Navigating the Risks of Bond Investing: A Strategic Guide for 2026

In the current financial landscape of 2026, where the RBI Repo Rate has settled at 5.25%, bond investing has moved from the sidelines to center stage. For many, the allure of 14.5% annual returns from secured corporate bonds, like those offered by Akara Capital on Stashfin, is the perfect antidote to lackluster savings account rates.

However, as with any investment that offers superior yields, it is vital to understand that "fixed income" does not mean "zero risk." To be a successful investor in 2026, you must know how to identify, evaluate, and mitigate the specific risks associated with debt instruments.

1. Understanding the Core Risks of Bond Investing

While bonds are generally more stable than the volatile equity markets of 2026, they are subject to a unique set of market forces.

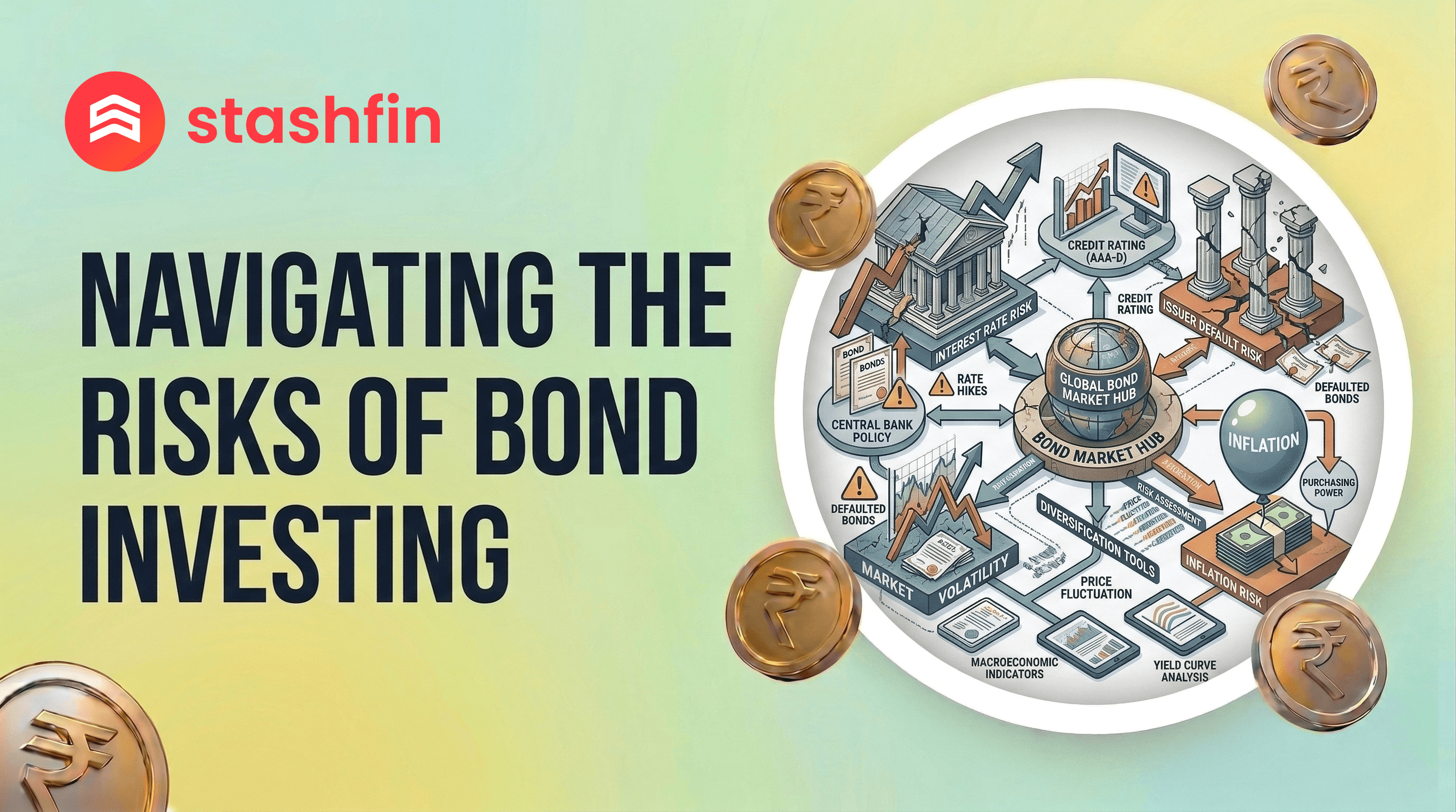

A. Interest Rate Risk: The Seesaw Effect

Interest rate risk is the most fundamental risk in the bond market. It describes the inverse relationship between market interest rates and bond prices.

- The Logic: If you hold a bond paying 8% and the RBI raises interest rates, new bonds will be issued at 9%. Your 8% bond is now less attractive, causing its market price to drop so its yield matches the new 9% standard.

- 2026 Context: With rates expected to stay "lower for longer," the primary risk today is the Opportunity Cost of being locked into a lower rate if the economy heats up faster than expected.

B. Credit Risk (Default Risk)

Credit risk is the possibility that the bond issuer will be unable to make timely interest payments or repay the principal at maturity.

- The Safety Gauge: Always check the Credit Rating. In 2026, an AAA rating signifies the highest safety, while a BBB rating (like Akara Capital) represents "Investment Grade" with moderate safety and significantly higher yields.

C. Inflation Risk (Purchasing Power Risk)

This is the risk that inflation will exceed the fixed return of your bond, eroding your "Real Return."

- The Math: If your bond pays 7% but inflation is 6%, your real gain is only 1%.

- The Buffer: High-yield bonds (14.5% p.a.) provide a massive inflation buffer compared to traditional FDs in 2026.

2. Advanced Risks in the 2026 Market

As the Indian debt market matures and "retailises," new nuances have emerged.

- Liquidity Risk: The difficulty of selling a bond before maturity without a price hit. Stashfin mitigates this by focusing on short-term 12-month tenures and monthly payouts.

- Reinvestment Risk: The risk that when your bond matures, you can only reinvest at a lower rate.

- Strategy: Many 2026 investors use a "Barbell Strategy", combining long-term G-Secs with short-term, high-yield corporate bonds.

- Call Risk: If a bond is "callable," the company can pay you back early if rates drop. Always verify if a bond is "Non-Callable" to lock in your high yield.

3. How Akara Capital Bonds Manage These Risks

At Stashfin, we believe in structured safety. Here is how Akara Capital Bonds are designed to protect the retail investor:

- The "Secured" Advantage: Most offerings are Secured Corporate Bonds, backed by the company's underlying assets. Secured bondholders are prioritised over equity shareholders in the payment hierarchy.

- Rigorous Credit Monitoring: Akara Capital maintains an Investment Grade (BBB/Stable) rating through continuous audits of capital structure and asset quality.

- Short-Term Tenures: By keeping tenures at 12 months, Stashfin minimises exposure to long-term interest rate fluctuations and inflation spikes.

4. Comparing Bond Profiles: Risk vs. Reward (2026 Data)

| Bond Type | Typical Yield | Primary Risk | Safety Level |

|---|---|---|---|

| Government G-Secs | 7.0% – 7.5% | Interest Rate Risk | Sovereign (Highest) |

| AAA Corporate Bonds | 7.5% – 8.5% | Inflation Risk | High Safety |

| Akara Capital Bonds | 14.5% | Credit Risk (Managed) | Strategic Yield |

| Unrated Junk Bonds | 18.0%+ | High Default Risk | Speculative |

5. 5-Step Checklist for Safe Bond Investing in 2026

- Check the Rating: Is it from a SEBI-registered agency like ICRA, CRISIL, or CARE?

- Verify the Security: Is the bond "Secured"? What specific assets back it?

- Understand the Payout: Does it offer monthly interest? (This reduces your "Time-at-Risk").

- Analyse the Issuer: Does the company have a transparent track record like Akara Capital?

- Diversify: Never put 100% of your capital into a single bond. Mix AAA safety with BBB yield boosters.

Conclusion

Navigating the risks of bond investing in 2026 means pricing them correctly. While no investment is 100% risk-free, the secured, short-term, and high-yield nature of Akara Capital Bonds on Stashfin offers a compelling "risk-adjusted" opportunity.