Different Types of Corporate Bonds: Introduction

Maximize your portfolio's potential by choosing the right debt instrument for your goals.

- Diversify across investment-grade and high-yield assets

- Understand the security of collateral-backed bonds

- Explore hybrid options like convertible bonds

- Identify bonds with callable or puttable features for maximum flexibility

Need a Comprehensive Guide to Types of Corporate Bonds?

In 2026, corporate bonds will become a staple for investors seeking higher returns than government securities without the extreme volatility of stocks. However, "corporate bond" is a broad term that covers a wide variety of instruments.

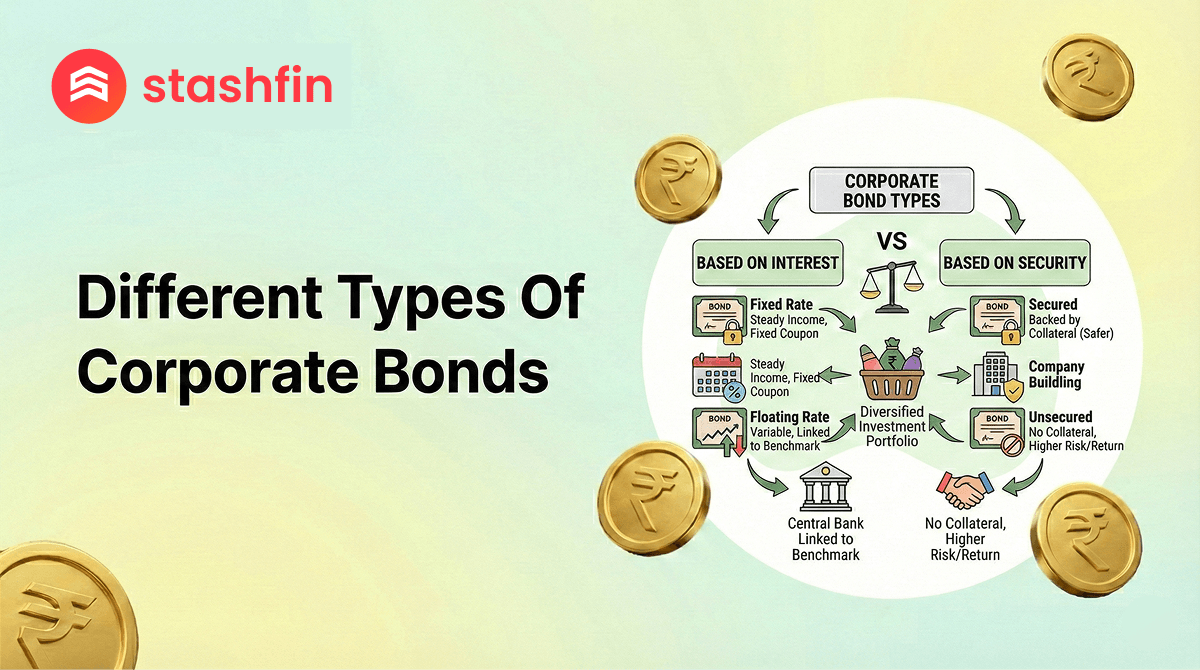

- By Interest: Choose between steady fixed-rate payments or market-linked floating rates.

- By Security: Protect your capital with secured bonds backed by company assets.

- By Convertibility: Participate in company growth by opting for convertible bonds.

- By Maturity: Align your cash flow with short-term, long-term, or even perpetual debt.

Understanding the various types of corporate bonds is the first step toward becoming a sophisticated debt investor.

[INSERT BOND YIELD CALCULATOR AVAILABLE ON WEALTH PAGE]

Features and Benefits of Different Corporate Bonds

Each of the types of corporate bonds offers a unique risk-reward profile. Depending on your strategy, you can unlock several benefits:

- Predictable Income: Fixed-rate "Vanilla" bonds provide a reliable coupon payment schedule.

- Inflation Protection: Floating-rate bonds adjust their interest based on market benchmarks (like MIBOR or SOFR).

- Capital Appreciation: Convertible bonds offer the safety of debt with the "upside" of equity.

- Lump-Sum Growth: Zero-coupon bonds are bought at a deep discount, providing a significant payout at maturity.

- Higher Yields: High-yield (Junk) bonds offer aggressive interest rates for investors with higher risk tolerance.

- Flexibility: Callable and puttable bonds allow either the issuer or the investor to exit the deal early if market conditions change.

Comparing the Main Types of Corporate Bonds

When navigating the market, it helps to categorize bonds based on their core functionality.

| Bond Type | Core Feature | Ideal For... |

|---|---|---|

| Secured Bonds | Backed by collateral (property/machinery). | Conservative, safety-first investors. |

| Convertible Bonds | Can be turned into company shares. | Investors seeking growth + income. |

| Zero-Coupon Bonds | No periodic interest; sold at a discount. | Retirement or child education funds. |

| Floating Rate Bonds | Interest resets based on market rates. | Hedging against rising interest rates. |

| Perpetual Bonds | No maturity date; pay interest forever. | Long-term steady cash flow needs. |

| Callable Bonds | Issuer can pay back the bond early. | Companies looking to refinance debt. |

Eligibility Criteria for Corporate Bond Investing

Investor Profile

To invest in any of the types of corporate bonds in 2026, you generally need to meet the following:

- Investor Type: Resident Individuals, HUFs, NRIs, and Institutional Investors.

- KYC Status: Active PAN, Aadhaar, and a verified bank account.

- Demat Account: Mandatory for holding and trading bonds in India.

- Minimum Investment: Can range from ₹1,000 for retail NCDs to ₹10 Lakhs for private placements.

Documentation

The process is 100% digital and straightforward:

- Identity Proof: Aadhaar Card or PAN.

- Financial Details: Cancelled check or bank statement for interest payouts.

- Risk Profile: Self-assessment of risk tolerance (especially for high-yield bonds).

How to Invest in Different Types of Corporate Bonds

- Analyse Your Goal: Do you need monthly income (Fixed-Rate) or a long-term corpus (Zero-Coupon)?

- Check Credit Ratings: Always look for ratings from agencies like CRISIL or ICRA (AAA is the safest).

- Choose Your Platform: Buy through a SEBI-registered broker, a dedicated bond platform, or during a public issue.

- Complete the Purchase: Units will be credited to your Demat account within T+1 or T+2 days.

Interest Rates & Risks Across Bond Types

| Bond Category | Expected Returns (2026) | Primary Risk |

|---|---|---|

| Investment Grade (AAA/AA) | 7.5% - 9.5% | Interest Rate Risk |

| High-Yield (A and Below) | 10% - 14% | Default/Credit Risk |

| Secured NCDs | 8% - 11% | Market Liquidity Risk |

| Convertible Bonds | 6% - 8% (Plus Equity Upside) | Equity Market Volatility |

Different Bonds for All Your Financial Needs

- Blue-Chip NCDs: For stable, safe monthly income.

- Infrastructure Bonds: Long-term growth with nation-building impact.

- Tech-Convertibles: Ride the wave of the next big startup.

- Short-Term Corporate Paper: Park surplus cash for 12–24 months.

- Distressed Debt: High-risk tactical plays for experienced traders.