How to Read Bond Yields and Avoid Investment Mistakes in 2026

Reading 2026 bond yields is not about the numbers; it's about being ready for another world of finance. With the Reserve Bank of India (RBI) holding the repo rate at 5.25% in its February 2026 meeting and a neutral stance, knowing how yields move helps you make informed decisions—whether you are building a retirement cushion or protecting your portfolio from stock market volatility.

This guide breaks down the bond market landscape in the current "goldilocks" zone of high growth (7.4% GDP) and low inflation, helping you navigate yields without the jargon.

What Is a Bond Yield and How Is It Calculated?

A bond's yield is a reflection of the return you get for owning a bond, typically measured as a percentage. In India, yields act as benchmarks for loans, deposits, and other financial products.

Simple Yield Formulas:

- Standard Yield: $$\text{Bond Yield} = \frac{\text{Annual Coupon Payment}}{\text{Face Value of the Bond}} \times 100$$

- Current Yield: $$\text{Current Yield} = \frac{\text{Annual Coupon Payment}}{\text{Market Price}} \times 100$$

- Yield to Maturity (YTM): The total return expected if you hold the bond until it matures, accounting for all interest payments and any capital gain or loss.

Example: You buy a ₹50,000 bond with a ₹5,000 annual interest.

- Current Yield: $(5,000 / 50,000) \times 100 = 10%$.

- If the market price drops to ₹45,000, the yield rises: $(5,000 / 45,000) \times 100 = 11.1%$.

Why Bond Yields Fluctuate in 2026

As of February 2026, the 10-year G-Sec yield is hovering around 6.7%–6.8%. Yields are currently under pressure due to several factors:

- Record Government Borrowing: The FY27 Union Budget announced a record gross borrowing plan of ₹17.2 trillion, increasing the supply of bonds and pushing yields higher.

- Inflation Outlook: While current headline inflation is benign (around 1.3%–2.1%), the market expects it to tick up to 4%–4.2% by mid-2026 due to base effects and rising metal prices.

- Interest Rate Expectations: After 125 bps of cuts in 2025, the RBI has signaled a "long pause." When investors expect rates to stay high for longer, they demand higher yields on long-term bonds.

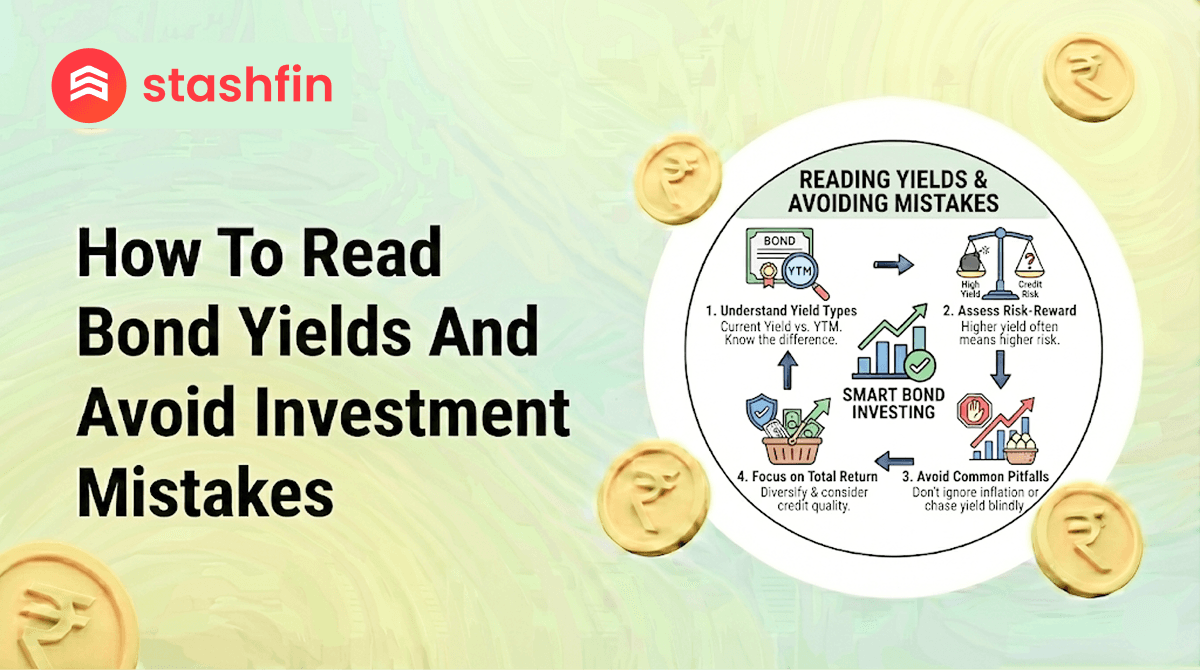

Common Mistakes New Bond Investors Make

- Chasing High Yields: A high return often signals higher credit risk. BB-rated corporate bonds yield more than AAA-rated ones because the risk of default is higher.

- Ignoring the Inverse Relationship: When bond yields rise, the price of existing bonds falls. If you need to sell before maturity, you could face a capital loss.

- Not Factoring in Inflation: If a bond yields 6% but inflation is 4%, your Real Yield is only 2%.

- Concentration Risk: Investing solely in one corporate issuer increases exposure. Diversify across government securities (G-Secs) and high-rated corporate bonds.

How to Analyze Yield with Your 2026 Goals

| Investment Goal | Recommended Strategy | Yield Metric to Watch |

|---|---|---|

| Emergency Fund | Short-term T-Bills or liquid funds. | Current Yield |

| Child's Education | Medium-term (3-5 year) G-Secs. | Yield to Maturity (YTM) |

| Retirement Income | Long-term sovereign bonds or AAA corporates. | Post-Tax Yield |

Pro Tip: Always calculate the post-tax yield. For an investor in the 30% bracket, a 7% taxable bond yields only 4.9% effectively.

Tools and Platforms to Track Yields in 2026

- RBI Official Website: The definitive source for daily G-Sec yields and policy rate updates.

- Stashfin: Provides user-friendly dashboards to monitor how yield trends might impact your credit limit and financial health.

- CCIL (Clearing Corporation of India): Offers detailed data on secondary market bond trades and yield curves.

Conclusion

Reading bond yields in 2026 isn’t just about chasing numbers; it’s about aligning them with your financial purpose. While the 10-year yield at 6.7% reflects a strong, borrowing-heavy economy, your personal strategy should focus on safety, tenure, and post-tax returns.

Would you like me to create a comparison table of current Fixed Deposit (FD) rates versus 2026 Benchmark Bond yields?