What Are Government Securities (G-Secs)?

Government Securities, or G-Secs, are like loans you give to the government. When the government needs money for large-scale projects like building roads or schools, they ask the public for help. In return, they provide a digital record confirming the debt and promising two things:

- Regular Interest Payments: Also known as "coupons."

- Principal Repayment: Your full original investment back on a set date.

Why Does the Government Issue These?

The money you lend is used to run the nation. Key projects include:

- Building highways, bridges, and digital infrastructure.

- Running public hospitals and schools.

- Funding national defense and military operations.

- Managing fiscal deficits when tax revenue is insufficient.

The Main Types of Government Securities

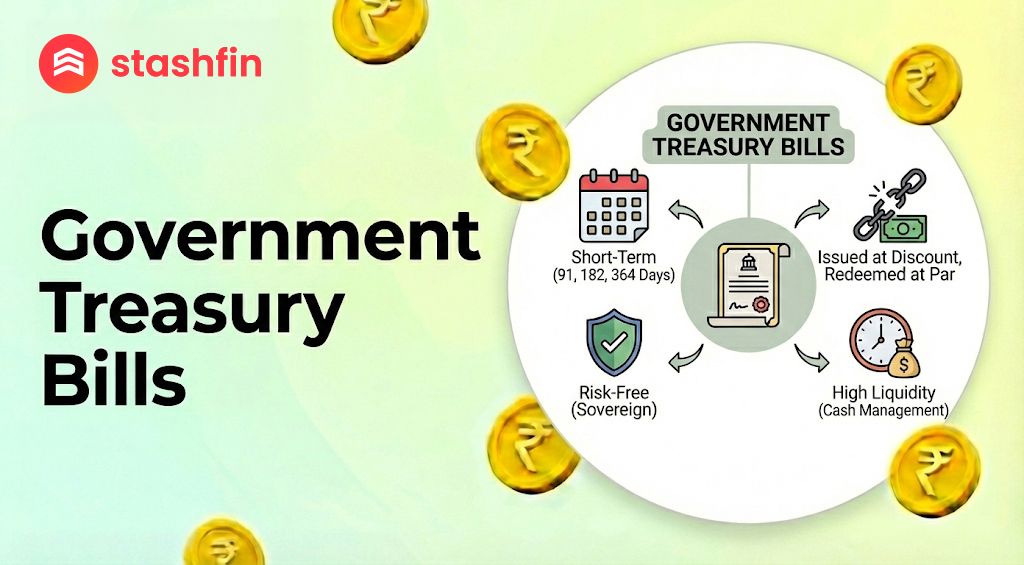

1. Treasury Bills (T-Bills) - The Short-Term Choice

Perfect for short-term savings, T-Bills last for 91, 182, or 364 days.

- How they work: You buy them at a discount (less than face value) and receive the full value at the end. Your profit is the difference between the two prices.

2. Dated Government Securities - The Long-Term Plan

These are long-term bonds with tenures ranging from 5 to 40 years.

- Best for: Steady income, as they pay fixed interest every six months.

3. State Development Loans (SDLs)

Just like the central government, individual states (like Maharashtra or Tamil Nadu) issue bonds to fund regional growth. They often pay a slightly higher interest rate than central government bonds.

4. Sovereign Gold Bonds (SGBs)

For gold lovers, SGBs track the market price of gold without the hassle of physical storage.

- Interest: You earn 2.5% per year on your initial investment.

- Tax Update 2026: Under the latest Budget 2026 rules, capital gains are tax-free at maturity only for original subscribers who buy directly from the RBI and hold until the end.

Why Invest in G-Secs? (The 2026 Benefits)

- Total Safety: Backed by a "Sovereign Guarantee," meaning there is zero default risk.

- No TDS: Unlike bank FDs, the government does not deduct tax at the source (TDS). You handle your own taxes at year-end.

- High Liquidity: In 2026, selling bonds is instant via the RBI Retail Direct mobile app or secondary markets like NDS-OM.

How to Buy G-Secs in 2026

It is now simpler than ever for individual investors to participate:

- RBI Retail Direct App: The official mobile app by the RBI allows you to open a free account and buy bonds directly.

- Demat Accounts: Popular apps like Zerodha, Groww, or Upstox allow you to buy G-Secs just like stocks.

- Net Banking: Most major banks (HDFC, ICICI, SBI) now have a "Bonds" section in their mobile banking apps.

Summary: G-Secs vs. Bank FDs

| Feature | Government Securities (G-Secs) | Bank Fixed Deposits (FDs) |

|---|---|---|

| Safety | Maximum (Sovereign Backing) | High (Insured up to ₹5 Lakh) |

| Tenure | Up to 40 Years | Up to 10 Years |

| Tax (TDS) | No TDS (Pay via your slab) | TDS deducted by the bank |

| Typical Yield | 6.7% – 7.5% (approx. for 2026) | 6.5% – 7.8% (varies by bank) |

G-Secs at a Glance

| Type | Best For | Time Period |

|---|---|---|

| T-Bills | Parking cash for a few months | < 1 Year |

| Dated Bonds | Retirement / Monthly Income | 5 to 40 Years |

| SGBs | Growing wealth with Gold | 8 Years |

| SDLs | Higher interest seekers | 3 to 35 Years |

Pro Tip: If you want the highest possible safety for an amount larger than ₹5 Lakh, G-Secs are superior to Bank FDs because the entire amount is guaranteed by the nation.