What is Effective Annual Rate (EAR)? The "True" Cost of Borrowing and Saving

If you’ve ever looked at a credit card statement and wondered why the interest feels much higher than the "15% per annum" advertised, you have likely encountered the difference between a Nominal Rate and the Effective Annual Rate (EAR).

In the financial world of 2026, transparency is everything. While banks often lead with a nominal rate to make loans look cheaper or savings look simpler, the EAR is the real number that dictates your wealth. It accounts for the "snowball effect" of interest, what we call compounding.

This guide demystifies EAR, explains the mathematics behind it, and shows you how to use it as a strategic tool for your personal finances.

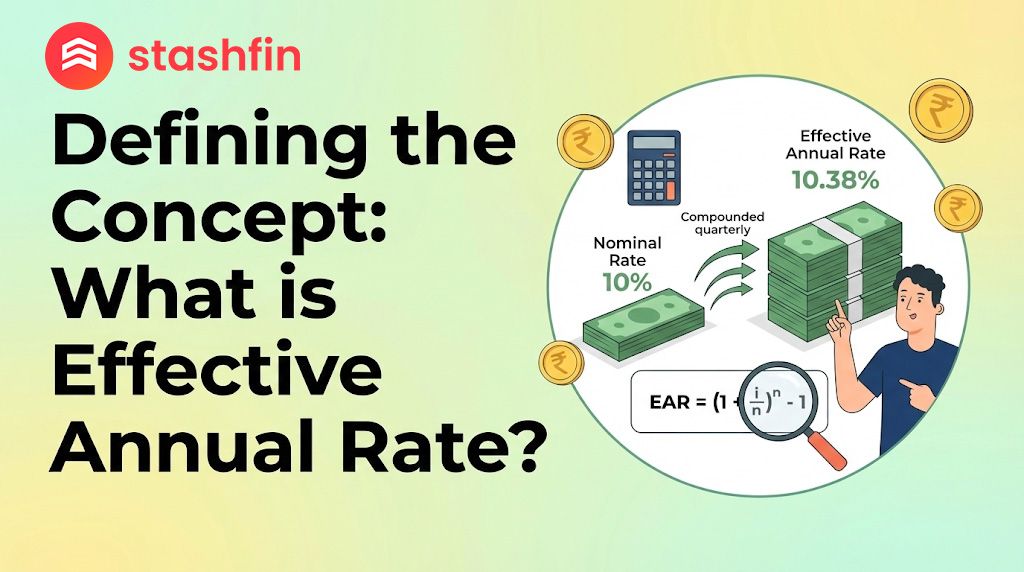

Defining the Concept: What is Effective Annual Rate?

The Effective Annual Rate (EAR) is the actual interest rate an investment or a loan earns (or costs) in a year after accounting for compounding.

Most financial products do not calculate interest just once a year. Instead, they compound it monthly, quarterly, or even daily. Every time interest is added to your principal, the next interest calculation is based on that new, higher amount. EAR captures this cumulative growth in a single, comparable percentage.

EAR vs. Nominal Interest Rate

- Nominal Rate (Stated Rate): This is the basic interest rate quoted by the bank. It does not account for compounding within the year.

- EAR: This is the "real-world" rate. If the compounding frequency is more than once a year, the EAR will always be higher than the nominal rate.

The Role of Compounding Frequency

The most important takeaway for any borrower or saver is that frequency matters. The more often interest compounds, the higher the EAR becomes, even if the nominal rate stays exactly the same.

| Compounding Frequency | Nominal Rate | Effective Annual Rate (EAR) |

|---|---|---|

| Annual (1x / year) | 10% | 10.00% |

| Semi-Annual (2x / year) | 10% | 10.25% |

| Quarterly (4x / year) | 10% | 10.38% |

| Monthly (12x / year) | 10% | 10.47% |

| Daily (365x / year) | 10% | 10.52% |

Why EAR is Critical for Your Financial Decisions

Understanding EAR isn't just a math exercise; it’s a survival skill for your wallet.

Comparing "Apples to Apples"

Lenders often use different compounding periods. One bank might offer a loan at 12% compounded monthly, while another offers 12.2% compounded annually. Without calculating the EAR, you might choose the 12% loan, but the EAR reveals that both are nearly identical. EAR provides a level playing field for comparison.The Credit Card Trap

Credit cards are notorious for daily or monthly compounding. A nominal rate of 36% per annum (3% per month) sounds expensive, but when you calculate the EAR with monthly compounding, it jumps to 42.57%. This is why credit card debt spirals so quickly.Maximising Savings

When choosing where to park your money, look for accounts that compound more frequently. A savings account with a slightly lower nominal rate but daily compounding might actually yield more than an account with a higher rate that only compounds annually.

EAR vs. APR (Annual Percentage Rate)

In the industry, these two terms are often used interchangeably, but there is a distinct difference that savvy users should know:

- APR (Annual Percentage Rate): Usually refers to the simple interest rate plus any extra fees or costs associated with the loan. However, APR does not account for compounding.

- EAR: Accounts for the effect of compounding within the year.

Key Rule: If you are borrowing, the EAR is the "truer" reflection of your cost. If you are investing, the EAR (sometimes called Annual Percentage Yield or APY) is the "truer" reflection of your gains.

The Bottom Line

In a world where financial products are becoming increasingly complex, the Effective Annual Rate is your best defense against "hidden" costs. By looking past the nominal rate and focusing on the EAR, you gain a clear, honest view of your financial commitments and opportunities.