Credit Period Vs Lead Time: Understanding the Difference for Better Supply Chain Management

In the world of supply chain and business finance, terminology matters. Two terms that are frequently used but often confused are credit period and lead time. While both concepts are deeply tied to the movement of goods and money within a supply chain, they refer to entirely different aspects of business operations. For logistics managers, procurement officers, and business owners, understanding the distinction between these two terms is not just an academic exercise — it directly influences how a business plans its inventory, manages its finances, and builds relationships with suppliers and customers.

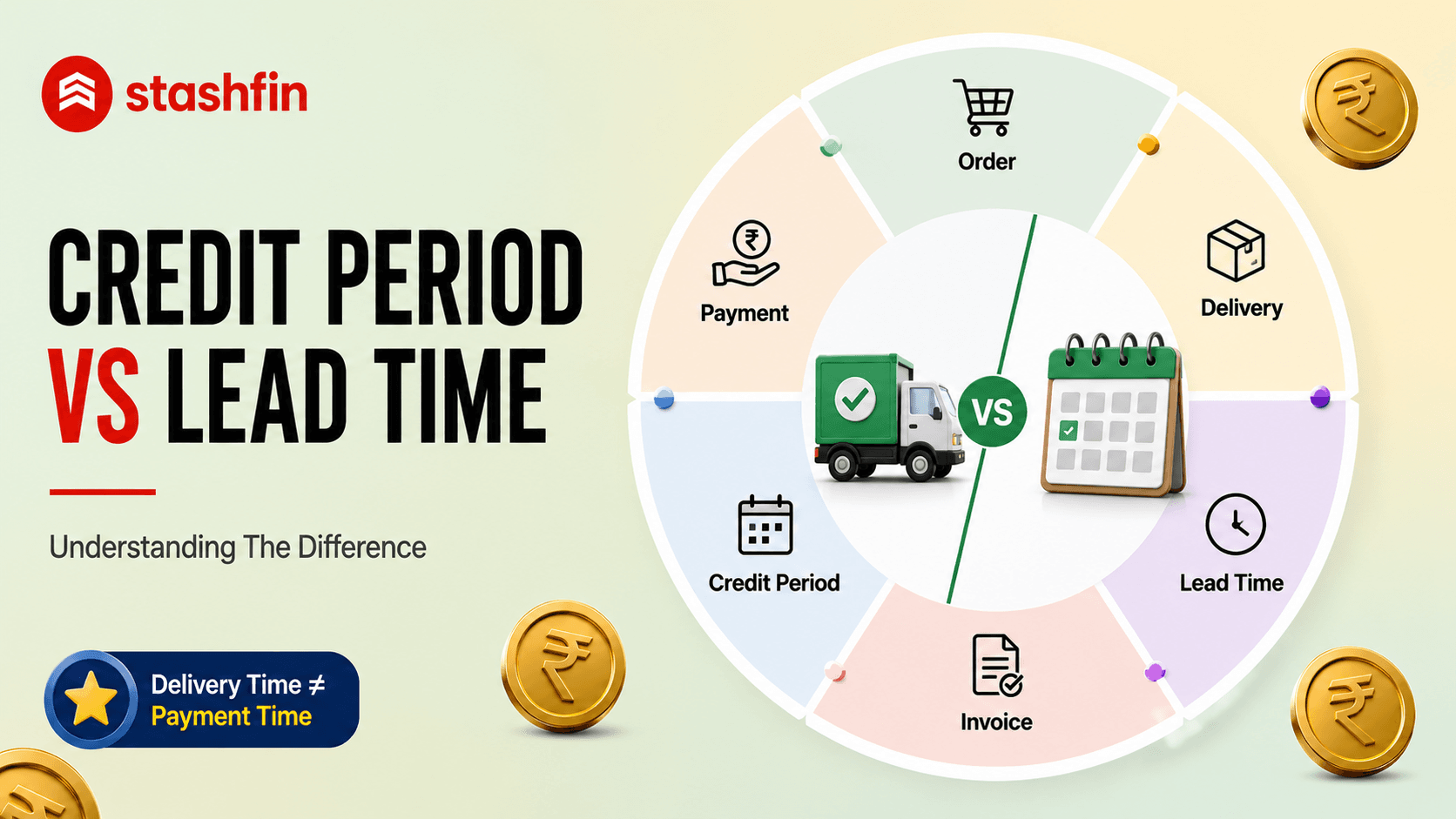

What Is Lead Time?

Lead time refers to the total amount of time that elapses between the moment an order is placed and the moment the goods or services are actually received by the buyer. In supply chain management, lead time encompasses every stage of the fulfilment process. This includes the time taken by a supplier to acknowledge an order, the time required for manufacturing or processing, the time spent in transit, and the time needed for any customs clearance or final delivery steps.

Lead time is fundamentally about the physical and logistical flow of goods. It is a measure of operational efficiency. A shorter lead time generally indicates a more responsive supply chain, while a longer lead time may point to inefficiencies, geographical constraints, or complex production processes. Logistics managers track lead time closely because it determines how far in advance orders must be placed to ensure that stock levels remain adequate and that production schedules are not disrupted.

Lead time is also a critical input in inventory planning. Businesses that rely on just-in-time inventory models are particularly sensitive to lead time variability. When lead times are unpredictable, businesses must hold larger safety stock buffers to absorb uncertainty, which ties up working capital unnecessarily.

What Is Credit Period?

Credit period, on the other hand, refers to the duration of time that a buyer is granted by a seller to make payment for goods or services already received. It is a financial arrangement that exists between trading partners and is typically agreed upon at the time of purchase or as part of a standing commercial relationship.

When a supplier extends a credit period to a buyer, they are essentially offering short-term financing. The buyer receives the goods immediately or within the lead time but is not required to make payment until the credit period expires. This arrangement gives businesses the breathing room to sell their inventory, collect revenue from their own customers, and then use those proceeds to pay their suppliers — without dipping into their own cash reserves prematurely.

Credit period is a financial concept, not a logistical one. It deals with the timing of money, not the timing of delivery. Businesses that can negotiate favourable credit periods with their suppliers enjoy improved liquidity and greater flexibility in managing their working capital cycles.

Credit Period Vs Lead Time: The Core Distinction

The most important distinction between credit period and lead time is the domain each belongs to. Lead time is an operational and logistical metric — it tells you how long it takes to get what you ordered. Credit period is a financial and commercial metric — it tells you how long you have before you need to pay for what you ordered.

Consider a straightforward example. A retailer places an order with a supplier. The goods arrive ten days after the order is placed — that ten-day window is the lead time. The supplier then gives the retailer thirty days from the date of invoice to make payment — that thirty-day window is the credit period. These two timelines can overlap, run sequentially, or be entirely independent depending on when the invoice is issued relative to when delivery occurs.

Understanding both figures simultaneously is what allows a logistics manager to build a complete picture of the cash conversion cycle. If the credit period ends before the retailer has had a chance to sell the goods and collect payment from customers, the business may face a liquidity squeeze. On the other hand, if the credit period extends well beyond the point at which inventory has been sold, the business enjoys a comfortable float.

Why Both Metrics Matter in Supply Chain Planning

For businesses operating in competitive markets, the interplay between lead time and credit period can make a significant difference to financial health. A long lead time combined with a short credit period is a difficult combination — it means a business must pay for goods before they even arrive or very shortly after. This can strain cash flow significantly.

Conversely, a short lead time combined with a long credit period represents an ideal scenario. Goods arrive quickly and can be processed or sold, while the business retains use of its cash for an extended period before the payment obligation falls due.

Supply chain professionals who understand this interplay are better positioned to negotiate with suppliers, set appropriate reorder points, and communicate meaningfully with finance teams about working capital requirements. The vocabulary around these two terms should not be used interchangeably, as doing so can create confusion in cross-functional discussions between logistics, procurement, and finance departments.

How Credit Period Influences Supplier Relationships

The credit period extended by a supplier is not arbitrary. It reflects the supplier's assessment of the buyer's creditworthiness, the commercial relationship between the two parties, and prevailing industry norms. Buyers who have a strong payment history and a long-standing relationship with their suppliers are often able to negotiate more favourable credit periods.

From the supplier's perspective, extending a credit period is a form of financial exposure. They have delivered goods but have not yet received payment. To manage this risk, suppliers may factor credit period terms into their pricing. This is why understanding credit period is not just about cash flow management — it also influences the total cost of procurement.

For businesses looking to optimise their supply chain financing, exploring financial products that support the working capital cycle during the gap between lead time and credit period obligations can be a sensible strategy. Stashfin offers a free credit period facility that can help businesses manage short-term cash flow needs without unnecessary strain on their finances.

Managing the Gap Between Delivery and Payment

One practical challenge that many businesses face is managing the gap between when goods arrive and when payment is due. If lead time is long and credit period is short, this gap can create operational pressure. Businesses may need to make payment while goods are still in transit or have only recently arrived, before any revenue has been generated from those goods.

Effective supply chain managers work to align these two timelines as closely as possible to the natural cash conversion cycle of their business. This involves negotiating lead times with logistics providers, discussing credit period terms with suppliers, and using appropriate financial tools to bridge any remaining gaps.

Digital financial platforms like Stashfin make it easier for businesses and individuals to access credit period benefits without complex paperwork or lengthy approval processes. By leveraging such tools, businesses can focus on their core operations while maintaining financial flexibility.

Practical Tips for Logistics Managers

Always track lead time and credit period separately in your financial planning models. Conflating the two can lead to inaccurate cash flow forecasts. When evaluating a new supplier, consider both the lead time they offer and the credit period they are willing to extend — neither should be assessed in isolation. Build a buffer into your reorder planning that accounts for lead time variability. A supplier who usually delivers in ten days may occasionally take longer, and your credit period terms will not adjust to accommodate that. Work closely with your finance team to ensure that payment schedules align with actual inventory turnover rates. If goods take time to sell, a very short credit period may create unnecessary working capital pressure. Finally, review your credit period arrangements periodically. As your business grows and your payment history strengthens, you may be in a position to negotiate more favourable terms.

Conclusion

Credit period and lead time are two distinct concepts that together form the foundation of effective supply chain financial management. Lead time tells you when goods will arrive; credit period tells you when you need to pay. Both must be understood, tracked, and managed with equal care. Logistics managers who master the relationship between these two metrics are far better equipped to optimise working capital, reduce financial risk, and build resilient supply chains. If you are looking for financial flexibility in managing your payment obligations, explore what Stashfin's free credit period offering can do for you. Get Your Free Credit Period on Stashfin today and take control of your business cash flow.

Credit products are subject to applicant eligibility, credit assessment, and applicable interest rates. Stashfin is an RBI-registered NBFC. Please read all terms and conditions carefully.