How to Build an Investment Portfolio with Short-Term Bond Options

Short-term bonds strike a rare balance; they’re more rewarding than a savings account but still flexible enough to meet short-term needs. Whether you're setting money aside for a car down payment, building an emergency fund, or gearing up for Diwali expenses, these investments can offer stability without long lock-ins.

Since they’re influenced by RBI policies and less volatile than stocks, short-term bonds are ideal for those who want steady returns with lower risk. In this guide, we’ll break down what short-term bonds are, why they make sense, how to use them in your investment plan, and the key risks to watch.

What Are Short-Term Bonds?

Short-term bonds are an investment in debt where you lend money to an issuer, such as the government or a business, for a short duration, typically less than one year. You get interest on your investment as repayment, and your principal is redeemed on maturity. Short-term bonds have fixed returns and are less sensitive to interest rate fluctuations since they are short-term.

Typical Choices Include:

- Treasury Bills (T-Bills): Issued by the Government of India with tenures of 91, 182, or 364 days. They are low-risk and highly liquid.

- Ultra Short Bond Funds: Mutual funds that invest in debt securities with a Macaulay duration of 3–6 months.

Due to their secure maturity and relative safety, short-term bonds are attractive for those who need to park money temporarily without sacrificing much yield.

Benefits of Short-Term Bond Investments

Short-term debt funds, like ultra-short duration bond funds, are preferred by investors seeking returns coupled with safety. They act as a reliable replacement for traditional fixed deposits.

Why invest in ultra-short duration bond funds?

- Low Market Volatility: They are less affected by interest rate fluctuations, providing a smoother experience.

- Improved Returns: Typically yielding 5-7% per annum, which is superior to standard savings accounts.

- Liquidity: Most funds have negligible exit loads, making it easy to access your money.

Popular Short-Term Bond Options in India

| Instrument | Tenure | Risk Level |

|---|---|---|

| Treasury Bills (T-Bills) | 91 to 364 Days | Low (Sovereign Guarantee) |

| Ultra Short Duration Funds | 3 to 6 Months | Low to Moderate |

| Short-Term Corporate Bonds | 1 to 3 Years | Moderate (Credit Dependent) |

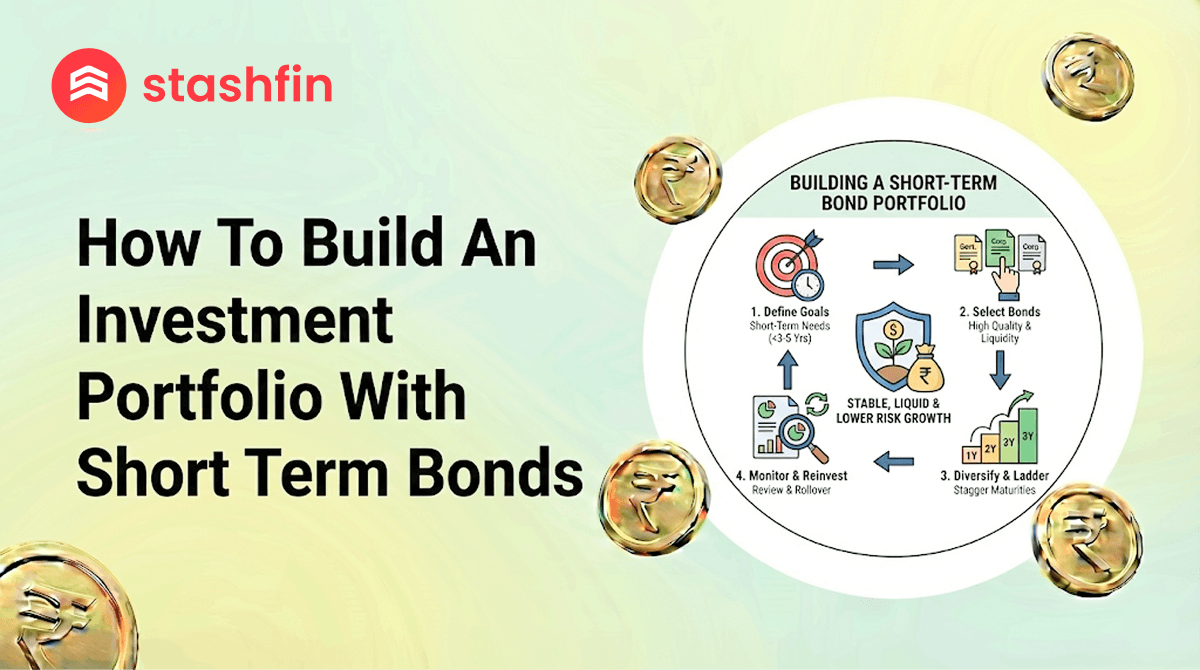

Steps to Build a Portfolio with Short-Term Bonds

Building a short-term bond portfolio is about mapping out your financial needs to ensure your money is available when required.

- Define Your Goal: Determine the exact amount and timeline (e.g., ₹1 lakh for an emergency fund).

- Decide Your Asset Mix: A sample split could be 50% T-Bills, 30% Ultra-Short Funds, and 20% Corporate Bonds.

- Pick the Right Instruments: * Use RBI Retail Direct for T-Bills.

- Explore mutual fund apps or AMCs like Mirae Asset for debt funds.

- Stay Flexible: Reinvest or adjust your portfolio as bonds mature based on the current market outlook.

- Track Credit Quality: Regularly monitor bond ratings and yields to keep risk in check.

Risks to Consider Before Investing

While short-term bonds are safer than stocks, they are not entirely risk-free:

- Credit Risk: Corporate bonds may face downgrades or defaults. Always check credit ratings.

- Reinvestment Risk: If rates drop before your bond matures, your next investment may earn less.

- Inflation Pressure: If inflation exceeds your yield, your real purchasing power decreases.

Pro Tip: Spread your investments across various issuers and credit profiles to add a layer of safety without sacrificing liquidity.

When Should You Choose Short-Term Bonds Over Other Assets?

Short-term bonds are the smart choice when stability is your priority:

- During Equity Volatility: They act as a cushion when the stock market dips.

- Near-Term Goals: Perfect for expenses coming up in the next 6–12 months (e.g., tuition, travel).

- Parking Idle Funds: When you want to beat inflation better than a savings account can.

Conclusion

Short-term bonds offer a practical mix of liquidity, moderate returns, and peace of mind. Whether you choose T-Bills for ultimate safety or corporate bonds for a yield boost, a balanced approach ensures your money works for you on your own timeline.

Looking to begin? You can check short-term bond options on Stashfin’s website and start building a portfolio that fits your financial timeline.