Guide to Taxation on Bonds in India (2026)

Maximize your post-tax returns by understanding the latest income tax rules for debt instruments.

- Interest Income: Taxed as per your slab rate under 'Income from Other Sources'

- Capital Gains: Revised 12.5% rate for Long-Term Capital Gains (LTCG) on listed bonds

- TDS Rules: 10% deduction on interest payments exceeding ₹10,000

- Tax-Free Options: Legally exempt your interest income using Section 10(15) bonds

Understanding Taxation on Bonds in India

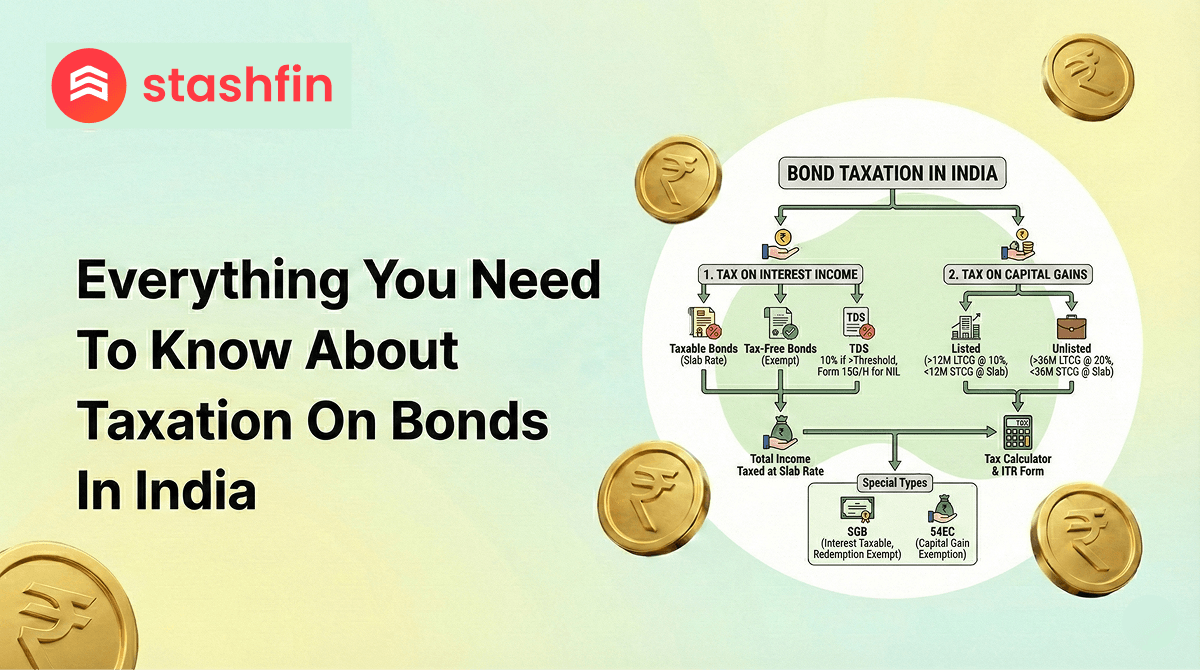

In the current 2026 fiscal environment, bonds remain a preferred choice for stable income. However, your "Real Return" depends entirely on how the government views your earnings. Taxation of bonds in India is split into two distinct categories:

- Interest Income: The periodic "Coupon" payments you receive (Monthly, Quarterly, or Annually).

- Capital Gains: The profit you make if you sell the bond on the secondary market at a price higher than your purchase price.

Tax on Bond Interest in India

The interest on bonds is taxable for almost all categories except specific "Tax-Free" issues. Here is how the law treats your coupon payments:

- Head of Income: Interest is categorized under "Income from Other Sources."

- Tax Rate: It is added to your total annual income and taxed according to your applicable income tax slab rate (New or Old Regime).

- Accrual Basis: Even if you hold a cumulative bond (where interest is paid at maturity), you are generally required to pay tax on the interest as it accrues each year.

Capital Gains Tax: Listed vs. Unlisted Bonds

The taxation of bonds in India underwent a significant shift in recent years to bring parity across asset classes. The tax rate depends on whether the bond is "Listed" on an exchange and how long you hold it.

1. Listed Bonds & Debentures

- Short-Term Capital Gains (STCG): If held for 12 months or less. Taxed at your slab rate.

- Long-Term Capital Gains (LTCG): If held for more than 12 months. Taxed at 12.5% (without indexation benefits).

2. Unlisted Bonds / Market Linked Debentures (MLDs)

As per the latest regulations (Section 50AA), profits from unlisted bonds, debentures, or MLDs are now treated as Short-Term Capital Gains regardless of the holding period. These are always taxed at your income tax slab rate.

| Bond Category | Period of Holding | Tax Rate (LTCG) | Tax Rate (STCG) |

|---|---|---|---|

| Listed Bonds | >12 Months | 12.5% | Slab Rate |

| Unlisted Bonds | Any Duration | Slab Rate (Always STCG) | Slab Rate |

| Tax-Free Bonds | >12 Months | 12.5% | Slab Rate |

Interest on REC Bonds Taxability & Special Categories

Many investors specifically look for interest on REC bonds taxability because of their popularity. REC (Rural Electrification Corporation) issues two main types of bonds with different rules:

- Section 54EC Bonds (Capital Gain Bonds): These allow you to save tax on LTCG from property sales. While the principal is exempt from tax, the interest is fully taxable at your slab rate.

- Tax-Free Bonds: These were issued in the past (available in the secondary market). The interest is 100% exempt from tax under Section 10(15).

TDS (Tax Deducted at Source) on Bond Interest

Under Section 193 of the Income Tax Act, issuers are required to deduct tax on bond interest in India before paying the investor:

- TDS Rate: 10% if a valid PAN is provided (20% without PAN).

- Threshold: TDS is applicable if the total interest paid in a financial year exceeds ₹10,000.

- Exemption: You can submit Form 15G or 15H to the issuer if your total annual income is below the basic exemption limit to prevent this deduction.

How to Report Bond Income in Your ITR

Managing your taxation on bonds during filing is a digital process:

- Schedule OS: Declare all interest income under "Income from Other Sources."

- Schedule CG: Report profits from the sale of bonds on the stock exchange.

- Form 26AS / AIS: Verify the TDS deducted by the bond issuer against your claims.

- Claim Exemptions: Ensure interest from tax-free bonds is reported under the "Exempt Income" section to avoid accidental taxation.

Taxation Strategy for 2026 Investors

- High-Slab Investors: Focus on Tax-Free Bonds to avoid the 30% hit on interest.

- Property Sellers: Use 54EC Bonds (REC/NHAI) to shield property gains up to ₹50 Lakh.

- Long-Term Holders: Prefer Listed Bonds to qualify for the 12.5% LTCG rate instead of your higher slab rate.