Understanding Bonds: Your Guide to Steady Passive Income

A bond is a simple agreement. Think of it like an IOU note. When you buy a bond, you are lending your money to a big company or the government. In exchange for your help, they promise to do two things:

- They will pay you interest for using your money.

- They will give your original money back on a specific date.

Lending Your Money for a Fee

Imagine your friend needs $100 to start a lemonade stand. You give them the $100. They promise to pay you $5 every month as a "thank you." At the end of the year, they give you your $100 back. That $5 every month is your passive income. A bond works exactly like this, but on a much larger scale.

How Bonds Pay You Passive Income

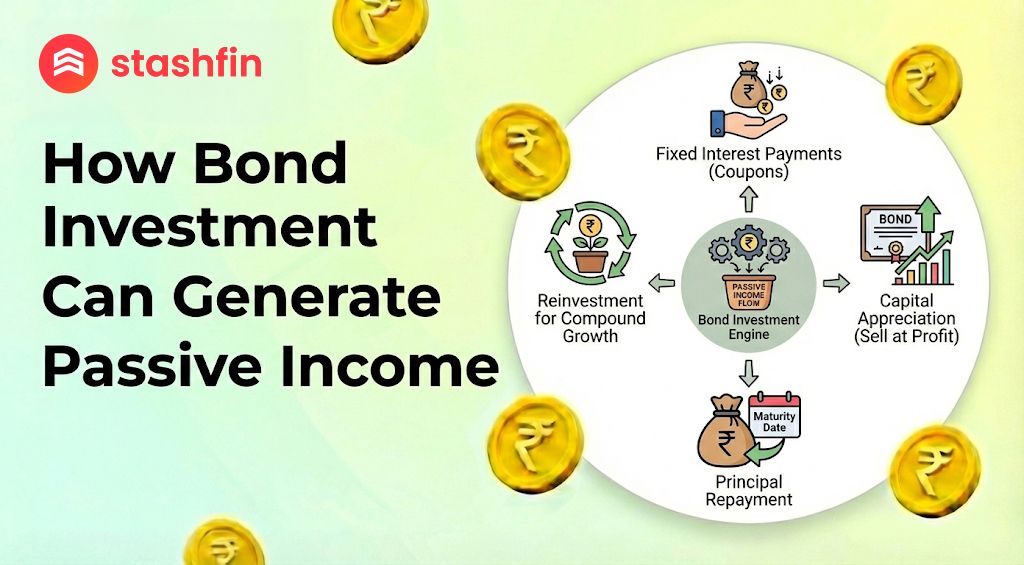

Passive income is money you earn while you sleep. Bonds are great for this because they are very predictable. You do not have to watch the news every day to see if you made money.

The "Coupon" Payment

In the old days, bonds were printed on paper with little tickets attached called coupons. Investors would clip these coupons and trade them for cash. Today, it is all digital. Most bonds pay you a set amount of money twice a year. This is still called a coupon payment.

Holding Until the End

Every bond has a "finish line" called the maturity date. When the bond reaches this date, the borrower pays you back the full amount you lent them (the principal). Because you get your money back at the end, your interest payments are pure profit.

3 Easy Ways to Start Buying Bonds

| Bond Type | Risk Level | Description |

|---|---|---|

| Government Bonds | Very Low | Lending to the country; considered the safest investment. |

| Corporate Bonds | Moderate | Lending to companies like Apple; higher interest for higher risk. |

| Bond Funds (ETFs) | Diversified | A "bucket" of many bonds managed by professionals. |

1. Government Bonds (Very Safe)

In 2026, Treasury bonds are very popular because they offer a guaranteed return. The government can always collect taxes to pay you back.

2. Corporate Bonds (Higher Pay)

Companies sell bonds to grow. Because a company could fail, they pay higher interest than the government to compensate you for that risk.

3. Bond Funds (The Hands-Off Choice)

A Bond ETF is a better way for many people. You can buy a "share" of a bucket filled with hundreds of bonds for a small price.

Why Choose Bonds Over Other Income?

- Bonds are Steady: Unlike the stock market "roller coaster," bonds are like a flat road.

- Legal Promises: If a company faces bankruptcy, they must pay bondholders before stockholders.

- Portfolio Balance: Bonds act like an umbrella during a rainstorm, staying steady when stocks drop.

Risks to Keep in Mind

- Inflation Risk: If the price of goods rises faster than your bond interest, your purchasing power drops.

- Interest Rate Risk: If new bonds offer higher rates, your old bond loses resale value. However, holding until maturity ensures you get your full principal back.

- Default Risk: The risk that a company cannot pay. Always check the bond rating (e.g., AAA is the safest).

How to Build a "Bond Ladder"

A bond ladder is a smart trick to get a paycheck every month. Instead of buying one big bond, you buy several small ones that end at different times:

- Bond A: Ends in 1 year.

- Bond B: Ends in 2 years.

- Bond C: Ends in 3 years.

Every time a bond ends, you reinvest the principal into a new bond at the top of the ladder.

Summary: Your Path to Passive Income

Bonds are a powerful tool for building a better life. By lending your money to strong governments and successful companies, you earn the right to a steady paycheck. Start small, look for a "Total Bond Market ETF," and watch your passive income grow. You are now a lender, not just a spender!