All About Cash Management Bills (CMB) – Government’s Short-Term Liquidity Tool

Master the ad-hoc financial instrument used by the RBI to stabilize India's cash flows.

- Sovereign Safety: Backed by the Government of India with zero default risk.

- Ultra Short-Term: Designed for immediate liquidity with maturities under 91 days.

- SLR Eligible: Ideal for banks to meet statutory regulatory requirements.

- Auction-Driven: Transparent pricing through RBI-led competitive bidding.

What is the Cash Management Meaning in Banking?

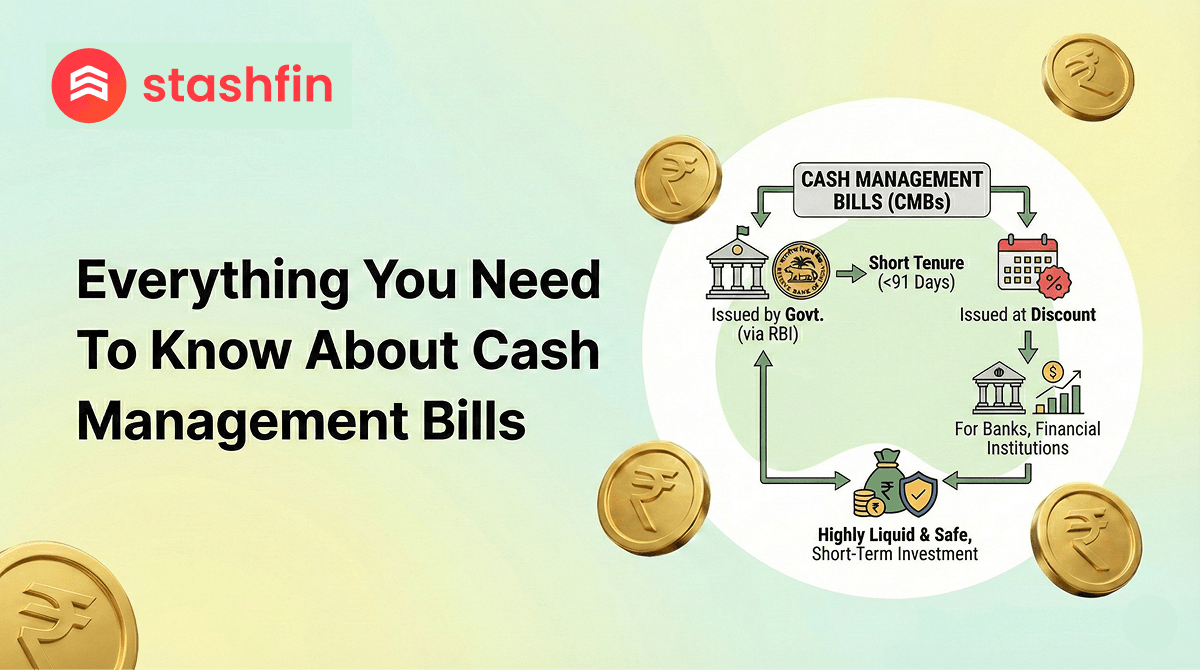

In the context of the Indian economy, cash management refers to the strategic process of monitoring and balancing the government’s short-term cash inflows (taxes, revenues) and outflows (expenditures).

When a temporary mismatch occurs, where spending exceeds available cash, the government reaches for Cash Management Bills (CMB). Introduced in 2010, these are non-standard, short-term money market instruments that act as a "bridge" to ensure fiscal operations run smoothly without the need for long-term borrowing.

Features and Benefits of Cash Management Bills India

When you invest in cash management bills India, you are participating in one of the most secure segments of the money market. Key features include:

- Short Maturity: CMBs are always issued for tenures of less than 91 days (often as short as 7 to 14 days).

- Zero-Coupon Structure: Like T-Bills, they pay no periodic interest. They are issued at a discount and redeemed at face value.

- High Liquidity: CMBs are tradable in the secondary market and eligible for Repo transactions, making them easy to convert to cash.

- Institutional Preference: They are a go-to for banks and mutual funds looking to park surplus cash for very short durations with virtually zero risk.

- Benchmark Yields: Their yields reflect real-time market liquidity, often serving as a key indicator for short-term interest rates.

- Statutory Compliance: Investment in CMBs is reckoned as an eligible investment for the Statutory Liquidity Ratio (SLR) for banks.

Why Understanding CMBs Matters for Institutional Investors

The difference between cash management bills and treasury bills is a thin but important line for treasury managers in 2026.

| Feature | Cash Management Bills (CMB) | Treasury Bills (T-Bills) |

|---|---|---|

| Maturity Period | Strictly less than 91 days. | 91, 182, and 364 days. |

| Issuance Schedule | Ad-hoc (As and when needed). | Fixed Auction Calendar. |

| Primary Goal | Emergency/Temporary liquidity management. | Regular short-term fiscal funding. |

| Investment Multiples | Multiples of ₹10,000. | Multiples of ₹25,000. |

| Non-Competitive Bidding | Not allowed. | Allowed for retail investors. |

Eligibility Criteria for Investing in CMBs

Qualification

Because of their high minimums and auction-based nature, CMBs are primarily designed for:

- Scheduled Commercial Banks: To manage SLR and liquidity.

- Primary Dealers: To act as market makers in government debt.

- Mutual Funds: Particularly Liquid and Money Market funds.

- Insurance Companies: For short-term deployment of premium income.

Documentation

The RBI manages the issuance through the Negotiated Dealing System (NDS):

- SGL Account: Investors must hold a Subsidiary General Ledger (SGL) account with the RBI.

- Demat Account: Retail participants (though rare) would need a Demat account to hold these in electronic form.

- PAN & KYC: Mandatory for all participating entities.

How to Apply for Cash Management Bills India

The process of issuance is managed entirely by the Reserve Bank of India (RBI):

- Announcement: The RBI issues a press release one day prior to the auction.

- Bidding: Market participants submit competitive bids (stating the yield they are willing to accept) through the E-Kuber portal.

- Allotment: Based on the cut-off yield determined by the RBI, successful bidders are allotted the bills.

- Settlement: Occurs on a T+1 basis, meaning the funds are debited and bills are credited the next working day.

Flexible Tools for India's Fiscal Stability

- Emergency Funding: Used during crises (like 2020) to manage sudden expenditure spikes.

- Tax Inflow Gap: Bridges the time between a budget spend and quarterly tax collections.

- Liquidity Absorption: Helps the RBI suck excess liquidity out of the banking system.