High-Yield Fixed Income on Bonds and FDs in India (2026 Edition) : Introduction

Secure your financial future with the safety of debt and the power of compounding.

- Stable Returns: Lock in interest rates up to 11% on high-quality corporate bonds.

- Capital Protection: Enjoy bank FD security with DICGC insurance up to ₹5 Lakh.

- Tax Efficiency: Leverage the 2026 tax regime with rebates up to ₹12 Lakh.

- Diversified Yield: Balance your portfolio against the equity market volatility of 2026.

[EXPLORE FIXED INCOME OPTIONS]

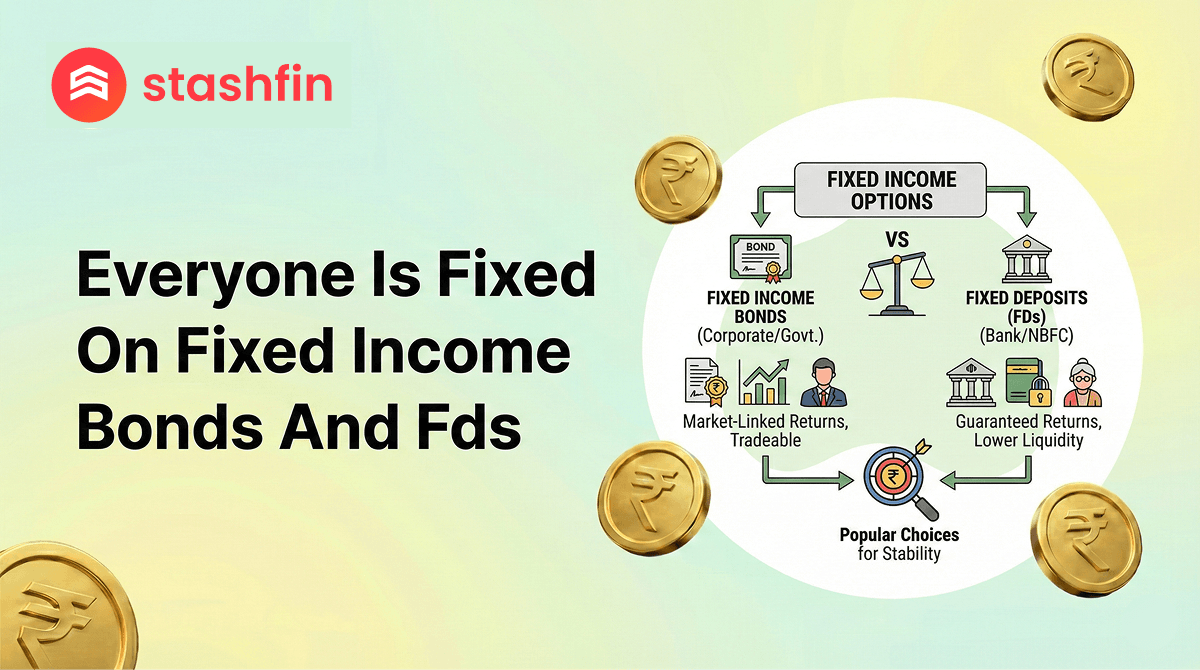

Why Everyone is "Fixed" on Fixed Income in 2026?

With equity markets showing heightened volatility in early 2026, savvy investors are shifting their focus. The demand for fixed income on bonds and FDs in India has reached a new peak as individuals seek "calm in the chaos."

- Market Resilience: While stocks fluctuate, bonds and FDs provide a contractual guarantee of interest and principal.

- Rate Cycle Pivot: Following the RBI's repo rate cuts in late 2025, long-term bonds are offering an attractive "lock-in" opportunity before further cooling.

- Institutional Inclusion: The inclusion of Indian G-Secs in global bond indices has brought unprecedented liquidity and stability to the domestic debt market.

- Digital Ease: Investing in a bond or opening a digital FD now takes less than 7 minutes, making it more accessible than ever.

Features and Benefits of Fixed Income on Bonds and FDs

Choosing a strategy for fixed income on bonds and FDs in India offers a robust alternative to traditional savings. In 2026, these instruments come with borrower-friendly enhancements:

- Predictable Cash Flow: Receive monthly, quarterly, or annual payouts to manage your lifestyle expenses.

- Portfolio Rebalancing: Use fixed income as a "ballast" to reduce the overall risk of your investment holdings.

- Small Ticket Investing: Start investing in corporate bonds with as little as ₹1,000, breaking the myth that debt is only for the wealthy.

- Senior Citizen Perks: Enjoy an additional 0.50% to 0.75% interest on FDs and specialized bond series.

- Secondary Market Liquidity: Unlike traditional FDs with exit penalties, listed bonds can be traded on the NSE/BSE for immediate cash.

- Collateral-Free Stability: High-rated corporate NCDs provide better-than-bank returns with professional management oversight.

Comparing Fixed Income: Bonds vs FDs in 2026

The fixed income on bonds and FDs in India landscape is diverse. Here is how the two primary vehicles compare for the current fiscal year:

| Feature | Corporate/Govt Bonds | Bank Fixed Deposits (FDs) |

|---|---|---|

| Typical Returns | 8% – 14.5% p.a. | 6% – 7.5% p.a. |

| Risk Level | Varies (Credit rating dependent) | Low (Insured up to ₹5 Lakh) |

| Liquidity | Tradable on exchanges | Premature withdrawal (with penalty) |

| Tax Treatment | LTCG @ 12.5% after 1 year | Taxed as per income slab |

| Ideal For | High-yield seeking, long-term investors | Capital preservation, emergency funds |

| Issuer | Corporates, PSUs, Governments | Banks and NBFCs |

Eligibility Criteria for Fixed Income Investments

Qualification

To access the best fixed income on bonds and fds in india, you must meet these simple requirements:

- Age: 18 to 100 years (Minors can invest through legal guardians).

- Resident Status: Both Resident Indians and NRIs (through NRE/NRO accounts).

- Income: No minimum income required for most retail bonds and digital FDs.

- Credit Score: While not required for investing, a fair credit score (650+) helps in accessing specialised debt platforms.

Documentation

The 2026 digital workflow requires minimal paperwork for immediate access:

- Identity Proof: Aadhaar Card and PAN Card (Linked).

- KYC: One-time Video KYC for digital FD platforms.

- Demat Account: Mandatory for bonds; optional for traditional bank FDs.

How to Start Your Fixed Income Journey

- Select Your Asset: Choose between the high-yield potential of corporate bonds or the safety of a bank FD.

- Verify Yields: Use our dashboard to compare the "Real Return" after accounting for inflation and taxes.

- Digital Onboarding: Complete your 100% digital application using Aadhaar-based OTP.

- Instant Allocation: Fund your account via UPI or Net Banking and receive your allotment/e-receipt instantly.

Interest Rates & Charges (Updated Jan 2026)

A transparent look at your earning potential and the costs involved in building a fixed income portfolio.

| Type of Investment | Current Interest Rate (p.a.) | Standard Charges |

|---|---|---|

| PSU/Govt Bonds | 7.2% – 7.8% | Nil (Brokerage only) |

| Corporate NCDs (AAA) | 9.5% – 10.5% | Platform fee (0.5% - 1%) |

| Digital FDs (Private Banks) | 7.0% – 7.5% | Nil |

| Small Finance Bank FDs | Up to 8.25% | Nil |

| NSC (Post Office) | 7.7% (Fixed for 5 years) | Nil |

Fixed Income Assets for Every Financial Goal

- Retirement Planning: Long-term G-Secs and Perpetual Bonds for lifelong income.

- Education Fund: Tax-saving 5-year FDs and Zero-Coupon Bonds.

- Emergency Buffer: Short-term 390-day "Liquid" FDs with zero premature penalty.

- Wealth Growth: High-yield corporate bonds like Akara Capital offering 14.5% returns for aggressive interest compounding.

Note: Akara Capital bonds and other high-yield instruments mentioned may be subject to market risks; always read the offer document carefully before investing.