What Are Gift Loans and How Do They Work?

Gift loans have become the default solution for Indian families who need to pay for significant expenses, such as a wedding in Jaipur, a medical bill in Kochi, or relocating a child to Mumbai in 2025. People are choosing gift loans instead since living costs are going up, and they feel they should help their family.

These regulations don't apply to formal loans, but informal financial favours like a father giving a child ₹50,000 for a down payment on a house are done with love and little paperwork. But you still need to be clear about what you want, even if it's just a favour. Gift loans walk a fine line between money and goodwill, which means that tax rules and intent matter more than most people think.

This article tells you how gift loans work, how they are different from regular loans or gifts, and how to be careful while lending or borrowing money from family members. You will get examples from actual life, cultural backgrounds, and rules to help you make these plans safer and easier.

Let's see if gift loans will help you with your finances.

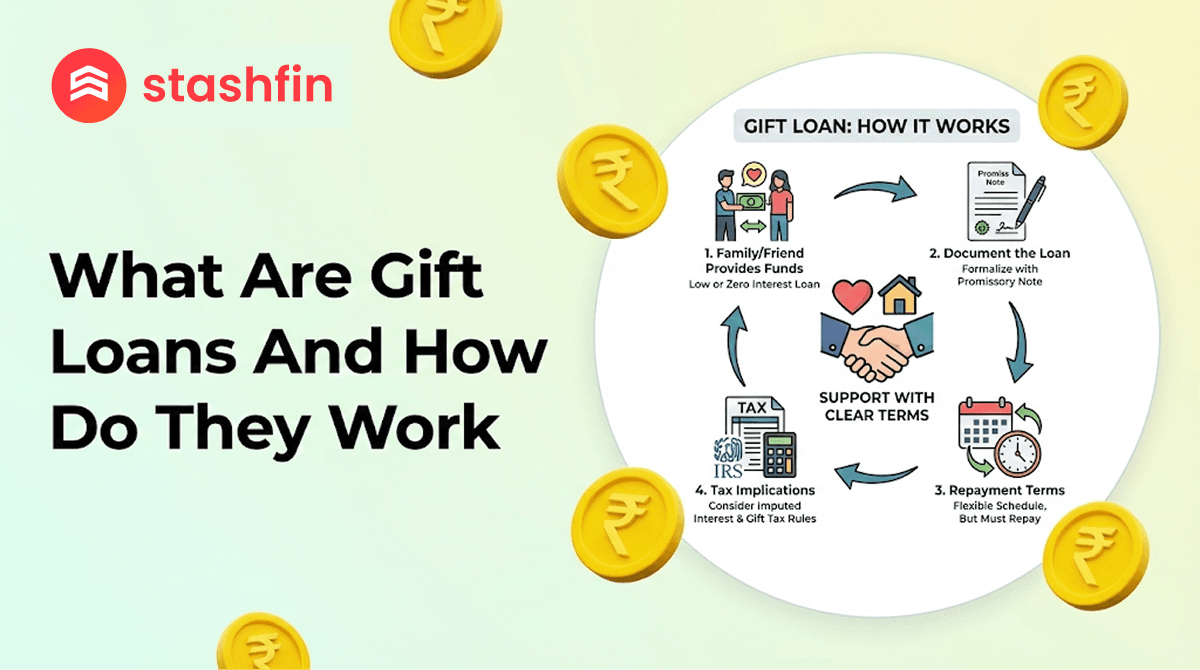

What Is a Gift Loan?

A gift loan is taking money from someone close to you, say a friend or a relative, without terms and without interest. They are different from bank loans, which are on terms and not on trust. There may be an unspoken understanding that the money would be returned, but without urgency, and definitely not in the form of EMIs.

Below are the reasons why a gift loan is different from a standard personal loan:

- No interest is paid

- Minimal or no documentation

- It's borrowed within families or close circles

- Repayment is convenient, with no fixed time

In India, these are a common occurrence at family gatherings or celebrations. Imagine a father quietly lending his daughter ₹1 lakh towards wedding expenses, or an uncle in Ahmedabad paying for a nephew's school fees with a promise to repay "when things settle."

The relationship is worth more than the balance sheet, and that is precisely what makes gift loans special.

Key Features of Gift Loans

Gift loans are no ordinary financial transaction. They're being made on goodwill and trust, not on clauses and fine print. Even these casual arrangements have some characteristics:

- Zero or Very Low Interest: Most gift loans don't carry any interest; it's a favour, not a business transaction.

- Shared Within Families: Parents, siblings, cousins, or close relatives are typically the parties involved.

- Repayment on Mutual Terms: No strict EMIs or time limits, just a mutual understanding to repay as and when possible.

- Minimum Paperwork: A casual WhatsApp note or plain letter can be the only document that is put down.

- No Collateral Involved: Here, trust is more valued than the signed paper.

At times like Diwali or Raksha Bandhan, the loans can prove useful for impromptu buying, festival expenses, or short-term shortages. It's more assistance on the spur of the moment rather than transactions.

Difference Between Gift Loans and Personal Loans

While both involve lending money, gift loans and personal loans work on very different terms. Your choice depends on the relationship, urgency, and how formal you want the arrangement to be. Here's a side-by-side view:

1. Structure

- Gift Loans: Casual and rooted in personal trust, often just a conversation.

- Personal Loans: Formal, issued by banks or NBFCs, with paperwork and approval steps.

2. Interest

- Gift Loans: Usually interest-free or involve a token amount.

- Personal Loans: Carry fixed interest, typically between 9% and 16% as of 2025.

3. Repayment Terms

- Gift Loans: No fixed EMIs. Repayment may be open-ended or discussed casually.

- Personal Loans: Come with a repayment schedule, EMIs, and late penalties.

4. Tax Considerations

- Gift Loans: If undocumented, large amounts could be seen as gifts and taxed under the Income Tax Act.

- Personal Loans: Not taxed, and in some cases (like home renovation), the interest paid may offer tax benefits.

In short, gift loans are built on personal bonds; personal loans are bound by financial rules. One supports sentiment, the other supports structure. Choose what fits your situation best.

Benefits and Risks of Gift Loans

Gift loans often feel like the easiest solution when a loved one needs quick help. But while they’re rooted in goodwill, they come with their own trade-offs. If you’re considering giving or taking a gift loan, especially during a wedding, festival, or family emergency, here’s what to weigh:

Benefits

- Strengthens family support: Lending without expectations can build deeper trust.

- No added pressure: Since there’s usually no interest or strict deadlines, repayment feels easier.

- Faster access to money: No paperwork or approval queues, just a decision between two people.

- Ideal for short-term use: Perfect for last-minute costs, event planning, or small emergencies.

Risks

- No legal backing: If things go south, there’s little legal ground to stand on without documentation.

- Risk to relationships: Delayed or missed repayment may cause awkwardness or long-term resentment.

- Tax uncertainty: If large amounts aren’t clearly documented as loans, the tax department may treat them as gifts.

- No official trail: Without a basic written record, both parties may forget or misinterpret terms later.

For anything above ₹50,000, it’s wise to at least draft a simple agreement or mention repayment terms in writing. It keeps things friendly and clear.

10 Common Uses of Gift Loans

Taking a personal loan for gifting can be a thoughtful way to help someone close, especially when there’s a clear need and mutual trust. Across India, families often turn to gift loans for reasons that feel deeply personal and practical.

Here are 10 real-life ways people use gift loans today:

- Wedding costs – covering venue, outfits, or last-minute arrangements

- Festival shopping – helping with Diwali décor or Eid gifts

- Education expenses – school fees or college admission deposits

- Medical bills – stepping in when insurance doesn’t cover it all

- Home repair or renovation – chipping in for repainting or plumbing fixes

- Buying gadgets or jewellery – for gifting or big family events

- Helping with a small business – capital for stock or equipment

- Paying rent or deposit, especially in shifting cities

- Religious events – like organising a puja or family ritual

- Travel help – funding a honeymoon or urgent family trip

Whether it’s a cousin’s engagement in Lucknow or a school term starting in Chennai, gift loans offer a way to support each other, without turning it into a formal financial transaction.

How to Prepare Your Taxes for Potential Gift Loans

It’s easy to overlook the fine print when helping out a loved one. But when money changes hands, especially in large sums, keeping things clean on paper matters. Even if it’s a family arrangement, tax rules still apply, and they’re getting more specific in 2025.

Here are a few things to keep in mind to stay on the right side of the rules:

- Put it in writing: A simple note signed by both people can go a long way. It doesn’t need legal jargon, just clarity.

- Mention repayment, even loosely: Whether it’s a “return when you can” deal or after six months, it helps define intent.

- Use bank transfers: Avoid giving large amounts in cash. Digital payments leave a record, which can prevent future tax queries.

- Know the ₹50,000 rule: Under Indian tax laws, gifts over ₹50,000 in a financial year may be taxable unless they fall under specific exemptions.

- Speak to a CA: If the amount is large or spread over financial years, a quick chat with a tax advisor could save trouble later.

For a more organised approach, Stashfin makes things easier by offering quick personal loans tailored to your needs, whether it’s helping a relative, covering festive costs, or managing a family emergency. With minimal paperwork, flexible repayment options, and real-time tracking, it lets you support loved ones while staying in control of your finances.

Conclusion

Gift loans can be thoughtful and timely, helping a friend in need or supporting a family event without the red tape of formal loans. But even with good intentions, it’s important to be mindful of the financial and emotional boundaries involved.

If you're looking for more structure or want to avoid tax complications, personal loans are a practical alternative. They offer clear terms, repayment schedules, and peace of mind, especially when taken from trusted digital platforms.

You can explore personal loan options on Stashfin that are easy to apply, quick to disburse, and designed to keep things simple when it matters most.