Difference Between Tax Saving Bonds and Tax Free Bonds: Smart Tax Planning in 2026

Optimizing your tax liability requires a clear understanding of how different debt instruments are treated by the authorities.

- Learn why tax free bonds vs tax saving bonds offer different advantages

- Maximise your 80C deductions or enjoy zero tax on interest income

- Understand lock-in periods and liquidity options

- Build a tax-efficient portfolio for the 2026 fiscal year

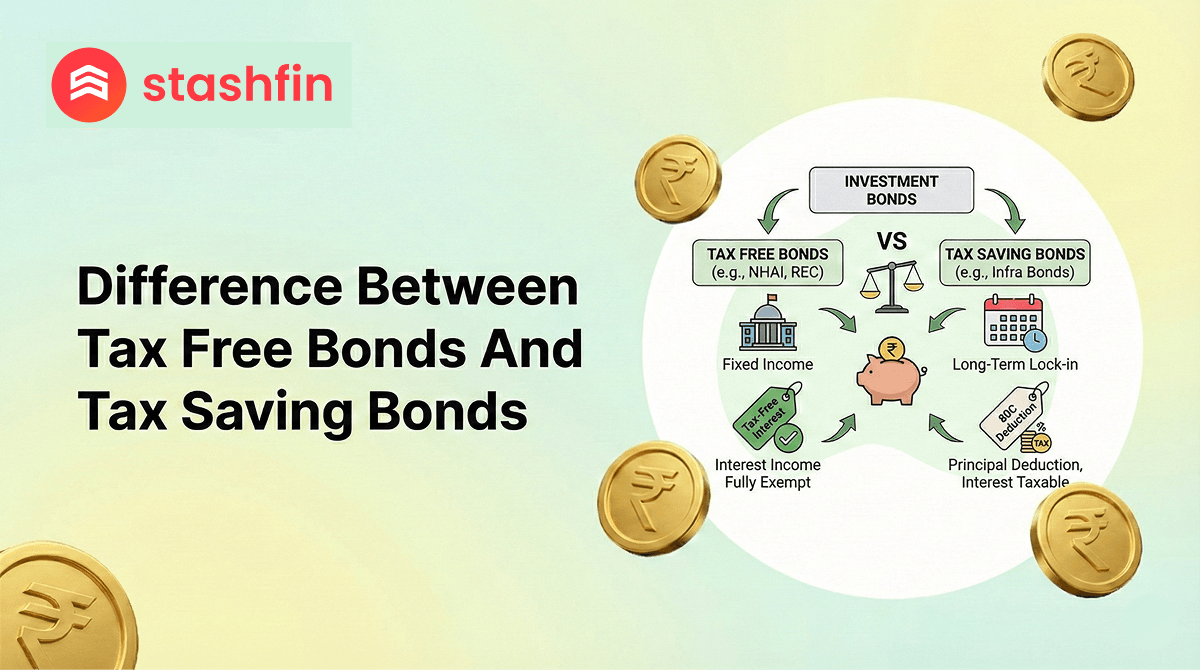

Are Tax Free Bonds & Tax Saving Bonds Same?

A common question among new investors is: "Are tax free bonds & tax saving bonds same?" The answer is a definitive no. While both help you manage your taxes, they do so in completely different ways.

- Tax Saving Bonds allow you to deduct the investment amount from your taxable income (usually under Section 80C). However, the interest you earn from them is typically taxable.

- Tax Free Bonds do not give you an initial deduction on the investment. Instead, the interest you earn every year is completely exempt from tax.

Understanding tax free bonds and tax saving bonds is essential for high-income earners looking to lower their "Effective Tax Rate."

Features and Benefits of Tax Free vs Tax Saving Bonds

Choosing between these two instruments depends on whether you want to save tax today on your income or tomorrow on your earnings.

- Immediate Tax Relief: Tax saving bonds provide an immediate reduction in your taxable income for the current financial year.

- Zero Tax on Interest: With tax-free bonds, the "Coupon" that hits your bank account is exactly what you get to keep, no TDS, no tax at the end of the year.

- Government Backing: Most of these bonds are issued by public sector undertakings (PSUs) like NHAI, REC, or HUDCO, offering high capital safety.

- Long-Term Wealth: Both are excellent for long-term goals, but tax-free bonds are particularly favored by those in the 30% tax bracket.

- Predictable Income: Enjoy a fixed interest rate that is usually higher than the post-tax return of a traditional Fixed Deposit.

Why Understanding Tax Free Bonds vs Tax Saving Bonds Matters

The fundamental difference between tax saving bonds and tax free bonds lies in where the tax benefit is applied: the principal or the interest.

| Feature | Tax Saving Bonds | Tax Free Bonds |

|---|---|---|

| Primary Tax Benefit | Deduction on the Investment Amount (e.g., Sec 80C). | Exemption on the Interest Income (Sec 10). |

| Tax on Interest | Taxable as per your income tax slab. | Completely Tax-Free. |

| Lock-in Period | Usually 5 to 7 years. | Long-term (10, 15, or 20 years). |

| Liquidity | Low (Cannot be sold before the lock-in). | Moderate (Traded on stock exchanges). |

| Ideal For | Salaried individuals looking to fill their 80C limit. | High Net-Worth Individuals (HNIs) in high tax brackets. |

| Investment Limit | Often capped (e.g., ₹1.5 Lakhs under 80C). | No upper limit (though retail category is capped). |

Eligibility Criteria for Tax-Efficient Investing

Investor Profile

To invest in tax free bonds and tax saving bonds in 2026, the criteria are generally broad:

- Resident Individuals: Most common category for tax benefits.

- Hindu Undivided Families (HUF): Eligible for tax deductions.

- NRIs: Can often invest in tax-free bonds on a non-repatriable basis (subject to specific bond terms).

- Senior Citizens: Often receive higher interest rates or priority allotment in certain issues.

Documentation

The process is 100% digital and transparent:

- KYC Documents: Aadhaar and PAN are mandatory.

- Demat Account: Most tax-free bonds are issued and traded in dematerialized form.

- Bank Details: For the direct credit of interest (Coupon) and principal at maturity.

How to Invest: Tax Saving vs Tax Free Bonds

- Identify Your Gap: Check if you have already exhausted your Section 80C limit (for tax saving bonds).

- Primary vs Secondary Market: Tax-free bonds are rarely issued as new IPOs in 2026; most investors buy them on the Secondary Market (Stock Exchange).

- Check the YTM: Always look at the Yield to Maturity, as bonds bought at a premium on the exchange will have a lower actual yield than the coupon rate.

- Complete the Purchase: Use your trading app to buy units of PSU bonds like PFC, IRFC, or NHAI.

Interest Rates & Financial Details

| Financial Aspect | Tax Saving Bonds (Typical) | Tax Free Bonds (Secondary Market) |

|---|---|---|

| Nominal Interest Rate | 7% - 8.5% | 5% - 6.5% |

| Effective Post-Tax Yield | Lower (due to tax on interest) | Higher (for those in 30% tax bracket) |

| TDS (Tax Deducted at Source) | Applicable | Not Applicable |

| Transferability | Restricted during lock-in | Fully transferable on exchanges |