Commercial Paper vs. Certificate of Deposit: Introduction

What are Commercial Papers and Certificates of Deposit?

In the 2026 financial landscape, these two instruments serve as the primary "short-term lungs" of the economy, allowing banks and businesses to manage their daily cash needs.

Download Stashfin App

- What is Commercial Paper (CP)?

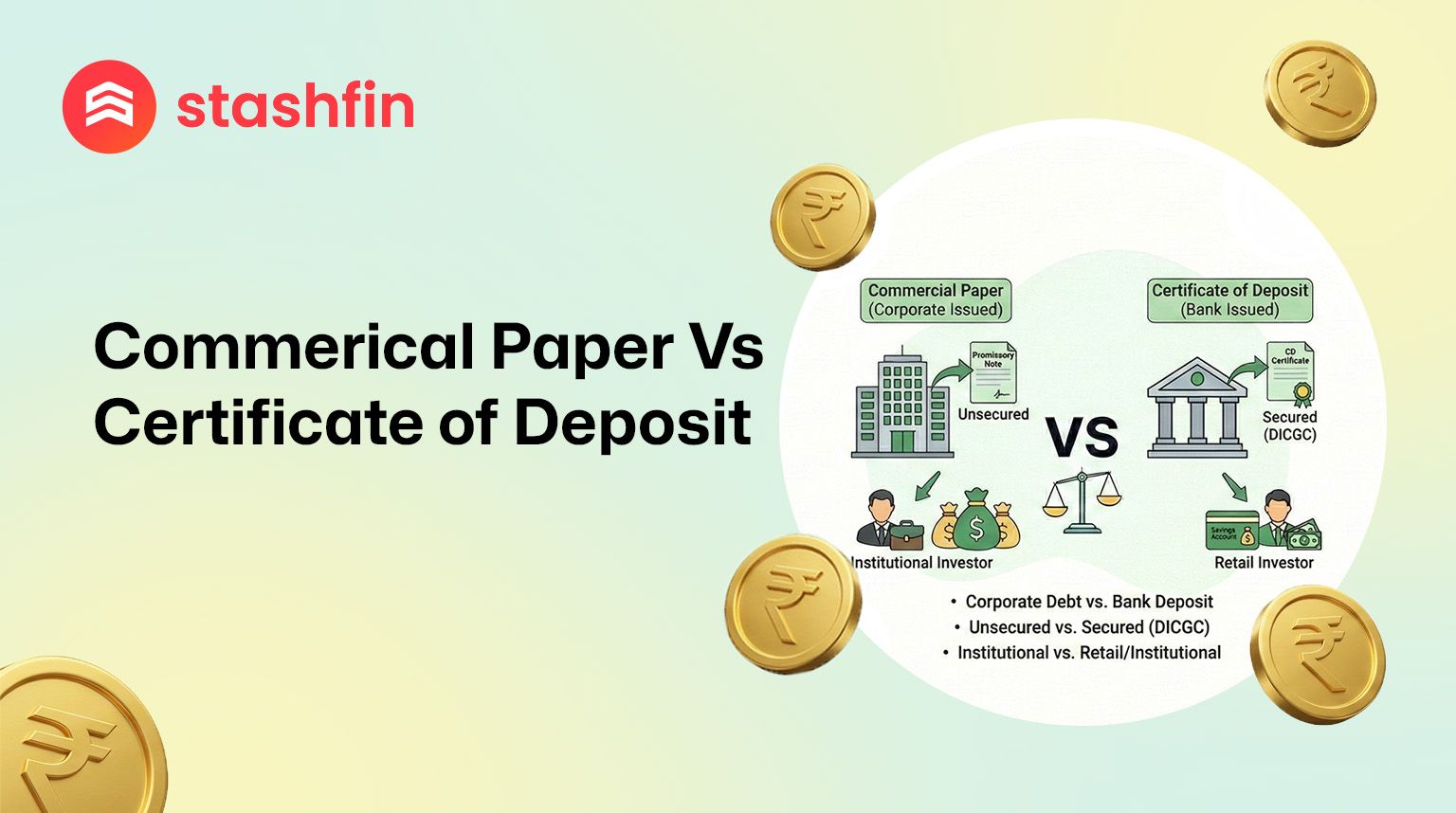

Commercial Paper is an unsecured money market instrument issued in the form of a promissory note. It allows highly-rated corporate borrowers to diversify their sources of short-term funding. Because it is unsecured, CP relies entirely on the issuer's creditworthiness. - What is a Certificate of Deposit (CD)?

A Certificate of Deposit is a negotiable money market instrument issued in dematerialised form against funds deposited at a bank or eligible financial institution. Think of it as a "tradable fixed deposit" used by banks to raise large-scale wholesale resources.

Key Differences: Commercial Paper vs. Certificate of Deposit

While both are short-term and traded in multiples, the difference between commercial paper and certificate of deposit lies in the issuer's profile and the underlying security.

| Feature | Commercial Paper (CP) | Certificate of Deposit (CD) |

|---|---|---|

| Primary Issuer | Corporates, PDs, & FIs | Scheduled Commercial Banks |

| Nature of Debt | Unsecured (Promissory Note) | Secured (Bank Deposit Base) |

| Minimum Investment | ₹5 Lakh | ₹1 Lakh |

| Standard Tenure | 7 Days to 1 Year | 7 Days to 1 Year (Banks) |

| Risk Level | Higher (Credit-dependent) | Lower (Bank-backed) |

| Target Return | ~7.5% - 8.5% p.a. | ~7.0% - 7.8% p.a. |

Features and Benefits of Commercial Paper

- Cost Efficiency: Large companies raise funds cheaper than bank loans.

- High-Yield Potential: Typically offers a higher interest rate than CDs to compensate for lack of collateral.

- Liquidity: Tradable in the secondary market in demat form.

Features and Benefits of Certificate of Deposit

- Institutional Safety: Backed by the robust balance sheets of regulated banks.

- Predictability: Offers assured returns unaffected by market volatility.

- Negotiability: Unlike FDs, these can be sold to other investors if you need cash before maturity.

The Retail Perspective: Why 14.5% Bonds Stand Out

Commercial Papers and CDs are primarily designed for institutional "wholesale" players with high minimum ticket sizes (₹1L–₹5L). For retail investors seeking similar stability with significantly higher "Alpha," Akara Capital Bonds provide a more accessible alternative.

| Feature | Institutional CP/CD | Akara Capital Bonds |

|---|---|---|

| Annual Yield | ~7.0% - 8.5% p.a. | 14.5% p.a. |

| Payout Frequency | At Maturity | Fixed Monthly Returns |

| Entry Point | ₹1 Lakh - ₹5 Lakh | ₹10,000 |

| Tenure | Up to 1 Year | 1 Year (Standard) |

Regulatory Framework in India (2026)

Both instruments are governed by the Reserve Bank of India (RBI) to maintain market integrity:

- Credit Ratings: CPs must have a minimum credit rating (typically A3 or better). CDs do not strictly require ratings but depend on the bank's standing.

- Demat Mandatory: All issuances must be in electronic form through NSDL or CDSL.

- RBI Repo Rate Impact: As the Repo Rate stands at 5.25%, the yields on these instruments are closely tied to the central bank's liquidity stance.