Definitive Guide to Negotiating Lower Interest Rates on Personal Loans

In the financial landscape of 2026, personal loans have become a cornerstone of urban lifestyle management. Whether you are consolidating debt, funding a high-end wedding in a Tier-1 city, or managing a medical emergency, the interest rate you secure can be the difference between a manageable EMI and a long-term debt trap.

Contrary to popular belief, the interest rate quoted on a lending app or website is often not set in stone. As lenders compete for high-quality borrowers in an increasingly digital market, your ability to negotiate can save you thousands of rupees over the loan tenure.

1. Leverage Your Credit Score: The 750+ Advantage

In 2026, credit scores are the ultimate bargaining chip. Most lenders in India now use risk-based pricing, offering lower rates to "Low Risk" profiles.

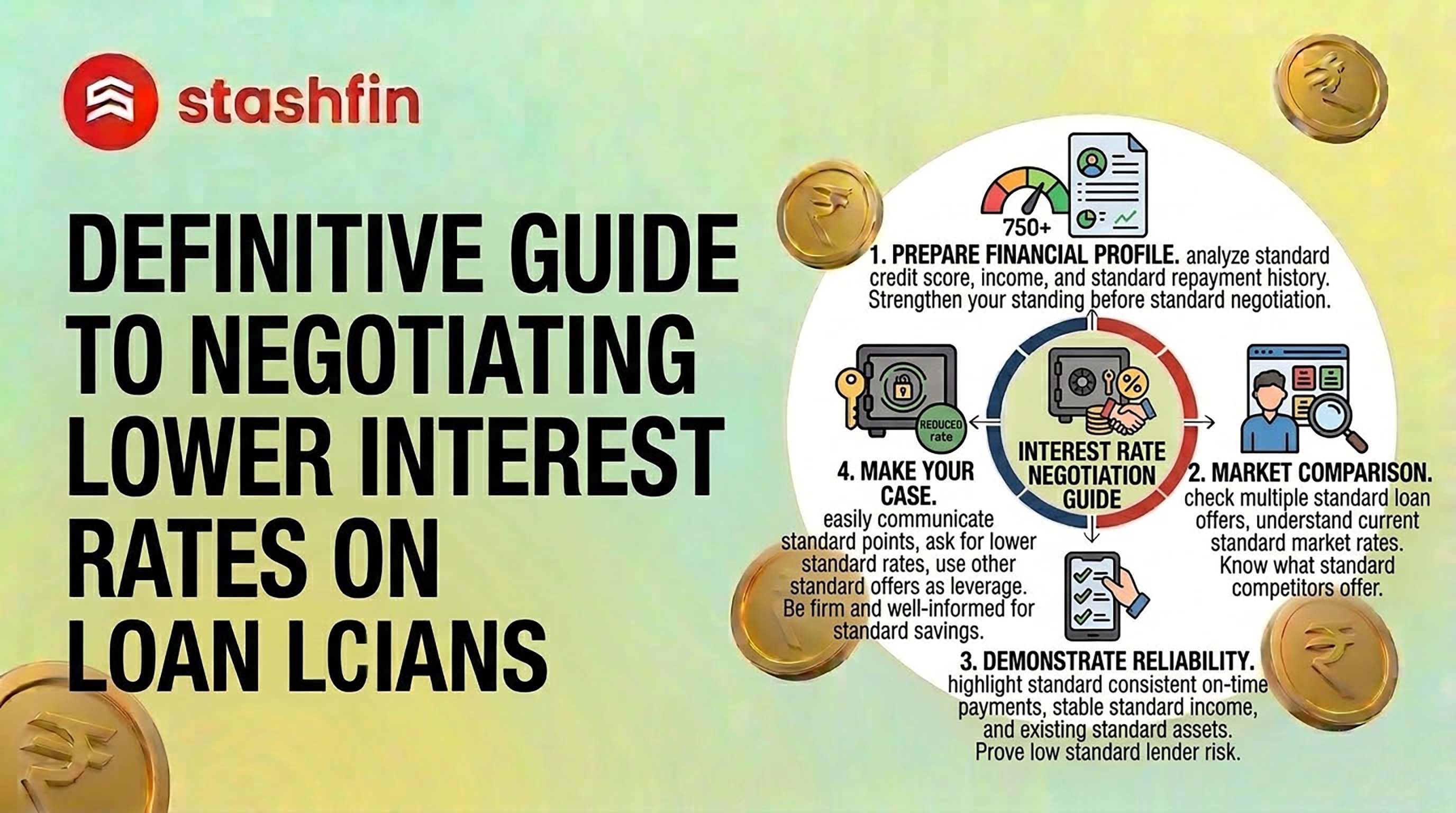

- Know Your Number: Before initiating any conversation, check your CIBIL or Experian score. A score of 750 or higher puts you in the elite bracket.

- The Negotiation Move: Explicitly mention your high score. If a lender quotes 14% p.a., but competitors offer 11% p.a. to 750+ scorers, use that data to ask for a rate revision.

- Fix Errors First: Ensure your report is clean before you negotiate, as simple reporting errors can artificially inflate your rate.

2. The "Existing Relationship" Strategy

Lenders value loyalty because it reduces their "customer acquisition cost."

- Salary Accounts & FDs: If your salary is credited to a specific bank or if you hold substantial Fixed Deposits (FDs), the lender has clear visibility of your stable cash flow.

- The Negotiation Move: Ask for a "Loyalty Discount." Relationship managers often have the authority to shave off 0.25% to 0.50% from the standard rate or waive processing fees (which can be as high as 3%).

3. Compare and Conquer: Use Competing Offers

Never accept the first offer. In 2026, digital platforms allow you to gather multiple pre-approved quotes in minutes via soft inquiries.

- Gather Proof: Secure written quotes or screenshots of "pre-approved" offers from at least 2–3 digital lenders or NBFCs.

- The Negotiation Move: Use direct comparisons: "Bank X is offering me 10.99% with zero processing fees. Can you match or beat this?" Lenders are often willing to drop rates to avoid losing a high-quality customer to a rival.

4. Optimise Your Debt-to-Income (DTI) Ratio

Lenders calculate your repayment capacity by looking at how much of your salary goes toward existing EMIs. Ideally, this should be below 40%.

- Clean Up Small Debts: Clear minor credit card dues or small BNPL (Buy Now Pay Later) outstandings before applying.

- The Negotiation Move: A lower DTI ratio proves you have high disposable income. Use this stability to argue for a lower "risk premium" on your interest rate.

Strategy Checklist for Lower Rates (AY 2026-27)

| Negotiation Factor | Impact on Rate | Why it Works |

|---|---|---|

| Credit Score 750+ | High (1-2% drop) | Signals low default risk. |

| Shorter Tenure | Medium (0.5% drop) | Reduces lender's long-term risk exposure. |

| Employer Reputation | Medium (0.5% drop) | Fortune 500/Govt. roles ensure income stability. |

| Festive/Special Offers | Variable | Lenders have targets during Diwali/Year-end. |

| Balance Transfer | High (Significant) | Moving high-interest debt to a new lender. |

5. Negotiate the "Hidden" Costs

If the lender is rigid on the interest rate, pivot your negotiation to fees:

- Processing Fees: These range from 1% to 4%. Always ask for a 100% waiver.

- Foreclosure/Prepayment Charges: Many fintechs like Stashfin offer zero foreclosure charges. If your lender charges them, negotiate to have them removed so you can save on interest by paying off the loan early.

Conclusion

Negotiating a personal loan is about presenting a data-backed case for why you are a low-risk, high-value customer. By maintaining a stellar credit score and strategically comparing offers, you can significantly reduce your borrowing costs. Even a 1% reduction on a ₹5 Lakh loan over 3 years can save you over ₹8,000–₹10,000 in total interest.