What Are the Top Business Loan Rejection Reasons in 2025?

Securing a business loan can launch any business and open the floodgates of opportunities, such as expanding operations, hiring new hands, creating a viable infrastructure, or simply keeping the fire burning during a slow season. Very often, a loan is like a lifeline that turns a dream into a flourishing enterprise.

However, laying one's hands on this lifeline can be a grueling task.

A meticulous preparation of documents, with a strong application that will showcase your business idea as one of a kind, can often result in a flat rejection. At that point, all one can feel is a wave of dismay and utter confusion as to what really could have gone wrong.

The lending landscape has changed in 2025. Both the traditional banks and the digital lenders are becoming increasingly selective. They are most often guided by data, credit behavior, and an analysis of risk profiles that very often disguise the full story of one’s business.

It is not just the dismay and confusion that one feels when a loan is rejected- it can bring a halt to one’s drive, undermine your confidence, and make you wary of the next step you will take. But this is not the end of the road.

It is essential to understand how the system works to take the next step: why business loans get rejected, what lenders have in mind when they read a loan application, and most importantly, what are the ways by which you can increase your chances of acceptance.

This guide says it all, with practical references and deep insights into what matters most in 2025.

What Is a Business Loan?

A business loan is not just procuring ready cash; it opens the vistas of abundant possibilities that can give momentum to the business. Whether you are launching a new product, investing in an attractive infrastructure, or tiding over a lean period, a loan comes in handy to give the fuel any business would need to move forward.

In 2025, business loans are no longer just a line of credit; they have become carefully structured financial tools that the bank, NBFCs and digital lenders are ready to offer, that involve a keen understanding of eligibility, repayment, and risk. A borrower will have to meet the lender’s expectations to be eligible for it.

How Lenders Evaluate Loan Applications

Beneath a lender's decision lies a formidable framework of checks and scrutiny, which goes way beyond surface-level numbers. Here is a list of probable checks that a lender relies on-

- Credit Score Check: This is one of the first filters used. A low CIBIL score could be the first step to rejection.

- Cash Flow Analysis: Lenders need assurance of a consistent income to trust that you can afford loan repayments.

- Financial Documentation: Your financial story unfolds before the lenders through your profit and loss statements, tax returns, and bank statements.

- Business Age & Stability: You appear trustworthy to a lender when you project a steady income from being operational for a greater number of years.

- Existing Debt Load: You are in a high-risk zone when you have too many open loans. Lenders are wary of businesses that are already too stretched.

These are some potential checks that every borrower needs to consider. Your business may not lack potential, but it may be stretched too thin to be preferred.

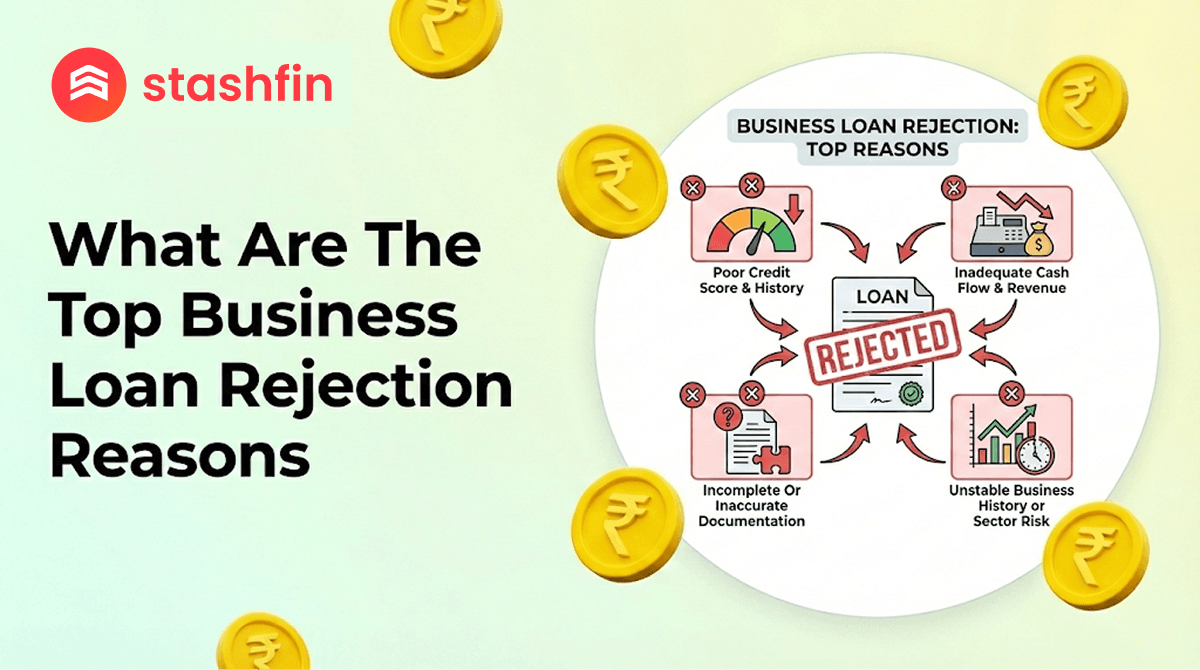

What are the common Reasons for Business Loan Rejection in 2025

Have you ever wondered why business loans get rejected, even when everything seems right?

In 2025, the focus is not just on poor credit; it’s more about the bigger picture and, most often, the smallest details. Here you may read some most common reasons for business loan rejection:

- Low Credit Score: A low CIBIL Score is a sure shot reason for rejection, since it rings a warning bell for repayment risks.

- Weak and unpredictable Cash Flow: Unstable cash flows ring a strong alarm bell for even profitable businesses.

- Incomplete and Inaccurate Documentation: A good reason to disqualify you would be to notice inconsistencies in your paperwork, old and outdated records, or any kind of missed paperwork.

- New Business without History: New business ventures with less than a year or two of sustained performance data can face scrutiny.

- Overleveraging: When debt is significantly high already, the lender may refrain from adding to the pile of your borrowings.

Often, even the most prepared business owners could fall into these aforementioned traps unless very careful.

Tips to Avoid Business Loan Rejection

Although a loan rejection isn’t always a final verdict, a little care and caution can help you avoid them. Here is a list of tips to help you avoid business loan rejection.

- Check and improve Your Credit Score: Always keep a check on your credit usage and resolve overdue payments and dispute errors if any.

- Keep Your Financial Records Organized: Statements that are clean and updated will exhibit transparency that will make a positive impact.

- Strengthen Your Business Plan: Focus on the ROI, show how you have a foolproof plan to generate returns.

- Apply for the Right Loan: Your business size, stage, and income level must match the loan you have applied for.

- Avoid Multiple Applications at Once: when the number of inquiries is too many, it can negatively impact your credit.

Although applying for a loan is like a sales talk, only here, impressing people should not be the focus; rather, you should try to convince a system that is only concerned about facts, figures, and financial reliability.

Impact of Credit Score on Business Loan Approval

In 2025, the only number that carries more weight than most is your credit score.

Whether it’s a traditional bank or a Fintech platform, lenders all across use this score to judge your financial responsibility. Just as a high score would boost your trustworthiness, a low score would make a lender cautious. A low CIBIL score results in loan rejection, and it is usually one of the first roadblocks to hit any business.

Can a Rejected Loan Be Reapplied?

Definitely. Rejection means looking out for other options in the market; it requires you to regroup.

It has been observed that most lenders assign a reason for rejecting a loan, even though it may not make much sense to you. However, use the reasons to fix your issues. Use observations to strengthen your weak points. Do not apply immediately; wait for anything between 30 to 60 days before reapplying.

Always remember that reapplication has to be a thoroughly thought-out plan where a larger number of applications lowers your chances, so apply smart. You will ask yourself, “Why are my loans getting rejected?” The answer lies in the truth that reapplying without positive changes will fetch the same results.

Alternative Funding Options for Small Businesses

In today's dynamic financial scenario, options are aplenty. When one door closes, another opens. One business loan rejection doesn’t close all doors; you will still have many funding paths opening up in front of you. For example-

- Microloans: These are small, low-interest loans, mostly available through nonprofit or government programs.

- Invoice Financing: In this case, it will be possible for you to use unpaid client invoices as collateral for quick money.

- Crowdfunding: It’s a popular platform that allows you to create a story to attract funds.

- Angel Investors or Venture Capital: A popular platform for high-growth businesses with a unique value proposition.

- Government Schemes and Subsidies: This is particularly designed for entrepreneurs, MSMEs, or priority sectors.

All the above-mentioned platforms come with their eligibility requirements and their plus and minus points. At the end of the day, they go to prove that a rejected loan doesn't end a business story.

Conclusion

Today, applying for a loan is a carefully thought-out strategy, a foolproof exercise in positioning, preparation, and presentation.

It is true that the reasons for business loan rejection can seem harsh and illogical in many cases, but they help you steel your resolve to grow even stronger. The loan rejection could delay your plan, but it doesn’t undermine your potential.

Do your homework well, gain a thorough understanding of the system, and know for sure that it’s a juxtaposition of the right loan, at the right time, and with the right lender that will give you the positive outcome. Platforms like Stashfin can further guide you with simplified personal and business loan solutions tailored to your financial needs.