CD vs. FD: Which Fixed-Income Tool is Right for You?

Understanding CD vs. Term Deposit

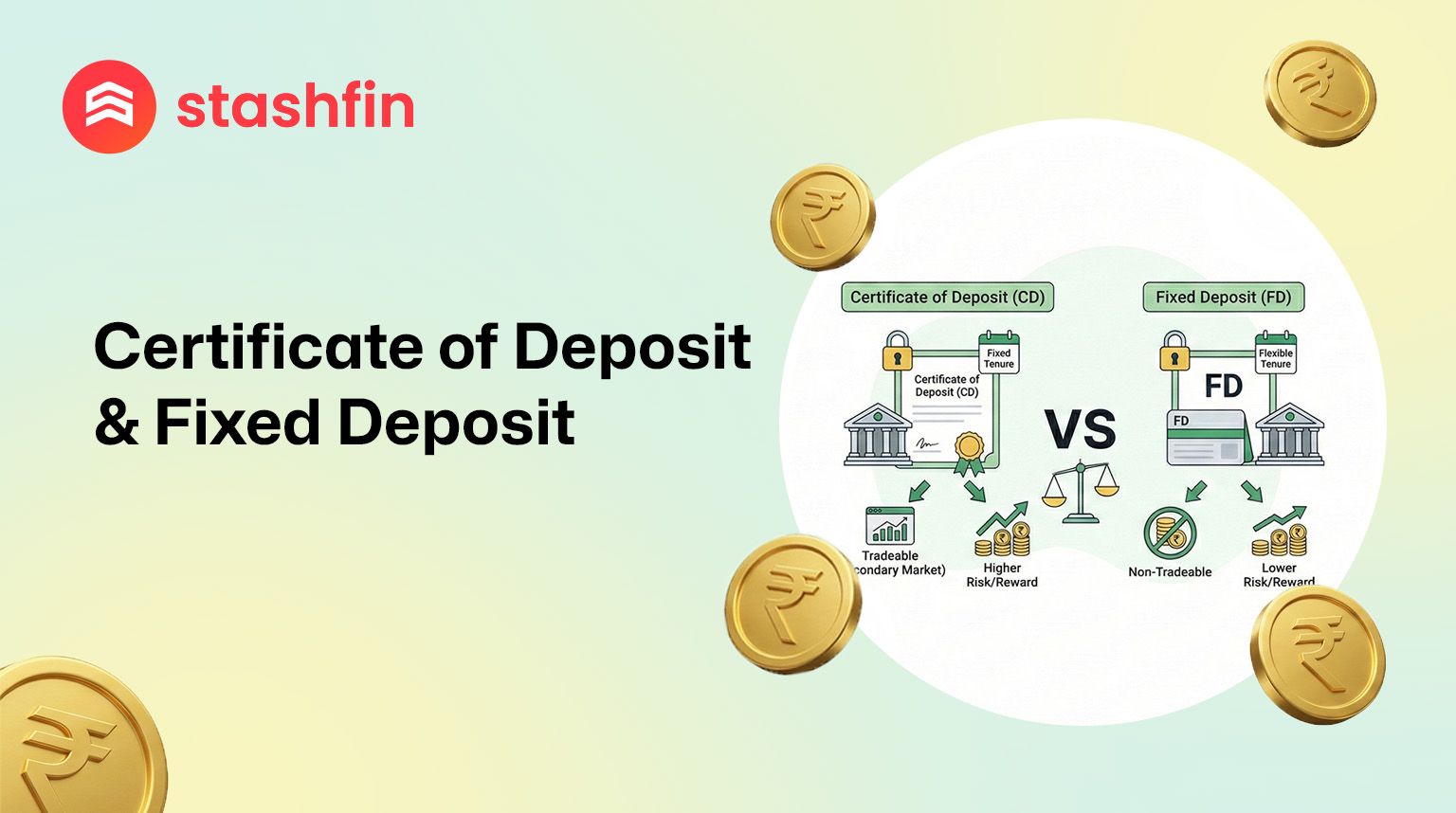

While both are time-based deposits where you lock in funds for a fixed rate, a Certificate of Deposit (CD) and a Fixed Deposit (FD) serve different investor profiles.

Download Stashfin App

- Fixed Deposit (FD): A contract with a bank where you deposit a sum for a set period. It is designed for retail individuals, offering safety and the convenience of premature withdrawal (with a penalty).

- Certificate of Deposit (CD): A negotiable money market instrument issued in dematerialised form. It is primarily used by corporations and HNIs to park large surpluses for short durations.

Key Differences: Certificate of Deposit vs. Fixed Deposit

In the 2026 landscape, the difference between CD and FD is defined by liquidity, accessibility, and the ability to leverage your assets.

| Feature | Certificate of Deposit (CD) | Fixed Deposit (FD) | Akara Capital Bonds |

|---|---|---|---|

| Minimum Investment | ₹1 Lakh (and multiples) | Typically ₹1,000 | ₹10,000 |

| Annual Return | ~7.5% - 8.2% p.a. | ~6.5% - 7.5% p.a. | 14.5% p.a. |

| Standard Tenure | 7 Days to 1 Year (Banks) | 7 Days to 10 Years | 1 Year |

| Transferability | Negotiable/Transferable | Non-Transferable | Tradable (Secondary) |

| Loan Facility | Not Allowed | Available (up to 90%) | Not Allowed |

| Senior Citizen Rate | No special rates | Extra 0.50% - 0.75% | 14.5% for all |

Features and Benefits of Fixed Deposit (FD)

- Accessibility: You can start an FD with as little as ₹1,000.

- Liquidity via Loans: Most banks allow you to take an instant loan/overdraft against your FD without breaking the deposit.

- Safety Net: Deposits up to ₹5 Lakh are insured by the DICGC.

- Retirement Friendly: Senior citizens get significantly higher rates compared to the general public.

Features and Benefits of Certificate of Deposit (CD)

- Negotiability: Unlike FDs, you can sell your CD to another investor in the secondary market if you need to exit before maturity.

- Institutional Yields: CDs often offer a slightly higher rate than standard FDs because they are issued in large volumes to institutional players.

- Fixed Tenure: Ideal for parking corporate funds for exactly 3, 6, or 12 months.

Why Stashfin for High-Yield Bond Investing?

If you are considering a CD or FD for its "fixed" nature but want a significantly higher return, Akara Capital Bonds provide the perfect middle ground.

| Benefit | Stashfin | Traditional CDs/FDs |

|---|---|---|

| Return Target | 14.5% Fixed p.a. | Capped around 7-8% |

| Payout Frequency | Guaranteed Monthly | Often only at Maturity |

| Onboarding | 100% Digital & Instant | May require branch visits |

| Tenure | 1 Year | Rigid cycles |

When to Choose What?

- Choose an FD if you need the safety of DICGC insurance, have a small amount to invest, or want the ability to take a loan against your deposit.

- Choose a CD if you have at least ₹1 Lakh, want a negotiable instrument, and are looking for institutional-grade bank yields.

- Choose Akara Capital Bonds if you want to maximise your income (14.5%), need fixed monthly cash flow, and have a short-term horizon of 1 year.