How to Invest in State Guaranteed Bonds: The 2026 Insider’s Guide

In the world of ultra-safe investing, State Guaranteed Bonds are often the hidden champions. While Central Government bonds (G-Secs) get all the headlines, these state-backed gems often offer a higher interest rate for essentially the same level of security.

In 2026, with the RBI's digital infrastructure more robust than ever, these are no longer reserved for institutional giants. Here is your roadmap to securing these high-yield, high-safety assets.

Understanding the Difference: SDLs vs. State Guaranteed Bonds

First, let's clear up a common confusion. There are two primary types of state-backed investments:

- State Development Loans (SDLs): Bonds issued directly by the State Government.

- State Guaranteed Bonds: Bonds issued by state-owned corporations (like a state power utility or infrastructure board) but officially guaranteed by the State Government.

If the corporation fails to pay, the state government is legally bound to step in. This "sovereign-like" backing makes them incredibly stable, but because they aren't "direct" government debt, they usually pay a higher interest rate—often called the "complexity premium."

The 2026 Advantage: Why Look Here?

In early 2026, while Central Government bonds are yielding around 7%, certain State Guaranteed Bonds are touching 8.2% to 8.5%. For a conservative investor, that extra 1.5% is a massive win over a 5-to-10-year horizon.

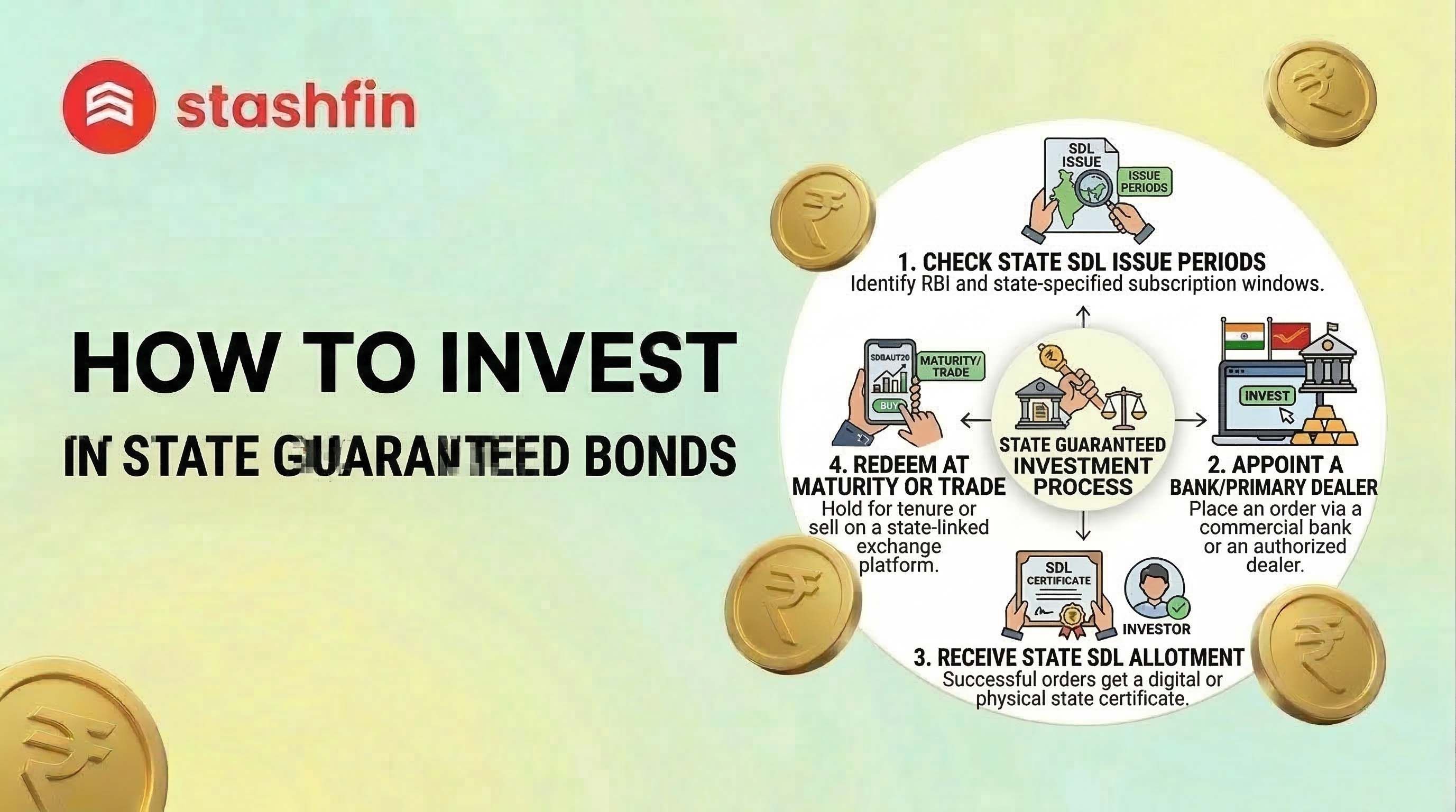

1. Where to Find These Bonds

State Guaranteed Bonds don't always appear in your basic banking app. You have to look in specific digital "marketplaces."

- GoldenPi / Wint Wealth / Grip Invest: These private platforms have democratized the bond market. They list State Guaranteed Bonds from issuers like the U.P. Power Corporation (UPPCL) or Andhra Pradesh Capital Region Development Authority (APCRDA).

- Stock Brokers (NSE/BSE): You can buy them in the secondary market through your Demat account (Zerodha, Groww, etc.). Search for the specific ISIN or bond name in the "Debt" or "Bonds" segment.

- The Secondary Market: Many of these bonds are traded daily. In the secondary market, you can often find "mispriced" bonds that offer a higher Yield to Maturity (YTM) than when they were first issued.

2. The Step-by-Step Buying Process

If you are buying through a specialized bond platform (the easiest method for retail investors):

- KYC: Complete your one-time digital KYC (Aadhaar + PAN).

- Browse the "State Guaranteed" Filter: Most platforms have a specific category for these.

- Check the "Credit Enhancement" (CE): Look for a "CE" rating (e.g., AA(CE)). The "CE" stands for Credit Enhancement, which is the official nod to the state guarantee.

- Payment: Use UPI or Net Banking to purchase. The bonds will be credited to your Demat Account within 24–48 hours.

3. The 2026 Tax Rules: Read Carefully

Budget 2026 has streamlined bond taxation, but it’s still "Slab Rate" heavy.

- Interest (Coupon): The interest you receive (usually semi-annually) is added to your total income and taxed at your Income Tax Slab Rate.

- Capital Gains: If you sell the bond on an exchange before maturity:

- Listed Bonds: Gains after 12 months are taxed at 12.5% (Long Term).

- Short Term: Taxed at your slab rate.

- TDS Considerations: While direct SDLs have no TDS, State Guaranteed Bonds (issued by corporations) might still have a 10% TDS deducted from interest payments. You can claim this back if your total income is below the taxable limit.

4. Risks: Nothing is 100% Free of Risk

Even with a guarantee, you should watch for two things:

Liquidity Risk: These bonds aren't as liquid as stocks. If you need to sell ₹10 Lakh worth of bonds tomorrow morning, you might have to sell at a slight discount. Plan to hold these until maturity.

Delayed Payments: While the state guarantee ensures you get your money, state-owned corporations can sometimes be slow with administrative paperwork, leading to minor delays in interest payouts.