Coupon Rate vs. Bond Yield: Mastering the Key Differences

Know exactly what you earn and how market shifts impact your bond returns.

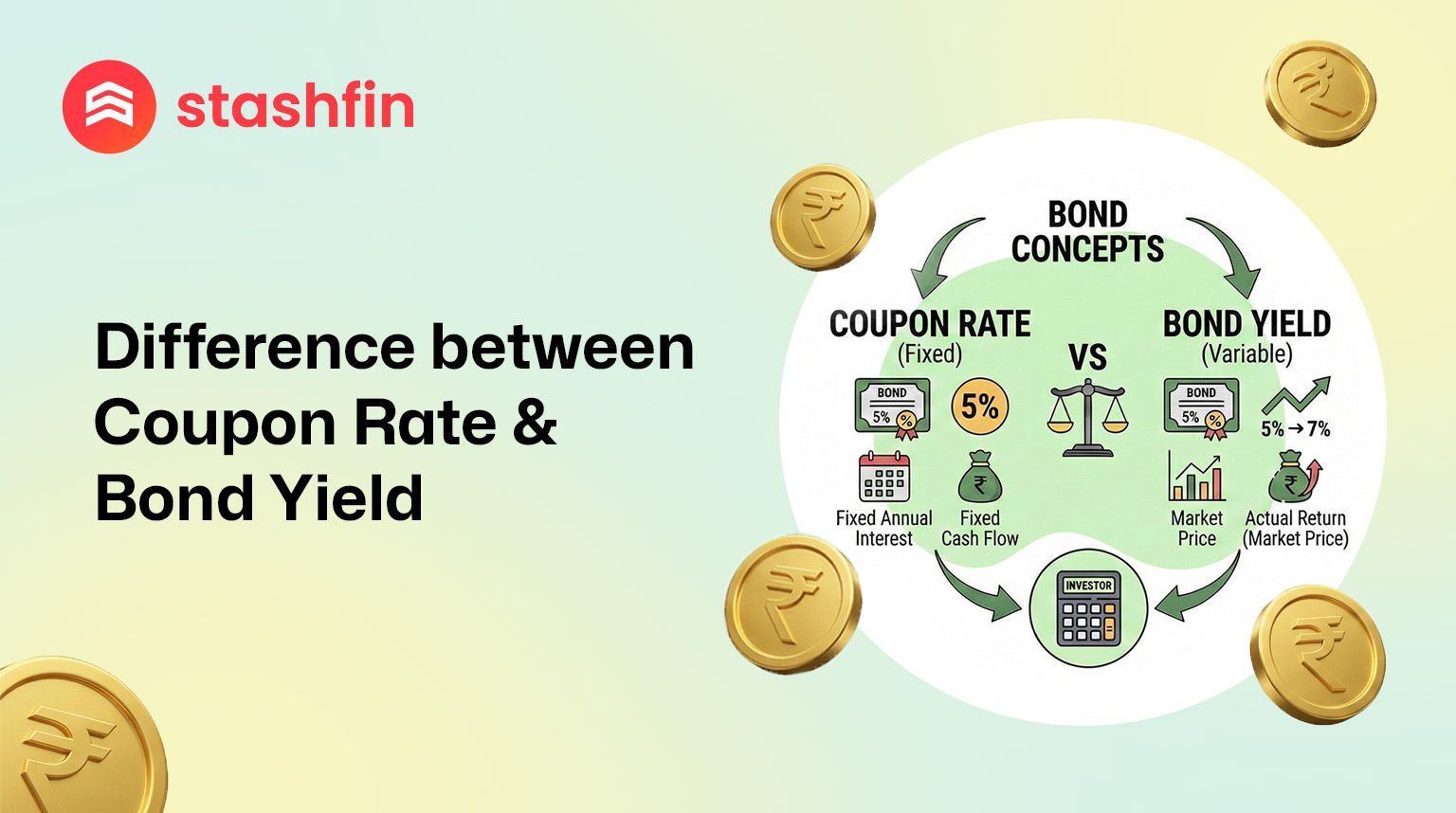

- Fixed vs. Dynamic: One is set in stone at issuance, while the other fluctuates every second the bond is traded.

- Income vs. Total Return: Coupons represent your "salary" from the bond; yield represents the total "value" of the deal.

- Market Sensitivity: With the 2026 Repo Rate at 5.25%, bond yields adjust to remain competitive with the central bank’s benchmarks.

- Secondary Market Navigation: Yield is the only way to compare bonds bought at different prices (premium vs. discount).

Defining the Terms: Coupon and Yield

To navigate the bond market, you must distinguish between the "sticker price" of interest and your actual "take-home" return.

What is the Coupon Rate in a Bond?

The coupon rate is the fixed annual interest rate that the bond issuer agrees to pay on the bond's face value (par value). It remains unchanged throughout the life of the bond (for fixed-rate bonds).

Calculation: It is always a percentage of the face value, not the price you paid. For example, a bond with a ₹1,000 face value and a 10% coupon rate will pay exactly ₹100 every year, regardless of whether the bond's market price rises to ₹1,100 or drops to ₹900.

What is Bond Yield?

Bond yield is a measure of the actual return an investor receives, relative to the bond's current market price. It changes daily as the bond's market price fluctuates. For instance, if you buy a bond at a discount (below face value), your yield will be higher than the coupon rate. If you buy at a premium (above face value), your yield will be lower.

Coupon Rate vs. Yield to Maturity (YTM)

The most comprehensive way to measure bond returns is Yield to Maturity (YTM). Unlike "Current Yield," which only looks at the next year of income, YTM factors in the time value of money, reinvestment of coupons, and any capital gain or loss at maturity.

Comparison Table: At a Glance

| Feature | Coupon Rate | Yield to Maturity (YTM) |

|---|---|---|

| Basis | Fixed on Face Value | Based on Purchase Price & Cash Flows |

| Nature | Predetermined and Static | Market-driven and Fluctuating |

| Formula | Annual Coupon / Face Value | Complex IRR Calculation |

| Relevance | Best for Primary Market Buyers | Best for Secondary Market Buyers |

| Insight | Shows promised annual interest | Shows expected total return |

Why the Difference Matters (2026 Scenarios)

With the RBI Repo Rate at 5.25%, the gap between coupon and yield tells a specific story about a bond's value.

- Buying at Par: If you buy a bond at its face value (e.g., during a new issue), your Coupon Rate = Yield.

- Buying at a Discount: If market rates rise, bond prices fall. Buying a 14.5% Akara Capital Bond at ₹950 (instead of ₹1,000) means your Yield > 14.5% because you earn interest plus a ₹50 gain at maturity.

- Buying at a Premium: If you pay ₹1,050 for that same bond, your Yield < 14.5% because the interest you earn is offset by the ₹50 loss you take when the bond matures at ₹1,000.