Housing Finance Companies in India: How They Work & What to Look For (2026 Expert Guide)

Before we dive into the deep end, let’s look at a quick summary of what this guide covers. This module acts as your roadmap to navigating the HFC landscape in 2026.

Quick Insights: The HFC Summary

- What is an HFC? A Housing Finance Company (HFC) is a specialized type of Non-Banking Financial Company (NBFC) that focuses primarily on providing credit for home purchases, construction, and renovations.

- Who regulates them? In 2026, the Reserve Bank of India (RBI) remains the primary regulator, while the National Housing Bank (NHB) manages refinancing and developmental roles.

- Why choose an HFC over a Bank? HFCs often provide more flexible eligibility criteria, faster processing, and higher loan amounts by including ancillary costs like stamp duty in the loan value.

- How do rates work? Unlike banks that use the Repo-Linked Lending Rate (RLLR), HFCs typically use their Prime Lending Rate (PLR). This means their rate changes might not always sync perfectly with RBI repo rate cuts.

- What is the "Credit Health" catch? Even with flexible criteria, a poor credit score leads to significantly higher interest rates. Checking your credit health before applying is the single most effective way to save on interest.

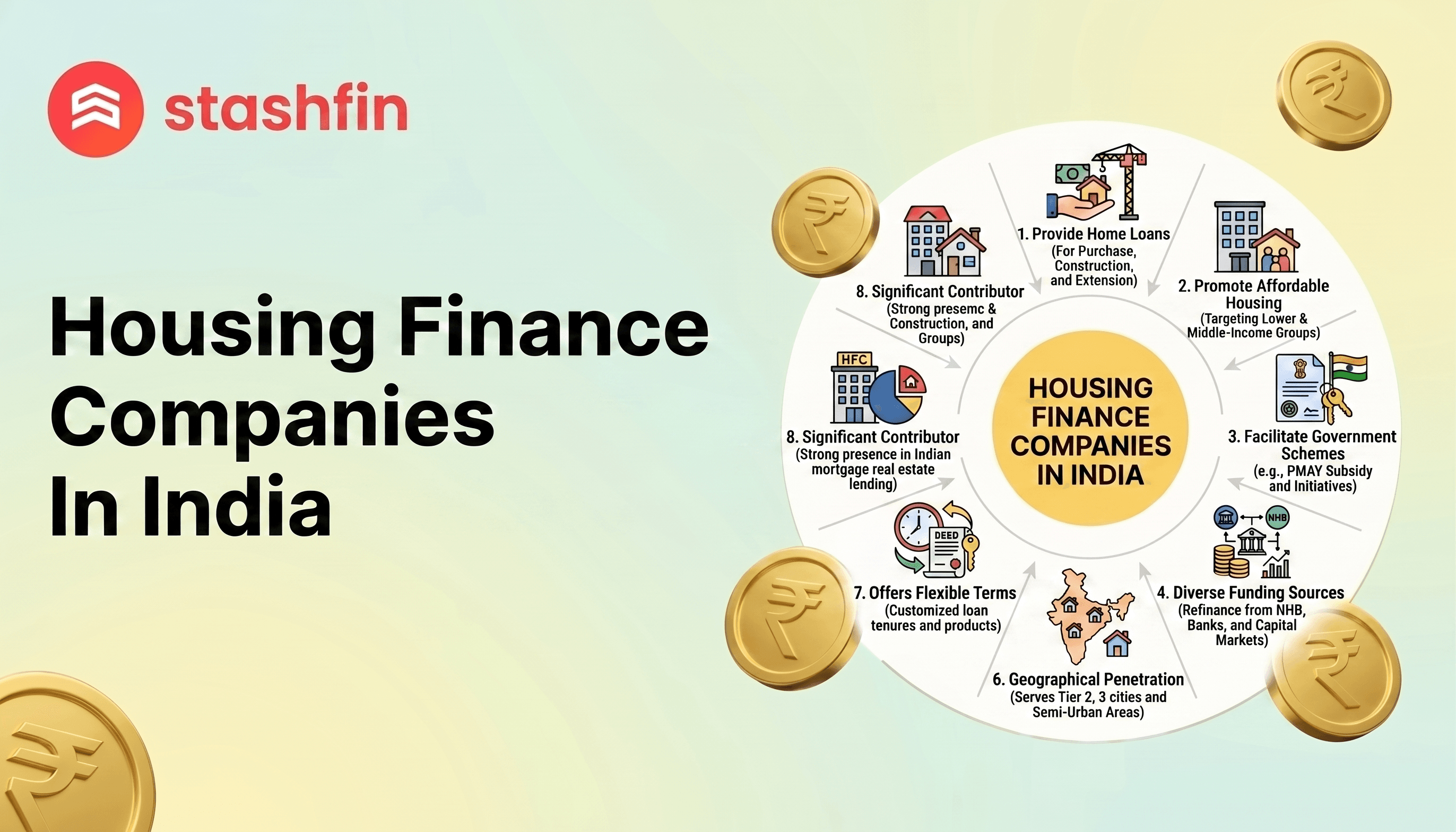

1. Understanding the HFC Landscape: What Exactly is a Housing Finance Company?

A Housing Finance Company is more than just a lender: it is a specialized institution built with the sole intent of promoting homeownership. Unlike a traditional bank that handles everything from savings accounts to gold loans, an HFC lives and breathes property.

The Legal and Regulatory Framework

HFCs are registered under the Companies Act and must maintain at least 60% of their net assets in providing finance for housing. In 2026, the distinction between HFCs and Banks has blurred slightly due to regulatory harmonization by the RBI, but their "customer-first" approach for homeowners remains a distinct USP.

Why it matters:

This specialization means that the loan officers at an HFC are usually more knowledgeable about local property laws, builder reputations, and specific documentation needed for "B-Khata" or "Panchayat" properties that traditional banks might reject.

2. How HFCs Work: The Financial "Plumbing" Behind Your Loan

To choose the right lender, you need to understand how they get the money they lend to you. This is called the "funding mechanism."

Funding Sources

Unlike banks, HFCs do not have a massive pool of low-cost "CASA" (Current Account and Savings Account) deposits. Instead, they raise money through:

- Refinance from the NHB: The National Housing Bank provides low-cost funds to encourage affordable housing.

- Corporate Bonds: HFCs issue bonds to institutional investors.

- Commercial Paper and Bank Loans: They borrow from larger banks to lend to you at a margin.

The Lending Mechanism (PLR vs. RLLR)

Banks link loans directly to the RBI's repo rate (External Benchmark). HFCs use an internal benchmark called the Prime Lending Rate (PLR). When the PLR goes up, your interest rate goes up. When the HFC offers a "discount" on the PLR, that becomes your effective rate.

Why it matters:

HFCs have more control over when they pass on rate benefits. Historically, they have been quicker to raise rates and slower to drop them compared to banks. Look for an HFC with a transparent track record of rate resets.

3. HFCs vs. Commercial Banks: The 2026 Comparison Table

| Feature | Housing Finance Companies (HFCs) | Commercial Banks (Public/Private) |

|---|---|---|

| Regulation | RBI (Regulated) & NHB (Supervised) | RBI (Directly Regulated) |

| Interest Rate Link | Prime Lending Rate (Internal) | Repo-Linked Rate (External) |

| Eligibility | Highly Flexible (Good for Self-Employed) | Strict (Prefer Salaried) |

| Documentation | Minimal and Approachable | Extensive and Rigorous |

| Max Loan-to-Value | Higher (Includes Stamp Duty/Registration) | Lower (Usually Property Cost Only) |

| Speed of Approval | Quick (3 to 7 Days) | Moderate (7 to 15 Days) |

| Credit Score Focus | High (but willing to negotiate) | Extremely High (Non-negotiable) |

4. What to Look For: The Ultimate HFC Checklist

A. Transparency in the PLR Reset Cycle

Ask the lender for their historical PLR data. Do they reduce rates for existing customers when the market drops, or only for new customers?

B. Inclusion of Ancillary Costs

One of the biggest hurdles is the "cash component" needed for registration and stamp duty. Some HFCs include these in the loan amount, while banks rarely do.

C. Turnaround Time (TAT)

In a competitive market, speed is currency. Look for HFCs that offer Digital Sanction Letters within hours based on your credit health.

D. Hidden Fees and Processing Charges

- Processing Fee: Usually 0.25% to 1% of the loan amount.

- Legal & Technical Fees: Fixed costs for property verification.

- MODT Charges: Charges for the memorandum of deposit of title deeds.

5. Preparing Your Application: A Step-by-Step Guide

- Credit Health Check (6 Months Prior): A score of 750+ can get you a rate of 8.5%, while 650 might push it to 10.5%.

- Consolidate Documents: Organize 6 months of bank statements; avoid cheque bounces or unexplained large deposits.

- Calculate Real Budget: Include registration (5-8%), interior work, and an emergency fund (6 months of EMIs).

- The "Soft" Inquiry: Ask for an "In-principle" eligibility check before a formal submission to avoid hard inquiries on your credit report.

6. The Role of Technology in HFCs (2026 Context)

- Video KYC: Remote verification without physical visits.

- E-Property Valuation: AI and satellite mapping for property assessment.

- Blockchain Records: Faster legal title searches through digitized land records.

7. Managing Your Home Loan Portfolio

- The Power of Prepayments: Paying even one extra EMI per year can significantly reduce your tenure. There are zero prepayment penalties on floating-rate loans.

- Balance Transfers: Consider moving your loan if you find a rate at least 0.50% lower elsewhere, after accounting for new processing fees.

- Insurance: Ensure you have a Home Loan Protection Plan so that unforeseen events do not put your family's home at risk.

8. Conclusion

HFCs are the champions of the middle class and the self-employed, offering flexibility that traditional banks often struggle to match. By prioritizing your credit health and understanding the PLR mechanism, you can navigate the path to homeownership with confidence.

Frequently Asked Questions (FAQs)

1. Is it safe to take a home loan from an HFC?

Absolutely. HFCs are strictly regulated by the RBI and supervised by the NHB, following standard fair practice codes.

2. Why are HFC interest rates usually higher than bank rates?

HFCs have a higher "cost of funds" as they lack access to low-interest savings deposits. They compensate with higher flexibility and better service.

3. Can I get a loan if I am a freelancer with no salary slip?

Yes. HFCs specialize in the "informal" income segment and assess bank statements and business models rather than just salary slips.

4. Fixed Rate vs. Floating Rate?

In 2026, most borrowers prefer floating rates to benefit from potential future market drops, linked to the PLR.