How to Invest in Government Securities: The 2026 Sovereign Wealth Playbook

Investing in government securities is essentially betting on the house—and in this case, the house is the Indian Government. Since the government has the power to tax and print currency, these securities are the only "risk-free" (zero credit risk) investments available in the domestic market.

The 2026 Landscape: Why G-Secs Now?

The 2026 Union Budget has reinforced G-Secs as a primary pillar for retail savings. With bank FD rates stabilizing and the new "Retail Direct" mobile app making the process friction-free, the barrier to entry has never been lower. Whether you want to park cash for three months or build a 30-year pension, there is a specific security for that.

1. Know Your Tools: The G-Sec Spectrum

"Government Securities" is a broad category. To invest wisely, you need to pick the right instrument for your timeline:

- Treasury Bills (T-Bills): Short-term debt with tenures of 91, 182, and 364 days. They are issued at a discount and redeemed at face value.

- Dated G-Secs: Classic long-term bonds (5 to 40 years) paying a fixed interest (coupon) every six months.

- State Development Loans (SDLs): Issued by state governments. These often offer a slightly higher yield (0.2%–0.4% more) than Central Government bonds.

- Floating Rate Bonds (FRBs): Interest rates reset periodically based on a benchmark, serving as an inflation hedge.

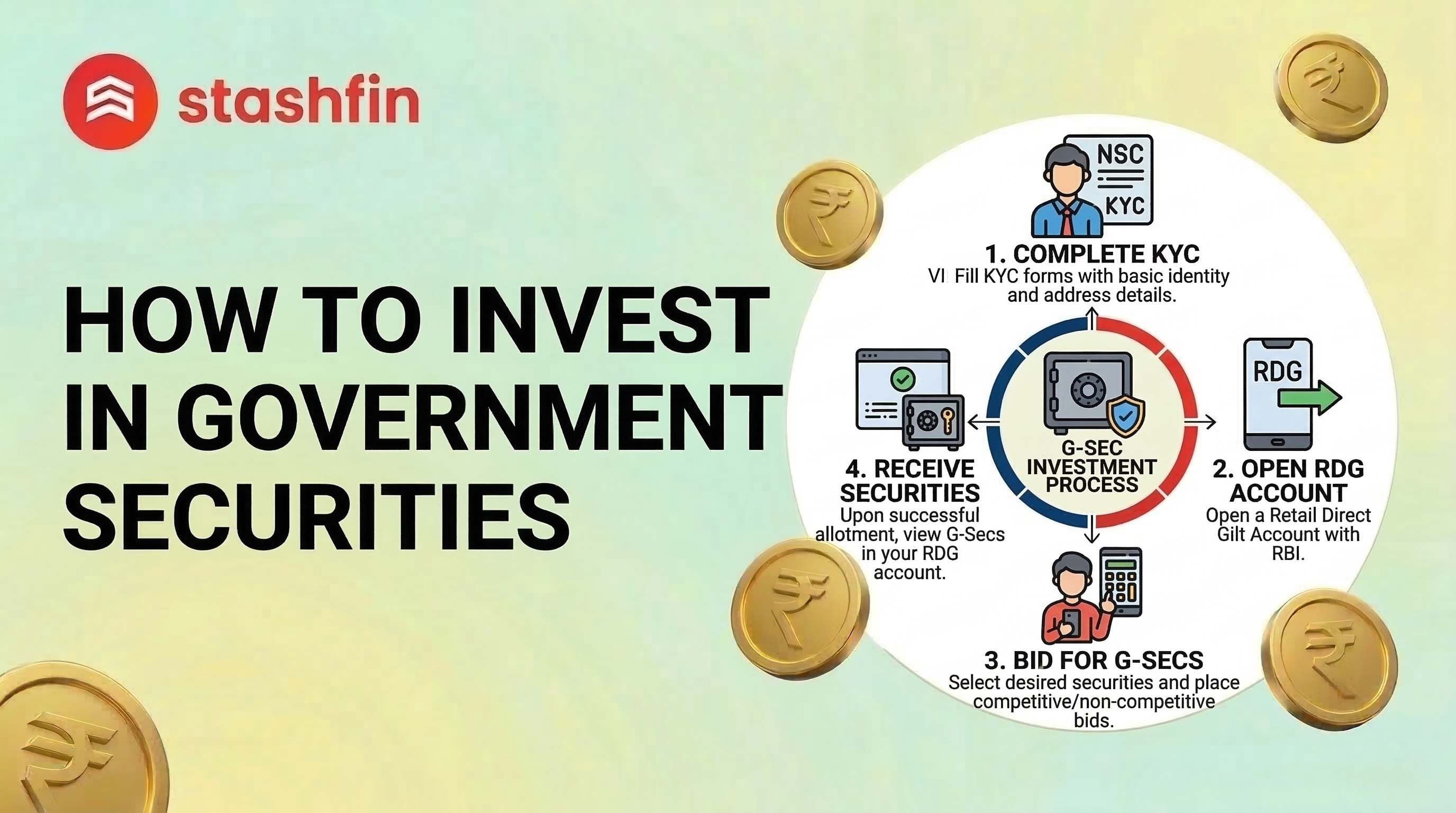

2. The Direct Route: RBI Retail Direct (App & Web)

This is the cleanest way to invest in 2026. By opening a Retail Direct Gilt (RDG) Account, you bypass all intermediaries.

The 2026 Workflow:

- Download the App: Use the official RBI Retail Direct app.

- KYC: Link your Aadhaar and PAN (mandatory as per 2026 mandates).

- Primary Auction: Place a "Non-Competitive Bid" during weekly auctions to get the weighted average price.

- Zero Fees: No brokerage, account opening fees, or annual maintenance charges.

3. The Secondary Market: Buying on the Exchange

You can buy existing bonds through your regular stock broker (Zerodha, ICICI Direct, HDFC Securities, etc.) if you don't want to wait for an auction.

- The Benefit: Instant entry on any business day.

- The Mechanism: Navigate to the "Bonds" or "NCB" section of your trading app.

- Liquidity Note: Selling quickly on the secondary market might involve a slight price "haircut" due to lower trading volumes in specific long-term bonds.

4. Taxation: The 2026 Rules

Taxes are where most investors get tripped up. Here is the 2026 breakdown:

| Income Type | Tax Treatment |

|---|---|

| Interest Income | Added to total income; taxed at your Income Tax Slab Rate. |

| TDS | No TDS deducted. You must declare this in your ITR. |

| STCG (<1 Year) | Taxed at your applicable slab rate. |

| LTCG (>1 Year) | Taxed at 12.5% (as per Budget 2026 for listed debt). |

5. Is This Better Than a Bank FD?

In 2026, the answer is often "Yes," especially for large amounts.

- Safety: FDs are only insured up to ₹5 Lakh. G-Secs carry a sovereign guarantee for the entire investment amount.

- Returns: SDLs frequently offer 0.5%–1.0% higher returns than FDs from major banks.

- Utility: G-Secs can be used as collateral for loans or as margin for trading.

Final Thoughts

Government securities provide a foundation of stability for any portfolio. By cutting out the middlemen via the RBI Retail Direct app, you ensure that 100% of the yield stays in your pocket.