Simple Guide to Bond and Fixed Income Terms

Investing in bonds is like being the bank. You lend money to a company or a government, they promise to pay you back, and they pay you extra money for the favor. This extra money is called interest. Here is the easy way to learn the lingo.

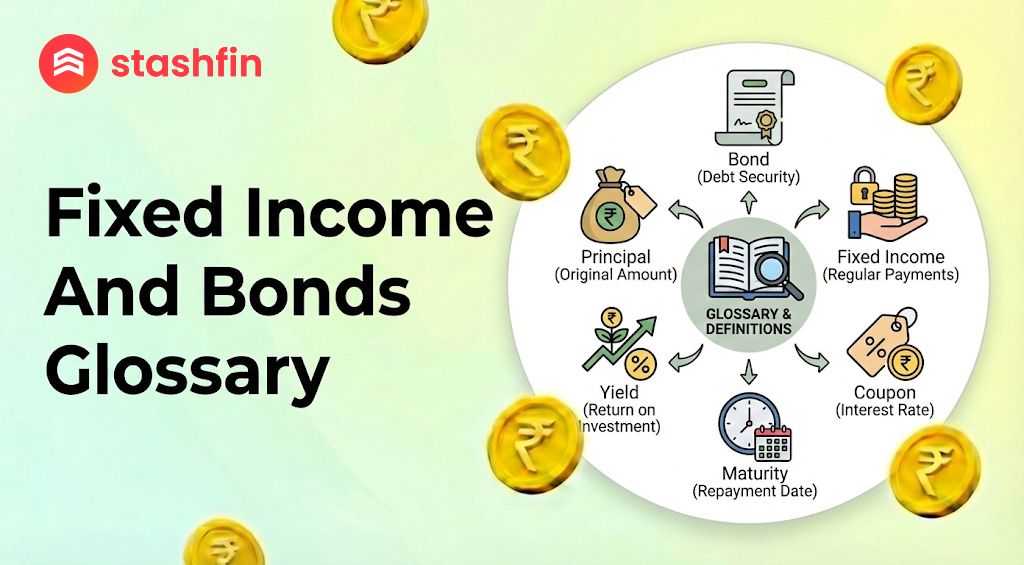

What is Fixed Income?

Fixed income is a specific way to invest that differs from stocks. When you buy a stock, you own a tiny piece of a company. When you buy fixed income, you are a lender.

The "fixed" part means the pay is steady. You know how much money you will get and when you will get it. It acts like a set schedule for your money to grow, helping your portfolio stay calm when the stock market gets wild.

Essential Bond Terms (The "Must-Knows")

Bond Principal / Face Value

The Principal is the amount of money you lend at the start. It is also called Face Value.

- Most bonds have a face value of $1,000.

- At the "Maturity Date," you get this full amount back.

Coupon Rate

The Coupon Rate is the interest rate.

- If a $1,000 bond has a 5% coupon, you receive $50 every year.

- Historically, investors clipped physical paper coupons to get their cash; today, it is all digital.

Maturity Date

The Maturity Date is the finish line—the day the loan ends.

- Short-term: Ends in 1 year.

- Long-term: Can last 30 years.

- On this day, the borrower returns your full Principal.

Bond Issuer

The Issuer is the entity borrowing your money. This could be:

- The Government (Treasuries)

- Corporations (Apple, Walmart, etc.)

- Municipalities (Cities building parks or schools)

Understanding Yield and Price

Current Yield vs. Yield to Maturity (YTM)

Yield is the word for "how much you actually make."

- Current Yield: Looks at the interest you get today compared to the price you paid.

- Yield to Maturity (YTM): The "total score." It counts all interest until the end, plus any gains or losses if you bought the bond at a discount or premium.

The Inverse Relationship

This is the most important rule in bonds. When interest rates go up, bond prices go down. Think of it like a Seesaw:

- If new bonds pay 7%, your old 5% bond looks boring. You must lower your price to sell it.

- If rates drop to 2%, your 5% bond becomes a "superstar," and its price goes up.

Types of Bonds

| Type | Issuer | Risk Level | Key Feature |

|---|---|---|---|

| Treasuries | U.S. Government | Lowest | Safest in the world; lower interest. |

| Corporate | Private Companies | Medium to High | Higher interest to reward the extra risk. |

| Municipal | Cities/States | Low to Medium | Often tax-free interest payments. |

Risks and Ratings

Default Risk

Default occurs when a borrower cannot pay you back. This is why investors check Credit Ratings before buying:

- AAA: The "A+" grade. Extremely safe.

- BBB: The "C" grade. Average safety.

- Junk Bonds: High risk, but they pay high interest to attract lenders.

Duration (Interest Rate Risk)

Duration measures how sensitive a bond is to interest rate changes.

- High Duration: Prices jump or fall significantly when rates move (common in long-term bonds).

- Low Duration: Prices stay mostly the same (common in short-term bonds).

Advanced Concepts: Par, Premium, and Discount

Bonds do not always sell for exactly $1,000 on the open market:

- Par Value: Selling for exactly face value ($1,000).

- Premium: Selling for more than face value (e.g., $1,050) because the interest rate is very attractive.

- Discount: Selling for less than face value (e.g., $950). You still get $1,000 back at maturity!

Inflation Risk: If your bond pays 3% but inflation is 5%, you are losing "buying power." Your money is growing slower than the cost of living.

Call Provision: Some bonds are "Callable," meaning the borrower can pay you back early. They usually do this if interest rates drop, similar to a homeowner refinancing a mortgage.