How to Invest in Government Bonds (G-Secs): A 2026 Guide

When you buy a government bond, you are essentially lending money to the Government of India. In return, they promise to pay you a fixed interest (coupon) and return your principal at the end of the term.

Because the "borrower" is the sovereign government, these are considered virtually risk-free. There is no "default" worry here like there might be with corporate bonds.

Why Government Bonds are Trending in 2026

With global markets being unpredictable, Indian retail investors are flocking to G-Secs for three reasons:

- Direct Access: No more middle-men taking a cut.

- Flexible Tenures: From 91-day Treasury Bills to 40-year long-term bonds.

- No TDS: Unlike Fixed Deposits (FDs), interest on G-Secs is not subject to Tax Deducted at Source (though it is still taxable as per your slab).

The Three Main Ways to Invest

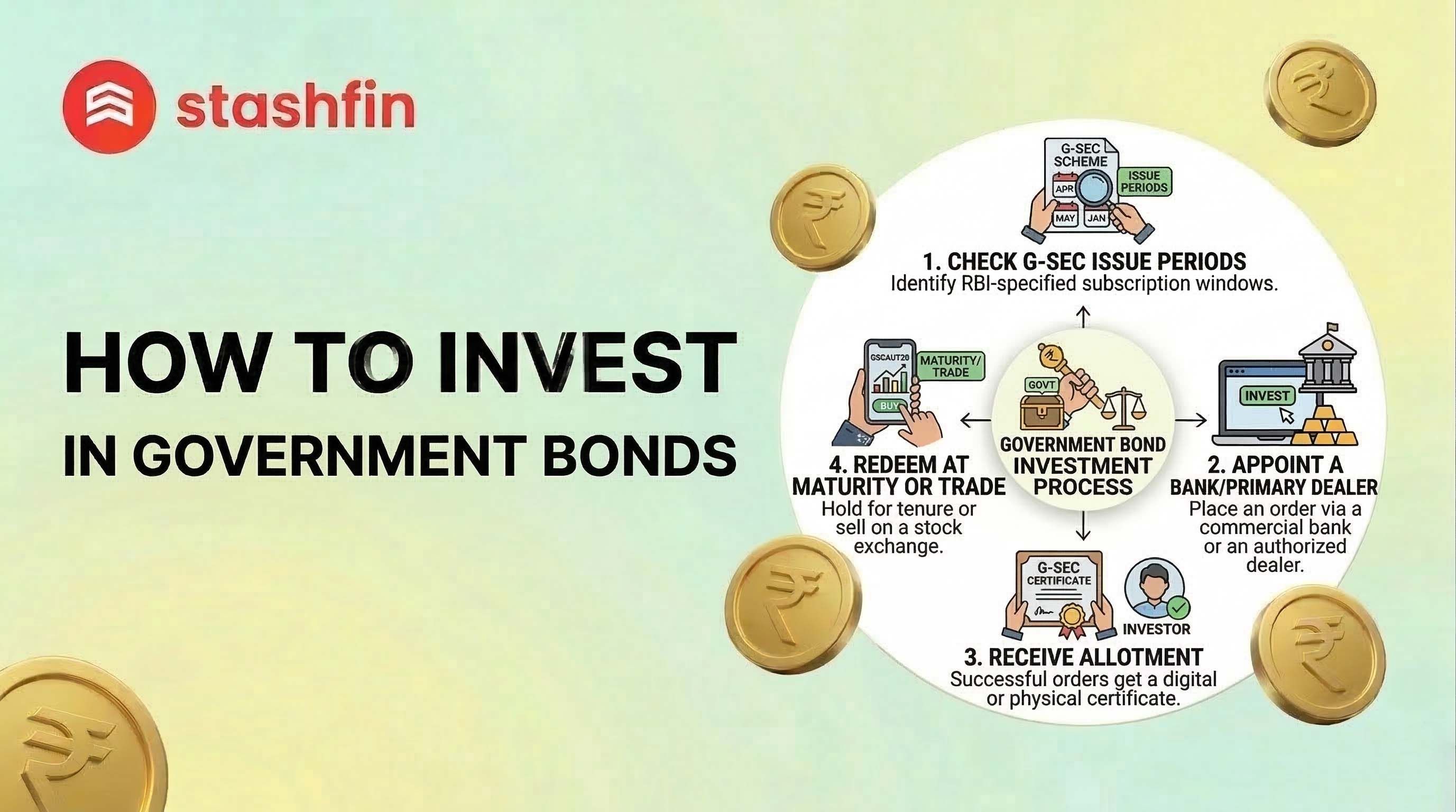

1. RBI Retail Direct (The "VIP" Route)

The RBI Retail Direct portal allows you to open a Retail Direct Gilt (RDG) Account directly with the central bank.

- Cost: ₹0. Opening and maintaining the account is free.

- The Process: Choose between Central Government Bonds, State Development Loans (SDLs), or Treasury Bills (T-Bills), and place a "Non-Competitive Bid."

- Why choose this: You get the absolute best price (weighted average) without any brokerage fees.

2. Through Your Existing Stock Broker (The "Easy" Route)

If you use apps like Zerodha, Groww, or Upstox, you don't need a new account.

- How it works: Look for the ‘Bids’ or ‘Bonds’ section in your app.

- The Experience: It’s just like applying for an IPO. Enter the amount (minimum ₹10,000) and block the funds via UPI.

- Settlement: Once allotted, the bonds show up in your regular Demat account.

3. Gilt Mutual Funds (The "Hands-Off" Route)

If picking specific bonds feels overwhelming, a professional fund manager can do it for you.

- Liquidity: Highly liquid—sell units and get cash in 24–48 hours.

- Diversification: The fund holds a basket of different government securities.

What are You Actually Buying?

Not all government debt is the same. Use this cheat sheet to decide:

| Instrument | Duration | Best For... |

|---|---|---|

| T-Bills | 91, 182, or 364 Days | Parking cash you need in less than a year. |

| Dated G-Secs | 5 to 40 Years | Long-term goals like retirement. |

| SDLs | Varies by State | Often pay 0.2%–0.5% more than Central bonds. |

| FRSBs | 7 Years | A hedge against rising inflation (rates reset every 6 months). |

The 2026 Tax Reality Check

- Interest Income: Taxed as "Income from Other Sources" at your applicable slab rate (10%, 20%, or 30%).

- Capital Gains: If you sell a bond on the secondary market (the stock exchange) before maturity, you will owe Capital Gains tax.

- Maturity: If you hold until the end, you get your principal back tax-free, as the "gain" was already taxed via the annual interest.

Is it Better Than a Fixed Deposit (FD)?

In 2026, government bonds often offer 0.5% to 1% higher returns than long-term FDs from top-tier banks.

The Safety Factor: FDs are only insured up to ₹5 Lakh by the DICGC. Government bonds have no such limit—the entire amount is backed by the sovereign guarantee of India. For someone looking to park ₹50 Lakh or more, G-Secs are the mathematically superior choice.