Call Money vs. Notice Money: Mastering Short-Term Liquidity

The primary mechanism for interbank lending and reserve management.

- Speed of Access: Borrow or lend funds almost instantly via electronic platforms like NDS-CALL.

- Unsecured Nature: These transactions are typically uncollateralised, relying on the creditworthiness of banks and primary dealers.

- Repo Rate Linkage: Yields in this market are highly sensitive to the 5.25% RBI Repo Rate and overall systemic liquidity.

- Regulatory Limits: The RBI enforces strict "Prudential Limits" on how much an institution can borrow or lend in this segment.

Call Money vs. Notice Money: Key Differences

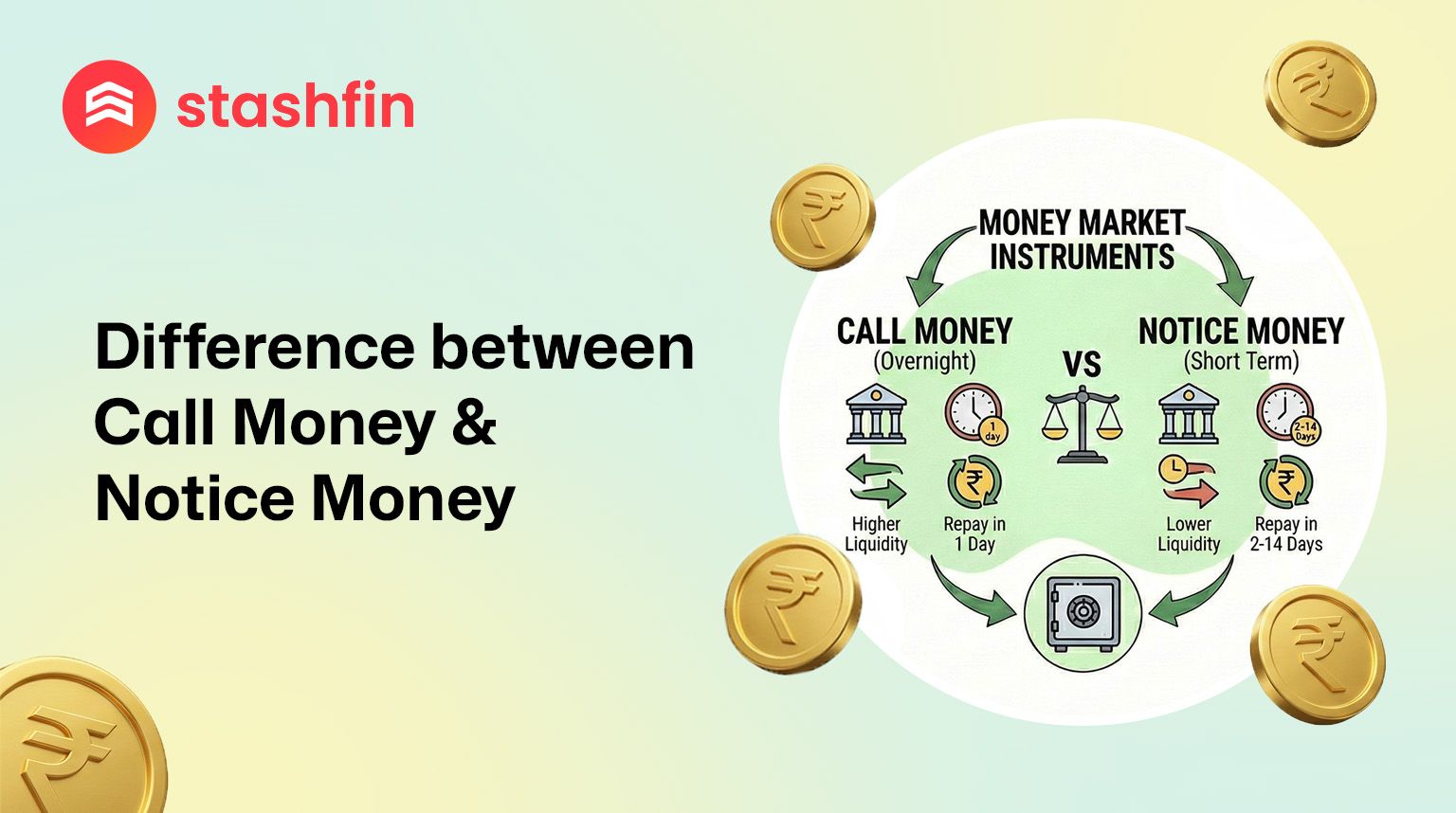

The fundamental difference between call money and notice money lies in the tenure of the transaction. Both are used by banks to cover temporary mismatches in cash flows or to fulfill the Cash Reserve Ratio (CRR).

| Feature | Call Money | Notice Money |

|---|---|---|

| Tenure | 1 Day (Overnight) | 2 Days to 14 Days |

| Maturity | Funds are returned the next business day. | Funds are returned after the notice period (within 14 days). |

| Purpose | Immediate overnight liquidity and CRR balancing. | Short-term liquidity management over a 2-week fortnight. |

| Interest Rate | Volatile; changes based on daily liquidity. | Slightly more stable than call money rates. |

| Collateral | Unsecured (No collateral required) | Unsecured (No collateral required) |

Participants and Regulations in 2026

The Call/Notice Money Market is an exclusive, highly regulated segment of the Indian financial system. To prevent systemic risk, the RBI limits participation and borrowing capacity.

Eligible Participants

- Scheduled Commercial Banks (SCBs): Both as borrowers and lenders (excluding Regional Rural Banks).

- Co-operative Banks: (Other than Land Development Banks).

- Primary Dealers (PDs): Act as intermediaries in the government securities market and use this market for funding gaps.

Prudential Limits (RBI Mandates)

- Borrowing Limit for SCBs: Typically capped at 100% of their capital funds on a fortnightly average basis.

- Lending Limit for SCBs: Usually limited to 25% of their capital funds on a fortnightly average basis.

- Reporting: All OTC deals must be reported within 15 minutes on the NDS-CALL platform.

How Interest Rates are Determined

Interest rates in the call and notice money markets are known as the Weighted Average Call Rate (WACR). In 2026, these rates fluctuate within a "corridor" established by the RBI:

- Repo Rate (5.25%): Serves as the primary benchmark. If the WACR drifts significantly above 5.25%, it signals a liquidity shortage.

- Marginal Standing Facility (MSF): Acts as the upper ceiling of the corridor.

- Standing Deposit Facility (SDF): Acts as the lower floor of the corridor.

Why This Matters for Your Portfolio

While retail investors cannot directly participate in the call money market, its performance affects your investments:

- FD and Bond Rates: If call money rates stay high, it indicates banks are hungry for funds, which may lead to a rise in Corporate Bond Yields and FD Interest Rates.

- Market Stability: A stable call money market prevents "liquidity crunches," ensuring that banks can process withdrawals and maintain lending operations smoothly.

- High-Yield Opportunities: When bank liquidity is tight, high-growth NBFCs may offer premium rates on instruments like Akara Capital Bonds (14.5% p.a.) to attract direct retail capital.