How RBI's Personal Loan Interest Rate Affects You

When most people think about taking a personal loan, the first question is usually simple: “How much will I need to pay every month?” And rightly so, whether you’re a salaried employee in Gurgaon planning your wedding, or a small business owner in Surat dealing with an unexpected cost, a personal loan can be a real financial lifeline.

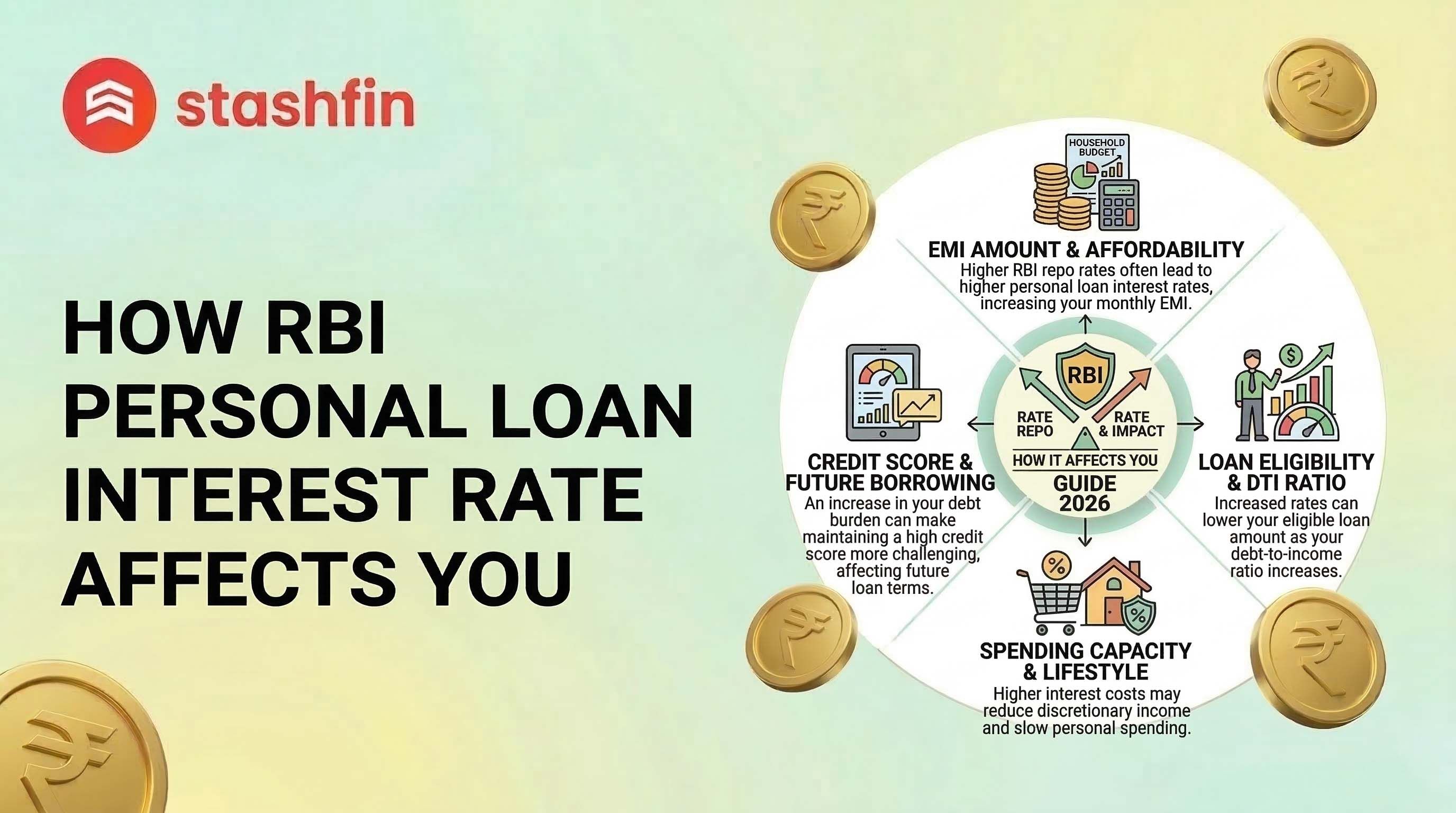

But here’s something people often overlook: how the RBI personal loan interest rate affects your EMIs. The RBI doesn’t fix your exact interest rate, but it gives banks a clear signal. When it changes things like the repo rate, banks and NBFCs usually follow by adjusting their lending rates. That change quickly shows up in the interest you pay on your loan.

Here, in this blog, we will demystify how the RBI personal loan interest rate affects your loan, from monthly installments and tenor to prepayment and chances of approval. Whether you are a first-time applicant or have to refinance a loan, understanding such a link can guide you to borrow wiser in 2025, in light of how money policy is shaping this year.

Why RBI’s Role Matters in Personal Loans

In the Indian economy, RBI is not only a regulator but a compass that all lenders follow directions from. By implementing tools such as the repo rate (the price at which RBI lends to banks), it determines the overall direction of whether loans are cheap or expensive for all.

RBI New Guidelines for Personal Loan – A Quick Look at Why It Matters:

Now that you are hearing RBI new guidelines for personal loan, here is the reality you actually must know, and why it impacts you personally:

- Repo rate effect: If RBI reduces the repo rate, like it did in June 2025, by reducing it by 50 basis points to 5.5%. That becomes cheaper for banks to borrow, and they typically transfer the savings to customers in the form of lower personal loan interest rates.

- Borrower safeguards: From how banks calculate your credit rating to foreclosure charges, the RBI puts it out in the open. It revises personal loan rules to ensure equity.

- Avoiding debt traps: With more and more people availing loans for weddings, higher studies and other needs, the RBI comes to the rescue to control aggressive lending, shield lenders from surprise charges, and keep the lender aware.

Long story short, your personal loan terms aren’t just shaped by your bank manager. They’re influenced by policies crafted on Mint Street, and staying updated with the RBI’s latest moves can make a real difference to your borrowing experience.

What is the RBI Personal Loan Interest Rate?

Let us make this clear first: the RBI does not charge a standard rate of interest on a personal loan to the borrower. It operates behind the scenes, primarily through its repo rate, i.e., at which banks borrow from the RBI. Most banks and NBFCs base their loans linked to the repo rate.

So, the next time you hear RBI having reduced the repo rate, how does your loan get affected?

Personal Loan Rate of Interest Slashed by RBI – What Does it Mean for You:

- If you are availing a new personal loan, banks are able to give you cheaper lending since their cost of funds reduced.

- If you already have a floating-rate loan, you may be paying less EMI, not now perhaps, but at the next rate reset cycle certainly.

- On a fixed-rate loan? Nothing happens right away. But if the rates drop dramatically, you may think of refinancing at a lower rate.

In June 2025, RBI cut repo rate by 50 basis points to 5.5%. Goal was to stimulate demand and ease credit. And for personal loan borrowers of Delhi, Pune, or Hyderabad, this meant one sure thing: cheaper borrowing, especially for those with floating-rate or hybrid-rate loans.

RBI Personal Loan Rules You Should Know

Before taking a personal loan, here are a few RBI rules you should know:

- Your credit profile counts: Banks and NBFCs must check your credit score, income, and past repayments. A good profile can mean lower interest and quicker approvals.

- No hidden prepayment fees: Planning to repay early? Lenders must tell you the exact charges upfront, no surprises later.

- Clear cost breakdown: You’ll now get a full view of charges, including interest, fees, and GST, all shown as a single APR.

- No automatic top-ups: Extra loan amounts won’t be added or approved unless you’ve clearly said yes.

- Pause before payout: Digital loans now have a short waiting period before disbursal, so you get time to rethink if needed.

Whether it’s ₹50,000 or ₹5 lakh, these rules are made to protect your decisions and keep things fair.

How RBI’s Rate Cut or Hike Affects Your Loan

Ever noticed your EMI going up or down without changing anything yourself? That’s probably the RBI repo rate doing its thing.

In June 2025, when the RBI announced a repo rate cut, lenders across India adjusted their loan rates in response. It’s one of the central bank’s key tools to manage how much it costs to borrow money.

RBI Guidelines for Personal Loan Prepayment Charges – What to Watch for:

Let’s break it down with simple scenarios:

| Scenario | Impact on You |

|---|---|

| Repo rate cut by 50 bps | Interest rate may drop → EMI becomes lighter or tenure shortens |

| Repo rate hike by 75 bps | Interest rate may rise → EMI gets costlier or tenure extends |

| Repo rate remains unchanged | No change in EMI, unless your lender reviews its rates |

| Lender delays rate transmission | EMI stays same for now → Check your loan reset cycle |

Let's assume you took a ₹5 lakh personal loan in April 2025 at 14% interest for 3 years If the repo rate drops in June and your lender passes on a 0.5% cut, your interest might reduce to 13.5%. That could lower your EMI by ₹200–₹300 every month.

But here’s the catch, this benefit shows only if your loan is linked to a floating rate or has a reset clause. Fixed-rate borrowers won’t see immediate changes.

Bottom line: A rate cut is good news, if your loan is built to take advantage of it.

New RBI Guidelines for Personal Loan Borrowers

2025 has brought in some important updates to personal loan rules, especially useful now that more and more Indians are using digital platforms to borrow. These RBI changes are meant to make your borrowing journey safer, clearer, and a little more in your control.

RBI Personal Loan Guidelines – 2025 Highlights

- Key Fact Statement (KFS) is now mandatory: Every lender must give you a one-page summary with all the basics, interest rate, charges, terms, clearly written, no fine-print surprises.

- Option to choose fixed-rate loans: Prefer a steady EMI every month? Salaried folks can now opt for fixed-interest loans that don’t change with market rates.

- DSA fee limits in place: If you're applying through a digital agent or third-party app, they can’t sneak in extra charges. RBI now caps what they can collect.

- NBFCs to follow stricter credit checks: Non-banking finance companies (such as NBFCs) now must adhere to the same credit guidelines. It's yet another move towards truthful and equitable lending.

- Easier loan portability: Got a better rate elsewhere? Now you can switch to some other lender with greater ease and lower penalties, subject to certain conditions.

Whether you're borrowing your first ₹1 lakh or refinancing a larger one, these changes leave you in charge, with a clear sense of what to expect.

EMI & Prepayment – RBI’s Impact

For most borrowers, the real pressure comes from monthly EMIs or surprise prepayment penalties. This is where the RBI plays a key role in keeping things fair.

RBI Guidelines for Personal Loan Prepayment Charges – What You Should Know:

- Prepayment penalty caps: If you’re on a floating-rate loan, most lenders must reduce or waive charges.

- Advance EMI clarity: Lenders must clearly tell you if they’re deducting EMIs in advance.

- Restructuring support: In genuine cases like job loss, RBI allows flexible repayment without hurting your credit score.

Example: You took a ₹3 lakh loan in Bengaluru in early 2024. After an RBI rate cut in 2025, your EMI drops from ₹10,200 to ₹9,900. Stashfin helps you track such changes and plan smarter prepayments, without nasty surprises.

Conclusion

The RBI’s monetary policy isn’t just for economists or the stock market, it directly affects your monthly EMI. Whether you're in Ahmedabad planning your next big move, or in Kochi repaying an existing loan, keeping an eye on the RBI personal loan interest rate can make a real difference.

The trick? Stay informed. Rates shift. Rules change. And lenders react quickly. You can check out loan options on Stashfin’s website to stay one step ahead and manage your money with confidence.