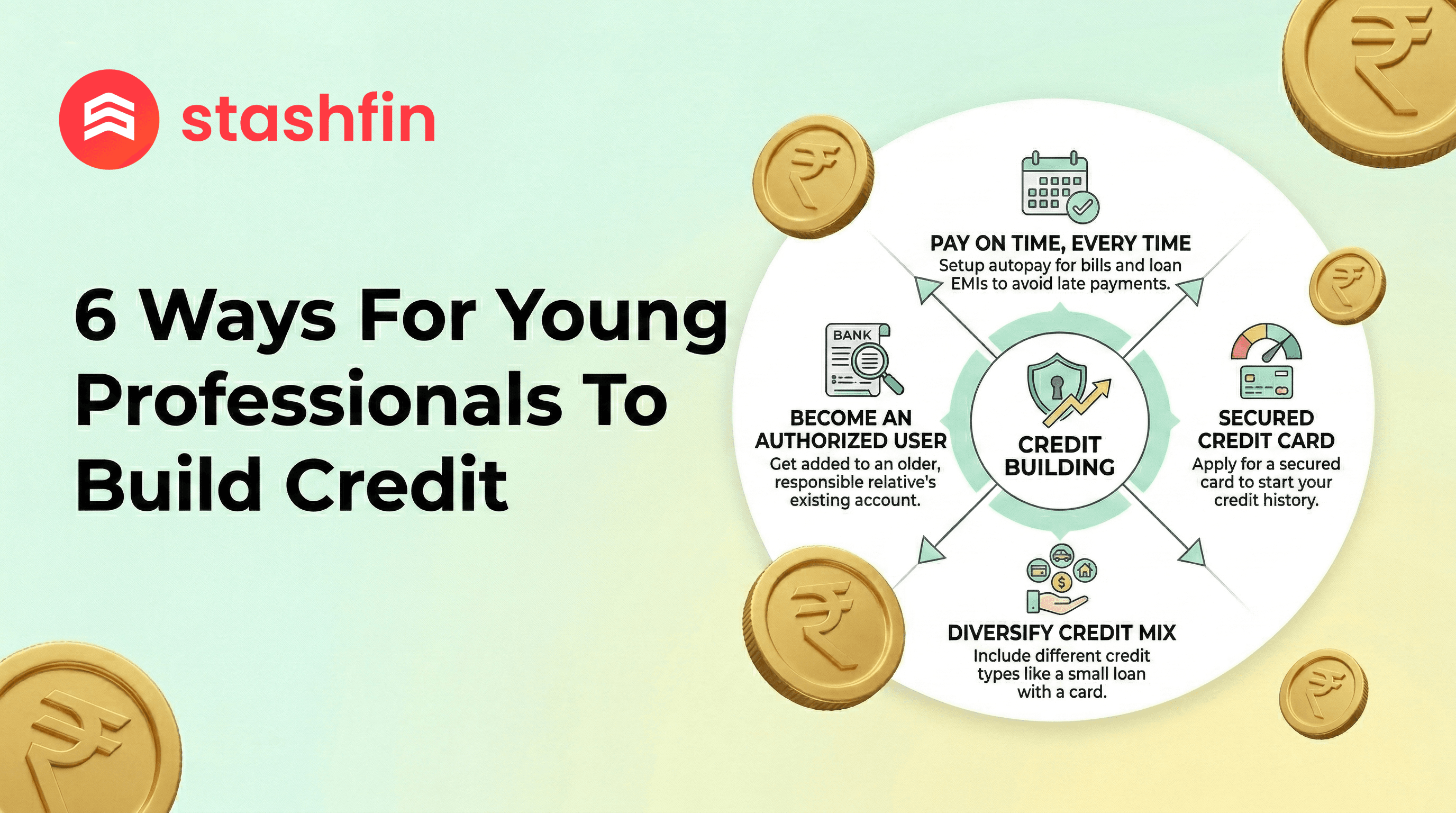

6 Ways For Young Professionals to Build Credit

Building a solid credit foundation is essential for your financial future. In 2026, having a high credit score is the key to unlocking lower interest rates, premium credit cards, and seamless loan approvals. Here is how young professionals can navigate the journey from a "No-Score" profile to credit excellence.

1. Start Small with a Personal Credit Line

The biggest mistake young professionals make is waiting for a large loan to start their credit journey. Instead, start with a "micro-credit" facility.

- Flexibility: A personal credit line offers more control than traditional loans.

- The Strategy: Apply for a small limit. Use a portion (e.g., ₹5,000) for routine costs and pay it back promptly.

- The Stashfin Advantage: We offer instant approval for first-time borrowers and 0% interest for up to 30 days, letting you build your score for free.

2. Leverage the "Credit Builder" Program

If you have zero credit history, traditional banks may hesitate to approve you. A dedicated Credit Builder program is designed specifically for "New to Credit" profiles.

How it works: You take a small, manageable loan specifically meant for reporting to bureaus like CIBIL and Experian. Consistent, on-time repayments act as "positive strokes" on your report. Within 6–8 months, a formal credit score will emerge.

3. Master the "30% Utilisation" Rule Early

Your credit score is heavily influenced by how much of your available limit you actually use. Using your entire limit every month signals that you are "credit hungry."

- The Goal: Keep your total credit usage below 30% of your approved limit.

- Example: If your Stashfin limit is ₹50,000, try to keep your outstanding balance below ₹15,000.

- Pro-Tip: Making multiple small repayments throughout the month helps keep this ratio low.

4. Automate Your Monthly Commitments

Payment history accounts for roughly 35% of your credit score. A single missed payment can stay on your report for years.

- Set up Auto-Debit (NACH): Use UPI-based mandates for your EMIs.

- Maintain Balance: Ensure your linked salary account has sufficient funds at least two days before the due date.

- Avoid Technical Bounces: Late fees aren't the only problem; a technical bounce can hurt your score significantly.

5. Diversify Your Credit Mix Over Time

Lenders look for your ability to handle different types of credit. A "thin" file with only one card is less impressive than a balanced portfolio.

- Revolving Credit: Like a Stashfin Credit Line.

- Installment Credit: Like a small consumer durable loan for a laptop or a two-wheeler loan.

Aim for a mix over 2–3 years to demonstrate you can manage various repayment structures.

6. Monitor Your Report for "Ghost Entries"

Data errors or identity theft can happen. You might find a loan in your name that you never took, or an old closed account still showing as "Active."

- Check Monthly: Use the Stashfin App to check your credit report.

- Soft Inquiry: This check does not hurt your score.

- Dispute Errors: Correcting a single wrong entry can sometimes boost your score by 50+ points instantly.

Credit Building Roadmap for Freshers

| Milestone | Action Item |

|---|---|

| Month 1 | Download Stashfin & Apply for a basic Credit Line. |

| Month 3 | Use the line for a small purchase; set up Auto-Debit. |

| Month 6 | Check your first CIBIL score (Aim for 700+). |

| Month 12 | Request a limit increase to lower your Utilization Ratio. |