India (Central) | State Governments |

| Safety Level | Sovereign (Zero Risk) | Sovereign-Equivalent (Very High) |

| Interest Rate | Benchmark (Base Rate) | Higher (Spread of 0.5% - 1%) |

| Tenure | Up to 40 Years | Typically 5 to 30 Years |

| Liquidity | Very High | Moderate to High |

| Ideal For | Capital Preservation | Regular High-Interest Income |

[Image comparing the yield curve of Central Government G-Secs vs State Development Loans]

How to Invest in 2026: The Digital Way

In 2026, a retail investor can start with just ₹10,000 through several digital avenues:

- RBI Retail Direct: The official "one-stop shop" where you can open a Gilt Account for free and participate in primary auctions.

- Stock Exchanges (NSE/BSE): Use your existing demat account to buy G-Secs or SDLs through mainstream investment apps.

- Debt Mutual Funds: Invest in "Gilt Funds" or "SDL Funds" where professional managers handle the bond selection for you.

Taxation: What You Take Home

Under the Tax Laws of 2026, it is important to calculate your "post-tax" returns:

- Interest Income: Coupons are added to your total income and taxed at your applicable slab rate.

- Capital Gains: If sold on an exchange, gains are taxed at 12.5% (if held for over 1 year) or at your slab rate (if held for less than 1 year).

- Tax Benefit: There is No TDS (Tax Deducted at Source) on the interest earned from listed G-Secs held in demat form.

Conclusion

G-Secs and State Guaranteed Bonds represent the pinnacle of financial security in India. In 2026, they provide a much-needed anchor in a volatile world. G-Secs offer ultimate "peace of mind," while State Guaranteed Bonds provide that extra "yield" to beat inflation.

At Stashfin, we believe in a balanced financial life. While you use a Credit Line for your immediate liquidity, parking your long-term savings in government-backed bonds ensures your future is always on solid ground.