Digital Gold vs. Gold ETF vs. SGB: The Ultimate 2026 Investment Guide

Caught between the ease of Digital Gold, the liquidity of Gold ETFs, and the tax benefits of SGBs? We compare Digital Gold vs. Gold ETF vs. SGB with the latest 2026 tax rules to help you maximize your returns and secure your future.

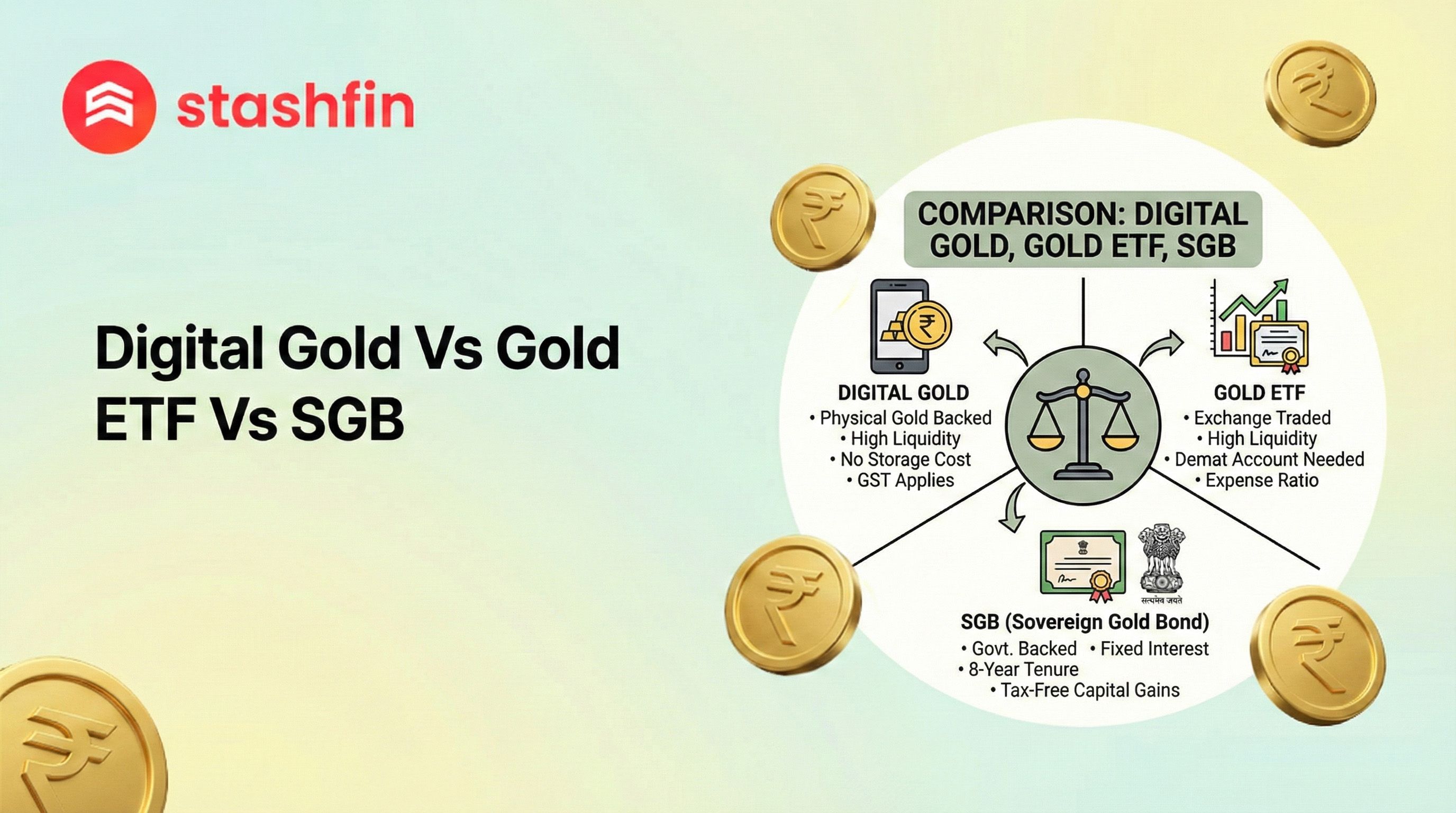

1. Digital Gold: The "SIP" King for Beginners

Digital Gold has revolutionized how young India saves. It allows you to buy 24-karat, 99.9% pure gold for as little as ₹1. When you buy digital gold on an app like Stashfin, a corresponding amount of physical gold is purchased and stored in high-security, insured vaults.

- Pros:

- Micro-Investing: Start with ₹1, perfect for daily or weekly savings.

- Instant Liquidity: Sell 24/7 at live market rates and get cash in your bank account instantly.

- Physical Redemption: You can convert your digital balance into physical coins or bars delivered to your doorstep.

- Cons:

- Spread & GST: Every purchase attracts 3% GST. There is also a "spread" (difference between buy and sell price) of roughly 2–5%.

- Regulatory Gap: While safe, it is not yet under a dedicated regulator like SEBI or RBI.

2. Gold ETFs: The Trader’s Best Friend

Gold Exchange Traded Funds (ETFs) are essentially mutual funds that track the domestic price of physical gold. Each unit is typically backed by 1 gram of 24K gold. These are traded on the stock exchange (NSE/BSE) just like shares.

- Pros:

- High Liquidity: You can buy and sell during market hours instantly through your Demat account.

- No Purity Risks: Since it is a regulated security, the gold backing the units is guaranteed to be 99.5% pure or higher.

- Low Tracking Error: ETFs track gold prices very closely with minimal friction.

- Cons:

- Demat Required: You must have a Demat and trading account.

- Expenses: You pay an annual "expense ratio" (management fee) of 0.5% to 1%, plus brokerage.

3. Sovereign Gold Bonds (SGBs): The Long-Term Tax Legend

Issued by the Reserve Bank of India (RBI) on behalf of the Government, SGBs are the "gold standard" for long-term investors. You don’t own physical gold, but a government bond linked to the gold price.

- Pros:

- Additional Interest: You earn a fixed interest of 2.5% per annum on your initial investment, paid semi-annually.

- Tax-Free Gains: If you hold the bond until its 8-year maturity, the capital gains are 100% tax-free.

- Government Backing: Zero risk of theft or purity issues.

- Cons:

- Lock-in Period: Maturity is 8 years, with exit options after the 5th year.

- Limited Availability: You can only buy from the primary market when the RBI opens a new "tranche" or through the secondary stock market.

The 2026 Taxation Cheat Sheet

The Union Budget 2026 has brought significant clarity to how gold is taxed. Here is the current status:

| Feature | Digital Gold | Gold ETF | SGB (Primary) |

|---|---|---|---|

| STCG (Short Term) | Taxed at slab (if <24 mo) | Taxed at slab (if <12 mo) | Taxed at slab (if sold on exchange) |

| LTCG (Long Term) | 12.5% (if >24 mo) | 12.5% (if >12 mo) | Exempt at Maturity |

| Indexation Benefit | No | No | Not applicable |

| Interest Income | N/A | N/A | Taxed at slab |

Note: As per the 2026 rules, secondary market SGB buyers (those who buy from the exchange rather than RBI directly) are now subject to capital gains tax even at maturity.

Comparison: Which One Wins?

To choose the right product, you must align it with your goal. Use this table as a quick reference:

| Factor | Digital Gold | Gold ETF | SGB |

|---|---|---|---|

| Minimum Spend | ₹1 | ~₹150 (1 unit) | 1 Gram (~₹7,500+) |

| Ease of Use | Extremely High (App) | Medium (Demat) | Medium (Bank/Portal) |

| Best For | Daily/Weekly Savings | Tactical Trading | Long-term Wealth |

| Safety | High (Insured Vaults) | Very High (SEBI) | Sovereign (RBI) |

| Ongoing Costs | Nil (first few years) | 0.5%–1% Expense Ratio | Zero |

The Stashfin Edge: Why Digital Gold Fits Your Lifestyle

At Stashfin, we believe in making wealth creation as seamless as taking a loan. Digital Gold is often the preferred choice for our users for three reasons:

- Low Friction: You don’t need to open a Demat account or wait for an RBI window. If you have ₹500 today, you can buy gold in 30 seconds.

- Emergency Buffer: Unlike SGBs, which lock your money away, Digital Gold is your emergency fund. If you need cash for an unplanned expense, you can sell your gold instantly.

- Gold SIPs: You can automate your savings. By buying small amounts consistently, you benefit from "Rupee Cost Averaging," protecting you from price volatility.

Final Verdict: The 2026 Strategy

In 2026, the "best" investment isn't one-size-fits-all. A smart investor uses a hybrid approach:

- For Long-term Goals (Retirement/Marriage): Allocate 50% to SGBs for the tax-free gains and 2.5% interest.

- For Portfolio Rebalancing: Use Gold ETFs to move in and out of the market easily based on trends.

- For Discipline & Emergencies: Keep a portion in Digital Gold via Stashfin. It’s the easiest way to ensure you are saving consistently without the overhead of a Demat account.

Ready to start? Gold is the ultimate hedge against inflation. Whether it's ₹1 or ₹1 Lakh, the best time to start was yesterday; the second-best time is now.