Back

Published May 4, 2026

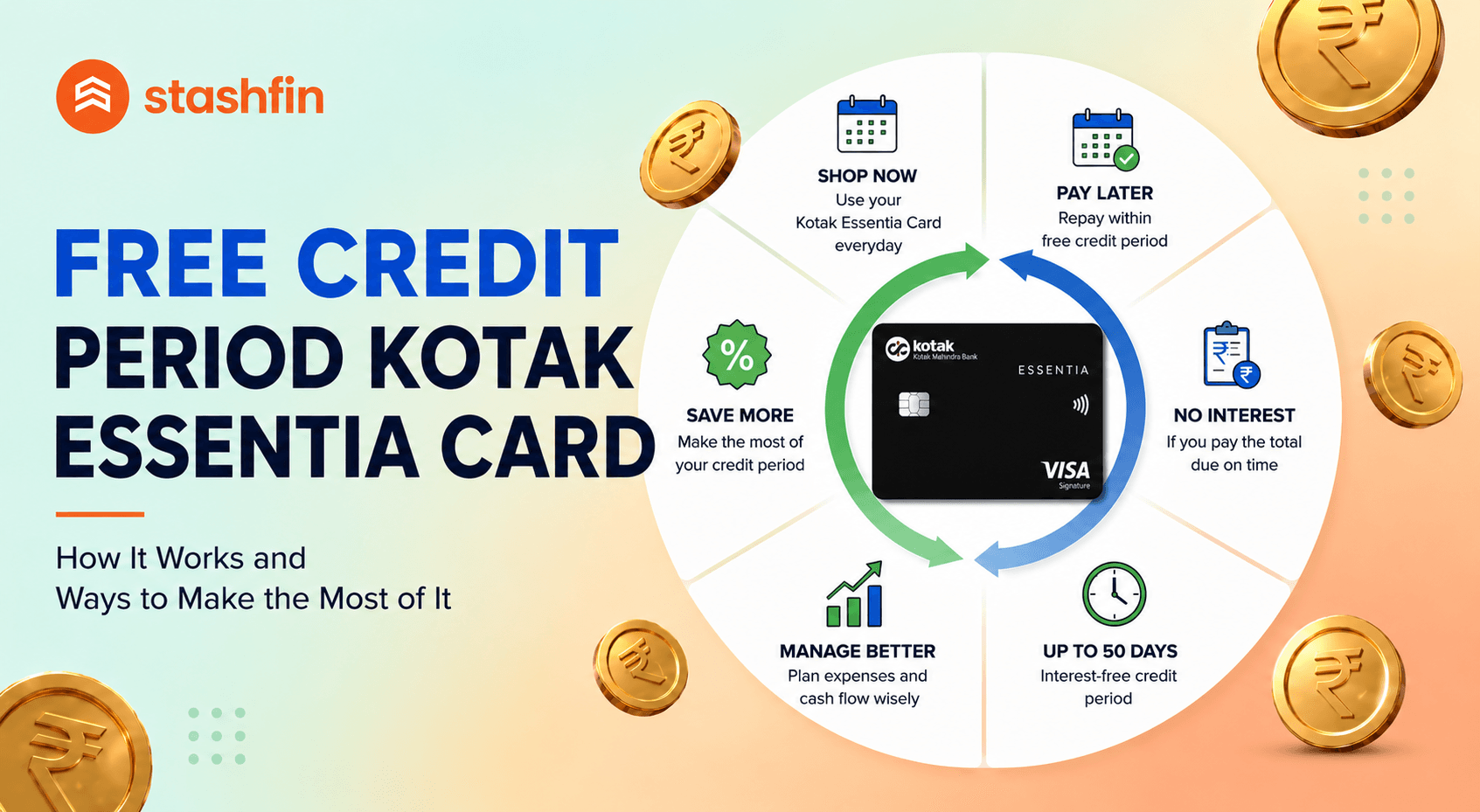

Free Credit Period Kotak Credit Card

Understanding the free credit period on your Kotak credit card can help you manage your monthly expenses more efficiently and avoid unnecessary interest charges. This guide explains how the billing cycle, statement date, and due date work together to give you interest-free days on your purchases.

Stashfin

May 4, 2026

Download Stashfin App